I’ve long been a student of game theory, the branch of mathematics that studies how rational actors make decisions when their outcomes depend on what everyone else does. It’s a helpful framework for understanding markets and geopolitics, and right now, there’s no better place to apply it than Taiwan.

The stakes couldn’t have been higher this week as President Trump met with Chinese leader Xi Jinping in Beijing. Xi reportedly warned Trump that “conflicts” could emerge if the two powers mishandle Taiwan.

Meanwhile, Taiwan’s legislation just approved $25 billion in special defense funding. The U.S. cleared an $11 billion arms package last December, with another $14 billion package reportedly waiting in the wings.

Chicken on the World Stage

There’s a famous scenario in game theory called the game of Chicken. Two drivers race toward each other head-on. The one who swerves first loses face but survives. If neither swerves, both are destroyed. The dilemma is that each player wants the other side to blink first, but the cost of miscalculation is catastrophic.

That’s precisely what’s at stake across the Taiwan Strait.

China believes reunification with Taiwan is inevitable. Xi perceives the island as the “core of China’s core interests,” and Beijing has never taken the use of force off the table.

On the other side, the U.S. has maintained military and political backing for Taiwan for more than 75 years. Abandoning that commitment would, as one analyst put it, trigger a “disastrous chain reaction” across America’s entire Indo-Pacific alliance system.

It would also mean surrendering the territory that produces over 90% of the world’s most advanced semiconductors.

In a textbook game of Chicken, the cost of collision is fixed. Both players know what mutual destruction looks like. But in the Taiwan Strait, the cost of a crash is growing exponentially, and that’s mostly due to artificial intelligence (AI).

Taiwan’s Semiconductor Dominance

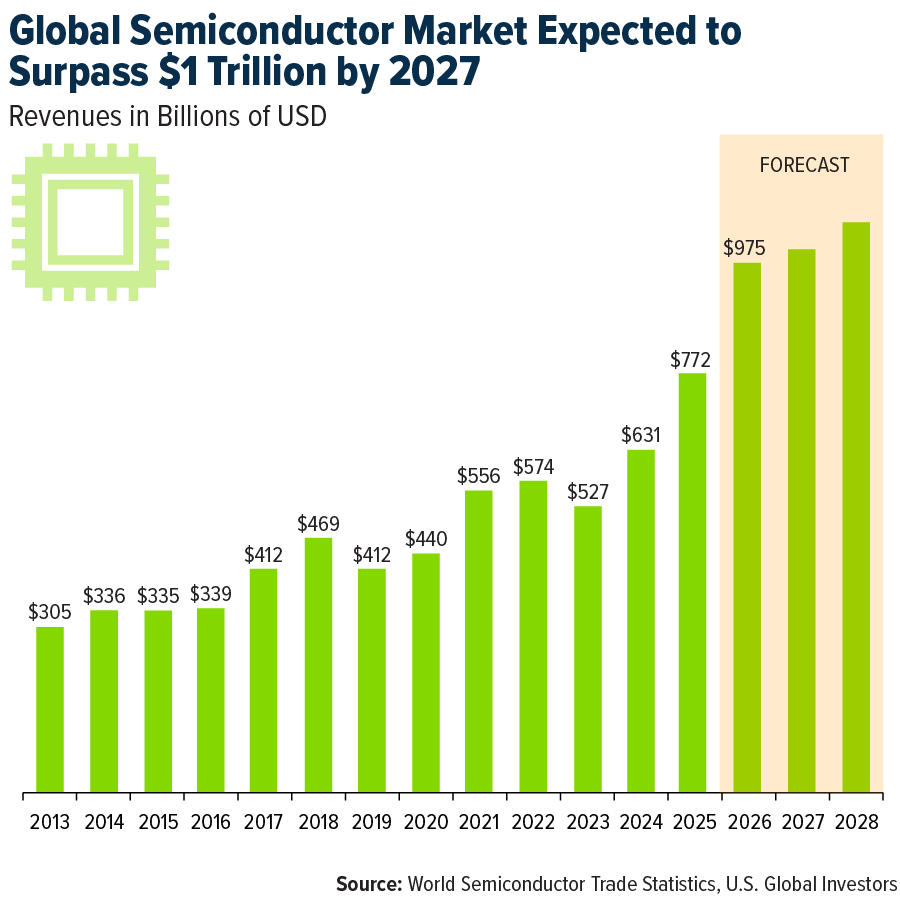

To put things in perspective, the global semiconductor industry is projected to reach $975 billion in annual sales this year, $1 trillion next year. Generative AI chips alone will generate an estimated $500 billion in sales.

