Financial regret is very real and manifests itself in various forms. Even Warren Buffett doesn’t have a 100% win rate when it comes to picking stocks. For the rest of us, financial regret comes about in other ways, including ill-timed investments, noting buying bitcoin in 2009 or not saving for retirement when we’re in our 20s.

Other common financial mistakes among “regular” people include superfluous spending, which leads to uncomfortable debt burdens. Point is no one is perfect and it’s not a stretch to say all of us have at least one financial regret. Point number two is that we don’t want to be judged for those missteps because chances are we’re already internally raking ourselves over the coals.

That’s something for advisors to remember when dealing with any client expressing financial compunction, but it’s particularly true with women. It’s not that men are better able to handle criticism or that women are more emotional. Rather, castigation of women’s financial missteps is portrayed differently in “polite society. ” Said another way, men, for no good reason, are extended more latitude when it comes to money mistakes than are women and women are aware of this. Advisors should be, too.

‘Reckless’ vs. ‘Strategic’

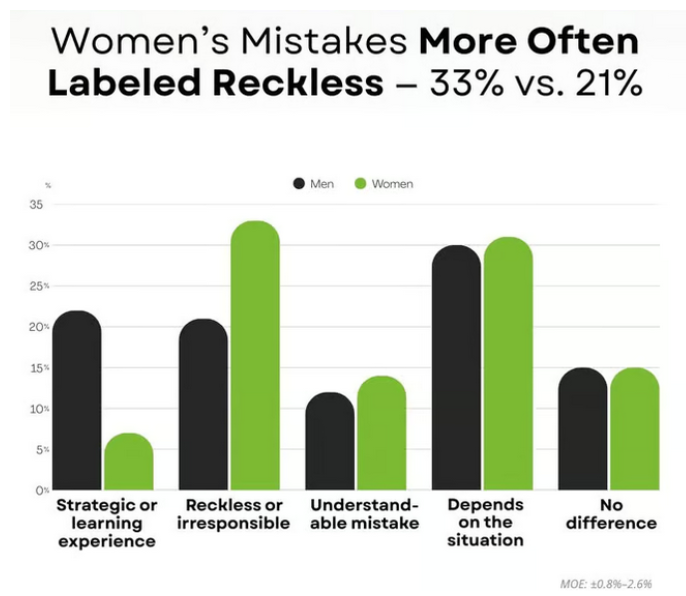

It’s 2025, but a lot of gender double standards and stereotypes persist. For example, a man that loses $5,000 on a meme coin or meme stock may be viewed as a “savvy risk taker” or “strategic. ” Conversely, a woman committing similar errors is considered “reckless. ”

“When asked how financial mistakes are portrayed in the media, only 7% of respondents said women’s financial mistakes are portrayed as strategic, compared to 22% who said the same about men,” according to BadCredit. org.

(Image: BadCredit. org)

A lot of this is attributable to old thinking. There was a time when men largely controlled household finances because society simply believed women weren’t up to that task. It wasn’t until the 1960s that women could get bank accounts and it wasn’t the Equal Credit Opportunity Act (ECOA) was passed in 1974 that creditors were forced to eliminate gender as a lending criteria. We’ve come a long way, but there’s more work to be done.

“The stereotype that women are bad with money may be to blame for this skewed viewpoint. Stemming from societal expectations and historical disadvantages, many people still believe, even if subconsciously, the myth that women can’t responsibly manage their money, let alone understand finances,” adds BadCredit. org.

Other Considerations for Advisors

Should advisors develop plans, strategies and tools specific to female clients? Absolutely. Do women want and expect that level customization? Definitely. Can some or all of that amount to advice that’s different than what’s dispensed to male clients? Yes.

This is where things get interesting for advisors. Giving a woman different financial advice than what’s given to a man because of the woman is a high earner, recently widowed or has low risk tolerance is one thing. Telling her something different than what would be said to a man simply because she admitted to a financial mistake is a whole other ballgame and a scenario that should be avoided.

“New data shows nearly 1 in 4 Americans think women are not only judged more harshly but also receive different financial advice, and that perception could carry real reputational weight and financial implications,” observes BadCredit. “While 23% of surveyed Americans say women receive different advice and are judged more harshly for financial mistakes, only 13% say men face more judgment and are advised differently. ”

Bottom line: we all have financial regrets and the best thing an advisor can do is help clients, regardless of gender, move past those hurdles not punish them for the missteps.