Much has been made about elevated levels of credit card debt in this country. Throw in increased talk about seven-year car loans and it’s clear high interest rates are burdening U. S. consumers.

Soaring credit card debt is attributed to high inflation and stubbornly low employee compensation, which is to say many Americans aren’t spending frivolously on their credit cards. They’re racking up credit card debt because they’re using cards to buy necessities. Speaking of necessities, automobiles are necessary for a massive percentage of this country’s. Seven-year loans or not, many folks need cars to get to work.

Problem is auto and credit card bills aren’t the “good” kind of liabilities as mortgage debt is considered to be. In fact, consumer debt is prime breeding ground for financial regret. Servicing those liabilities gets in the way of more productive allocations of capital, including saving for homes or college, planning for retirement and fortifying taxable investment accounts.

Although there’s a silver lining, sort of, credit card debt is a call for those saddled with it to not fall victim to pride and contact advisors for budgeting assistance.

Consumer Debt Nearing Catastrophic Levels

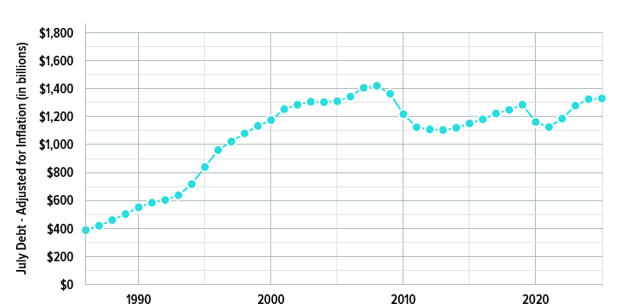

The aforementioned silver lining, if it can be called that, is when adjusted for inflation, the July level of credit card was 6% below the all-time high, according to WalletHub.

(Image: WalletHub)

Still, the second-quarter credit card debt increase of $28 billion took the total tab to $1. 32 trillion, representing a 0. 4% year-over-year jump. Optimists might say 0. 4% isn’t a lot, but $1. 32 trillion is and the strain that number has on consumers is tangible. It’s also highlight the efficacy of some tried-and-true debt-reduction strategies, including eliminating the debt on the card with the highest interest rate.

“Most people with serious credit card debt have multiple balances. If that’s the case for you, try the ‘avalanche method,’” advises WalletHub. “That means putting the majority of your monthly debt payment toward the balance with the highest interest rate and making the minimum payment required on the rest. Once your most expensive debt is paid off, repeat the process until you’re debt-free. ”

How the Fed Figures In

The Federal Open Market Committee (FOMC) will render a decision on interest rates on Sept. 17 and Fed funds futures imply an almost 90% chance the Federal Reserve will lower interest rates. For individuals, that could result in a few dollars saved per month in interest expenses, but in aggregate, the benefits are considerable.

“Exactly what impact such a move will have on consumers’ wallets and the economy more broadly remains to be seen, but we can project that a 25-basis-point cut will save consumers roughly $1. 92 billion in interest over the next 12 months,” according to WalletHub.

For those not familiar with the plumbing on interest rates as it relates to most traditional forms of consumer debt, the Fed’s impact on credit cardholders carrying large balances is meaningful because nearly all credit cards have variable rates. In simple terms, that paves the way for card issuers to raise interest rates when the Fed does the same. Bottom line: the Fed’s recent tightening campaign cost indebted consumers tens of billions of dollars.

“Due to the 525 basis points in Federal Reserve rate hikes from March 2022 to July 2023, credit card users were set to pay roughly $40 billion more in interest during 2024 than they would have otherwise,” adds WalletHub.