Taiwan Semiconductor Manufacturing Co. (TSMC) alone enjoys a roughly 70% global market share in this massive industry. This has helped make it the sixth most valuable company in the world, with a market cap exceeding $2 trillion.

Apple and NVIDIA alone account for almost 40% of TSMC’s sales. Add in their other customers—Microsoft, Amazon, Alphabet, Meta, Oracle—and the broader equipment supply chain, and you’re looking at roughly $30 trillion in market value directly or indirectly tethered to Taiwan’s chip fabrication.

TSMC posted an incredible 58% jump in quarterly profits in the first quarter because of the AI boom.

Taiwan’s economy has likewise boomed. Its GDP grew nearly 14% in the first quarter of this year, a 39-year high. In March, exports hit a record of $80.2 billion. The island’s chip dominance has become a form of military deterrence many analysts call the “silicon shield.”

The Cost of War with China

In game theory, rational players weigh the costs and benefits before making a move. So, what does the math actually look like if the silicon shield fails?

Bloomberg recently modeled five possible scenarios, from outright war to rapprochement, and the numbers are sobering. In the worst case, a U.S.-China conflict would cost the global economy roughly $10.6 trillion in the first year alone, representing about 10% of global GDP. That would eclipse both the pandemic and the 2008 financial crisis.

Those figures may actually underestimate the damage. Remember the pandemic-era chip shortages, which led to empty car lots, appliance backorders and factory shutdowns? As stated by Eyck Freymann, a Hoover fellow and author of Defending Taiwan: A Strategy to Prevent War with China, the economic shock from a U.S.-China war over Taiwan “would dwarf anything we’ve seen in the [post-World War II] period.”

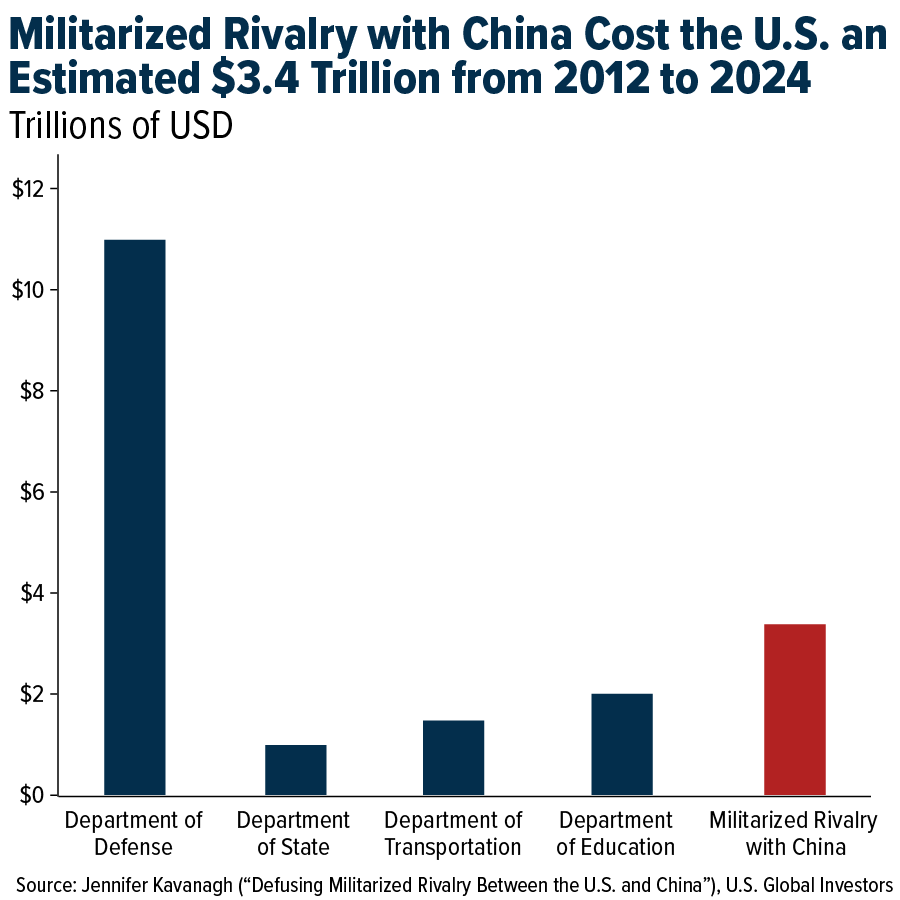

The rivalry has already cost the U.S. trillions even without a single shot being fired. A recent study from Brown University’s Costs of War project estimates that the U.S. government has spent approximately $3.4 trillion on its militarized rivalry with China between 2012 and 2024, or about $260 billion a year.

That’s roughly 30% of total defense spending over that period, nearly double what the federal government spent on education, and 3.5 times the cumulative budget of the State Department.

CEOs at the Table

More than a dozen of America’s most powerful CEOs joined Trump’s delegation to Beijing, including Apple’s Tim Cook, NVIDIA’s Jensen Huang, Tesla’s Elon Musk and Goldman Sach’s David Solomon. The group’s combined net worth is nearly $1 trillion.

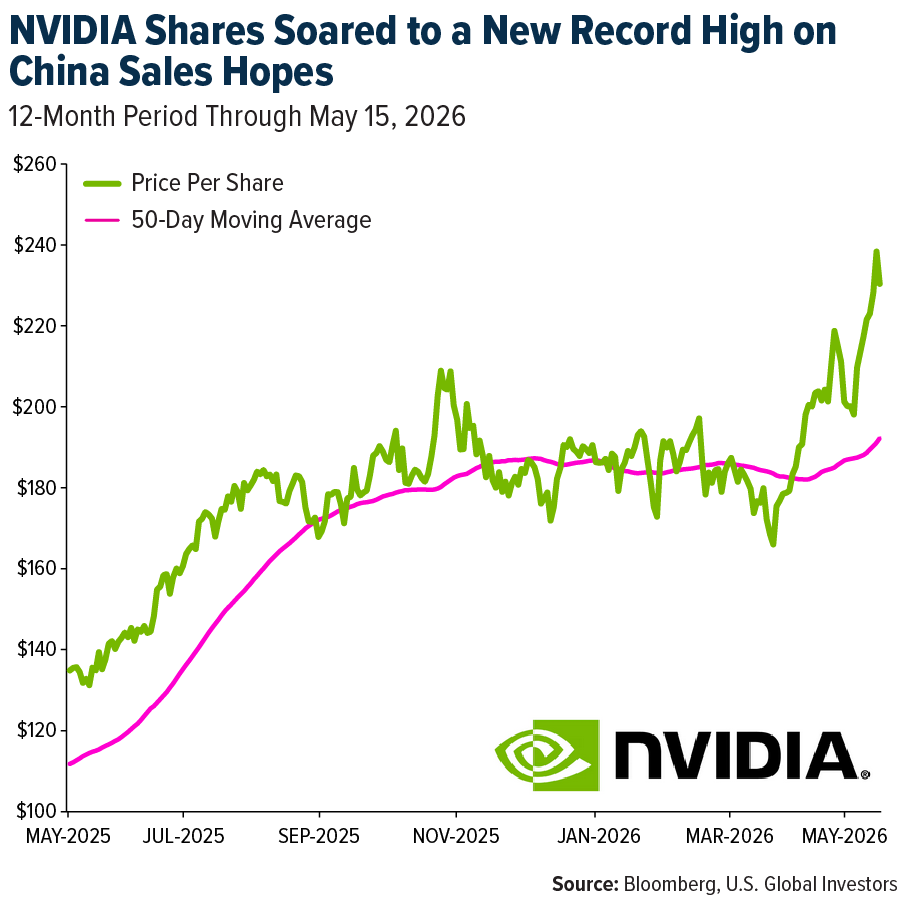

The summit doesn’t appear to have been a raving success for these U.S. mega-caps. Trump touted “fantastic trade deals,” and NVIDIA shares hit a new record on reports that Washington had cleared 10 Chinese firms to buy its H200 chips. But Beijing hasn’t said if it would permit those sales.

No breakthroughs were made on tariffs or Taiwan either. Xi’s warning about “conflicts” still hangs in the air.

An Insurance Policy Against Catastrophe

In game theory, when the cost of collision is high enough, rational actors are more likely to find ways to cooperate. Taiwan’s growing importance to the AI revolution, and the deepening economic ties between Taipei and Washington, may be the best insurance policy the world has against catastrophe.

But as any game theorist will tell you, rationality is an assumption, not a guarantee. Investors would be wise to keep an eye on the Strait.

Airlines and Shipping

Strengths

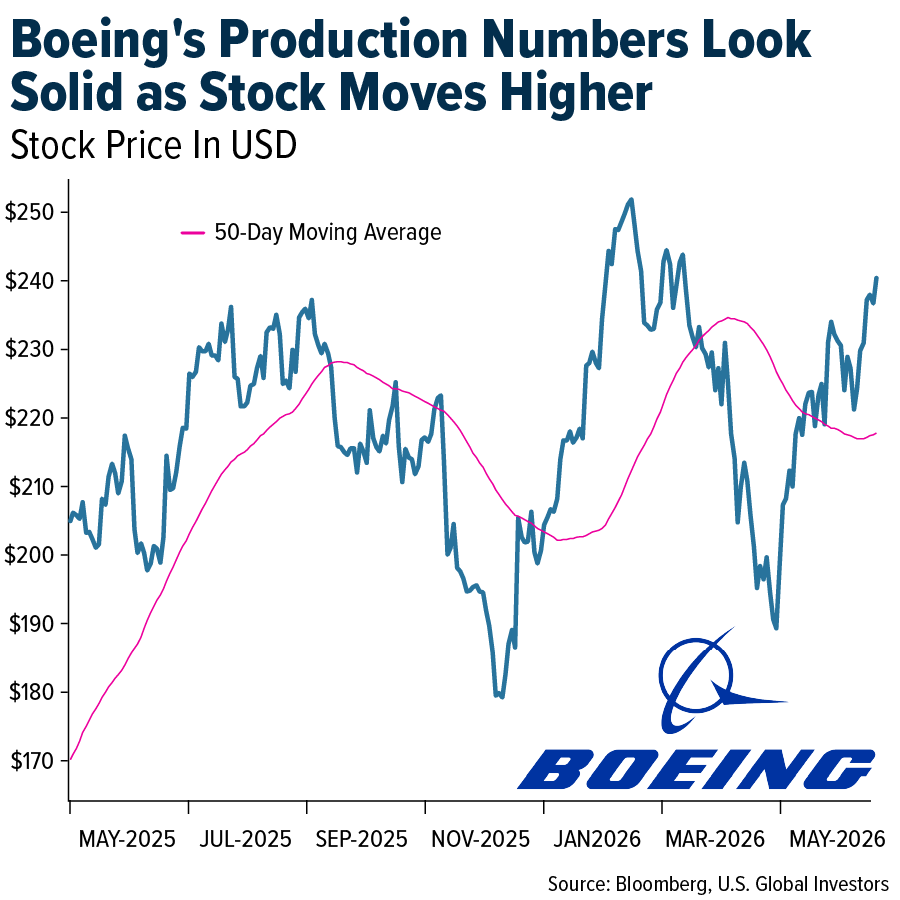

- The best-performing airline stock for the week was Copa, up 7.3%. According to Morgan Stanley, Boeing delivered 47 aircraft in April, including 34 MAX and six 787s. This compares to 29 MAX and eight 787s delivered in April 2025. In addition, China pledged to buy another 200 Boeing aircraft.

- According to Morgan Stanley, shipping rates from Asia were up 3.6% this week on North America routes to the West Coast and up 0.7% this week to the East Coast. Rates on Europe routes from China were down 1.6% this week to Northern Europe and down 0.1% this week to Mediterranean locations.

- As reported by JPMorgan, Copa Holdings delivered a strong quarter, with operating profit of $259 million, up 13% versus Bloomberg consensus, and net income of $212 million, up 13% versus consensus. More importantly, the company introduced second quarter 2026 guidance and currently expects an operating margin between 8% and 12%.

Weaknesses

- The worst-performing airline stock for the week was Sabre, down 22.6%. In the month of April, the number of U.S. citizen departures to international regions was down 2% year-over-year (YoY). However, the number of non-U.S. citizen international arrivals into the United States fell 10% YoY, according to Morgan Stanley.

- Hormuz transits are down to 1% of normal in the past week, with the U.S. and Iran double blockade disrupting flows. However, the Iran war has driven Red Sea transits to around half of normal, with Red Sea crude transits above normal levels given surging Yanbu Saudi exports and with container transits somewhat lagging at 10% to 20% of normal, according to Bank of America.

- TSA throughput volumes have now declined on a year-over-year basis at a low-single-digit pace, according to BMO, for the past three weeks, with quarter-to-date traffic down 0.6% YoY. This potentially reflects several factors, including higher fares, reduced schedules, and the closure of Spirit.

Opportunities

- According to Morgan Stanley, there has been a notable effort to reclaim aircraft, liquidate assets, and redistribute valuable airport slots among other airlines. They believe Spirit’s airport access in major cities and operating slots at airports like LaGuardia and Newark Liberty would be highly sought after by other airlines.

- Maersk Management believes many ocean carriers are analyzing the potential gradual return of service to the Red Sea. If conditions remain favorable in terms of safety and there is availability of naval escorts, more carriers could restart transits via Bab el-Mandeb in a matter of weeks, according to UBS. While this may represent a short-term headwind to industry profitability, it would also serve as a catalyst to rationalize capacity and provide an avenue to reduce costs.

- In an interview, Wizz Air CEO Jozsef Varadi said that the airline is seeing not just volume growth, but also revenue growth for the peak summer season, as budget fares attract passengers and help offset the impact of the Iran war. According to Varadi, Wizz Air is seeing between €100 million and €200 million in cost savings materializing in the current financial year. On the topic of jet fuel, he said it is available in Europe and that, looking ahead to the next six to eight months, the airline appears well positioned, with suppliers confirming fuel availability.

Threats

- According to TD, Spirit announced its liquidation, and Frontier loaded its full third quarter schedules. Frontier cut 1.8 points from its second quarter schedule, while United cut 2.2 points from its third quarter schedule. JetBlue added 3.4 points to its third quarter schedule.

- Car carrier time charter rates grew higher by 10% to 20% month-over-month in April 2026, with oversupply concerns more than offset by robust first quarter 2026 demand tracking at up 10% year-over-year (YoY), led by strong Chinese auto exports. In addition, Japanese shipping companies reported some car carrier margin squeeze from surging fuel costs since the Iran war, according to Bank of America.

- Wizz Management’s commentary on load factors and yield heading into the first half of 2027 suggests downside risks, reports Morgan Stanley. This comes on both first half 2027 and full-year 2027 estimates of £318 million and negative £203 million, respectively, in their view.

Luxury Goods and International Markets

Strengths

- Viking Holdings reported strong financial results this week, with first-quarter revenue rising 17.5% year-over-year to more than $1 billion. The cruise company also said bookings for 2026 remain very strong, showing continued demand for luxury travel. Investors reacted positively to the results, sending Viking shares higher after the announcement.

- The United Nations World Tourism Organization (UNWTO), the agency that tracks global tourism trends, expects global tourism to grow by 3–4% in 2026 after international tourist arrivals reached 1.52 billion in 2025, up 4% from the previous year and above pre-Covid 2019 levels for the first time. Europe’s 2026 tourism growth may support luxury and beauty travel retail.

- Shinsegae Inc., a South Korean luxury retail and department store operator, was the best-performing stock in the S&P Global Luxury Index over the past five days, with shares rising more than 20%. The move is driven by strong investor optimism following upbeat earnings results and improving demand trends across the premium consumer segment.

Weaknesses

- Burberry reported stronger financial results this week, with improving sales and a return to operating profit as its turnaround strategy showed progress. However, shares fell after the announcement as management warned that geopolitical and macroeconomic uncertainty could weigh on consumer spending. The company also did not reinstate dividend payments, which some investors had expected.

- The EU economy grew by only 10 basis points in the first quarter and 80 basis points year-over-year (YoY), highlighting a slow recovery in the region. Economists generally view around 1.5% to 2.0% annual GDP growth as a healthy pace for the eurozone economy, meaning current growth remains well below normal levels.

- Ananti, a South Korean luxury hospitality and resort developer, was the worst-performing stock in the S&P Global Luxury Index, with shares down almost 23% over the past five days. Shares declined as investors reacted to concerns over weakening earnings, rising financial risks, and continued volatility in the company’s stock price following softer recent results.

Opportunities

- Watches of Switzerland Group shares gained about 19% on Thursday after the company reported stronger-than-expected sales and raised its profit outlook. Investors were encouraged by strong U.S. demand, where wealthy consumers continued buying luxury watches from brands like Rolex and TAG Heuer. The company also forecast higher profits than analysts expected, boosting confidence that luxury spending among high-income consumers remains resilient.

- Piper Sandler analyst Alexander Potter believes Tesla has further upside, maintaining an Overweight rating with a $500 price target versus the current share price of $444. However, his valuation excludes potential revenue from Optimus, which could eventually become more significant than Tesla’s vehicle business. Elon Musk has said Tesla’s future value could exceed $20 trillion, positioning Optimus as a potential multi-trillion-dollar opportunity.

- President Donald Trump visited China this week for high-level meetings with Chinese President Xi Jinping in Beijing. The visit focused on trade, technology, and regional security issues, including tensions over Taiwan and economic cooperation between the two countries. President Trump said that Chinese President Xi Jinping would like to see a deal with Iran, a reopening of the Strait of Hormuz, and has offered to help.

Threats

- The ongoing Iran conflict is significantly hurting the luxury sector in the UAE, with major malls in Dubai and Abu Dhabi reporting luxury sales declines of 30 to 50% as tourism and foot traffic weaken, The downturn is especially damaging because the Middle East, particularly Dubai, has become one of the luxury industry’s most profitable regions, Brands including LVMH, Kering, and Hermès are now warning investors that geopolitical instability, disrupted travel, and weaker consumer confidence could delay any recovery in luxury spending

- With the reporting season in the luxury sector almost over, with Compagnie Financière Richemont (CFR) still due to report, luxury stocks remain under pressure, Year to date, LVMH shares are down 27%, Hermès is down 21%, and Kering has fallen 19%, Investors remain on the sidelines due to geopolitical tensions and a lack of clear recovery in China’s consumer market

- China’s retail sales data next week could show a modest improvement, but most economists still expect consumer spending to remain relatively weak overall, Recent holiday spending and travel data have been slightly better, and government stimulus measures are helping support consumption, However, investors remain cautious because China’s property market is still weak and consumer confidence remains low.

Energy and Natural Resources

Strengths

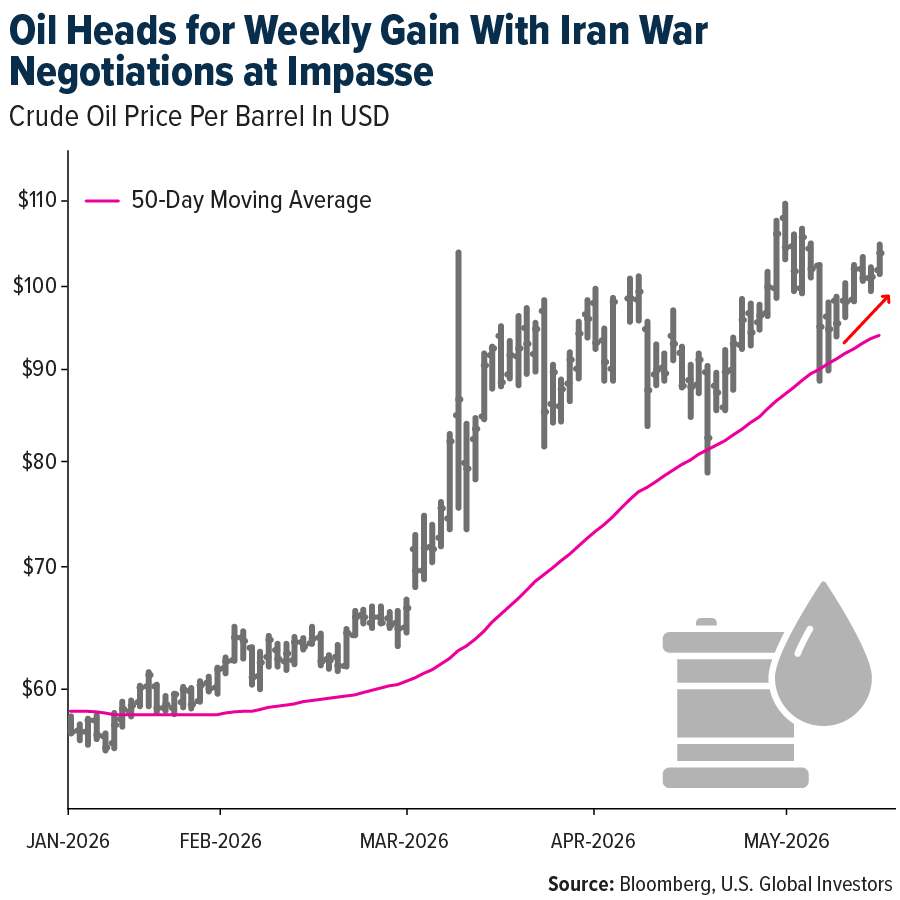

- The best performing commodity for the week was WTI crude oil, up 10.71% on no meaningful signs of progress on finding common ground to ending the war with Iran. The Strait of Hormuz remains highly constrained for traffic which is beginning to have more knock-on effects with the restriction to shipping. Global oil inventories have declined at a record pace, and the market will remain “severely undersupplied” until October even if hostilities end next month, the International Energy Agency (IEA) said this week.

- Fervo Energy’s IPO surged 35% on its first day of trading, pushing the geothermal company’s valuation past $10 billion — a clear signal that markets see dedicated baseload energy as critical infrastructure for AI-driven data centers. With $7.2 billion in supply contracts from Google and Shell and its Cape Station project targeting 500 megawatts initially expandable to 2–4 gigawatts, Fervo is positioning geothermal as the go-to power source for computers that demands 24/7 reliability independent of grid constraints.

- The first quarter was broadly stronger than expected for copper miners despite rising energy costs. Operating margins held up well at current spot prices, while full-year direct production cost estimates increased only modestly to $2.09 per pound. Valuations are signaling opportunity, with miners trading at just a 3% premium to spot versus an 18% three-year average. Meanwhile, supply disruptions at Grasberg and Kamoa-Kakula are viewed as structurally bullish for the multi-year copper outlook.

Weaknesses

- Cotton was the week’s worst-performing commodity, falling 4.86% as officials offered vague promises of billions in exports to China without providing details. Corn and soybeans also declined. Farmers and traders are still looking for specifics on purchase volumes and timing, hoping for a deal large enough to improve difficult market conditions.

- The national wheat harvest has hit a 55-year low, reflecting the mounting pressures on U.S. grain production. For farmers still in the game, this scarcity could present a meaningful pricing opportunity as tighter supply supports stronger wheat markets. Wheat futures climbed 2.6% for the week.

- The surge in interest rates that came at the close of the week wiped away all the gains copper made up in till midweek with Thursday and Friday’s losses approaching a 6% decline. Copper prices near record highs have started to deter demand in China, with fabricators seeing orders weaken this month. Higher interest rates are also a barrier to demand growth.

Opportunities

- India has launched a $3.9 billion incentive plan to accelerate coal gasification, covering 20% of plant and machinery costs with the goal of converting 75 million tons of coal into synthetic gas across 25 new plants within five years. The move, fast-tracked amid the Iran war’s disruption to Middle Eastern gas supplies, aims to leverage India’s vast coal reserves to reduce import dependence and ease pressure on foreign exchange.

- Climate change-related disasters have quietly diverted roughly $20 trillion in global wealth since 2000 toward recovery, preparation and insurance costs—rivaling the economic toll of the Great Recession, a Bloomberg Intelligence study finds. Meanwhile, companies that help repair, prepare for or mitigate these disasters are dramatically outperforming the broader market, showing that investors are already betting big on climate change even as the concept faces political retreat.

- Abaxx Technologies has appointed Jeff Currie, former Goldman Sachs Global Head of Commodities and current Carlyle CSO, as Executive Co-Chair, as the exchange reported its first ~CAD 1 million in trading revenue with average daily volumes surging from ~1,500 to 11,500 contracts. The company also launched MarketOS for real-time collateral mobility, completed Digital Title pilots enabling same-day settlement and secured U.S. CFTC Foreign Board of Trade approval to broaden its participant base.

Threats

- Global oil inventories are declining at a record pace of about 4 million barrels per day due to the Iran war’s disruption of Strait of Hormuz shipping, and markets will remain “severely undersupplied” until October even if the conflict ends soon, the IEA says. The crisis has also triggered the steepest drop in world oil demand since the Covid pandemic, with aviation and petrochemical sectors hit hardest as prices surged above $126 a barrel before easing to around $106.

- Australia’s LNG sector faces possible industrial action at key export facilities, creating another supply risk for Asian buyers already seeking cargoes after Middle East disruptions. A wage and working-conditions dispute involving contractor UGL Ltd. could trigger action starting Wednesday at Woodside Energy Group Ltd.’s Karratha Gas Plant and Pluto facilities. The situation recalls the strikes at Chevron’s Australian facilities in 2023, which drove a sharp rise in global natural gas prices.

- Chinese solar panel exports hit a record 68GW in March 2026—double the prior month—driven by the massive shift from passivated emitter and rear contact (PERC) to tunnel oxide passivated contact (TOPCon) technology that tripled production capacity and cut prices 70%, with 50 countries surpassing their historical import levels as China’s 80%+ share of global manufacturing capacity floods the market.

Bitcoin and Digital Assets

Strengths

- CME Group, one of the world’s largest regulated derivatives exchanges, plans to launch Nasdaq CME Crypto Index futures, providing diversified exposure to major cryptocurrencies including BTC, ETH, SOL, XRP, ADA, LINK, and XLM through a single regulated instrument. The launch comes as CME’s crypto product suite surpassed $7.3 trillion in lifetime notional volume, while average daily trading volume increased 43% year-to-date. In the first quarter of 2026 alone, CME’s crypto average daily volume rose from 191,000 to 310,000 contracts year-over-year, highlighting accelerating institutional demand for regulated digital asset products and risk-management tools.

- Coinbase is expanding its role in decentralized finance by becoming the official manager of USDC liquidity on Hyperliquid, one of crypto’s fastest-growing on-chain trading networks. The partnership strengthens USDC’s position as a core settlement asset within decentralized trading infrastructure, as USDC supply on Hyperliquid has doubled year-over-year to approximately $5 billion. Circle also announced plans to expand its technical role on the network and stake 500,000 HYPE tokens. The collaboration highlights the growing integration of stablecoins into decentralized trading, collateral, and treasury systems as DeFi trading activity continues accelerating.

- The Digital Asset Market Clarity Act advanced through the U.S. Senate Banking Committee in a bipartisan 15-9 vote, marking a major step toward establishing a clearer federal regulatory framework for digital assets in the United States. The legislation, which still requires approval from the full Senate and House of Representatives, includes provisions related to investor protections, DeFi oversight, and banking participation in digital assets. The bipartisan support signals growing political momentum for crypto regulation in the world’s largest capital market, reducing uncertainty for institutional investors and strengthening the long-term outlook for the digital asset industry.

Weaknesses

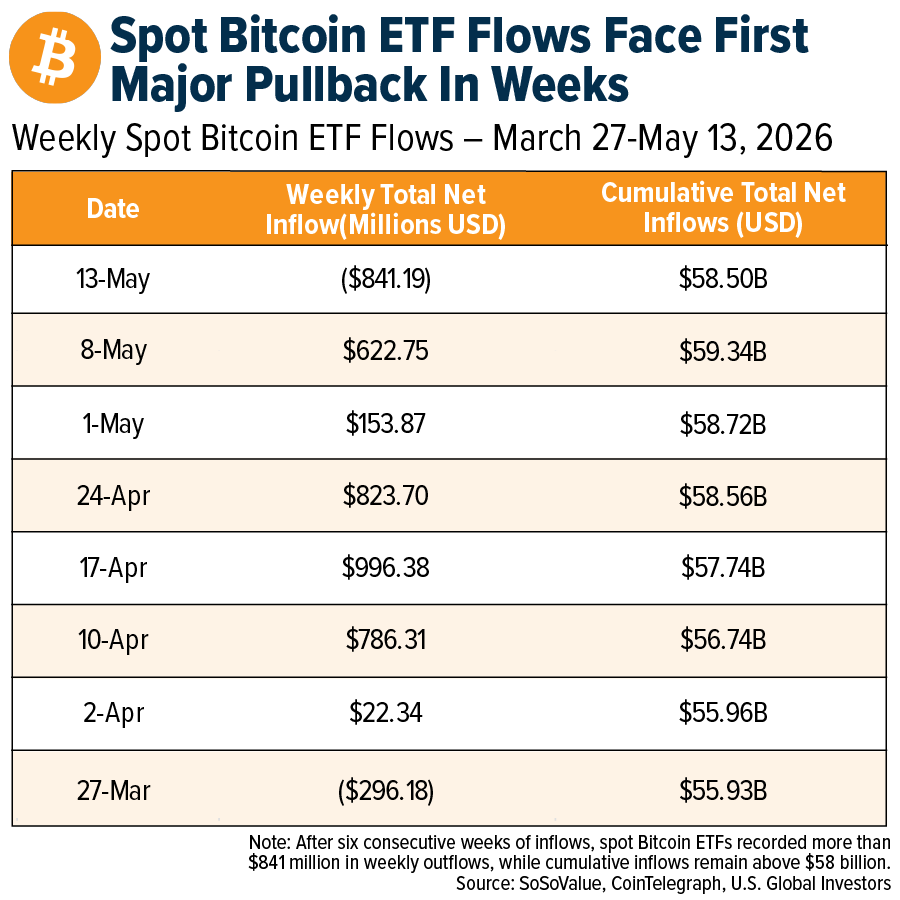

- Bitcoin’s rebound toward the $80,000 level may be less durable than it appears, as several indicators suggest the rally is being driven more by short-term trading activity than by institutional demand. U.S. spot bitcoin ETFs recorded $635 million in outflows on May 13, the largest daily withdrawal since January, while corporate bitcoin purchases fell 80% from last month. Analysts also estimate that nearly $2 billion in derivatives positions around the $82,000 level may be temporarily supporting prices through market hedging activity. Elevated realized losses of roughly $479 million per day further suggest the market has not fully stabilized despite the recent rebound.

- U.S. spot bitcoin ETFs recorded $635.2 million in outflows in a single day, the largest withdrawal since January, as bitcoin struggled to hold the $80,000 level amid rising profit-taking pressure. Weekly outflows have already reached approximately $841 million, putting the market on track for its first negative week following six consecutive weeks of inflows totaling roughly $3.4 billion. BlackRock’s IBIT led redemptions with approximately $285 million in outflows, while analysts warned that weakening spot demand and elevated unrealized gains could increase the risk of a deeper correction toward the $70,000 range.

- Bitcoin remains under pressure as rising U.S. Treasury yields and fading expectations for interest rate cuts reduce investor appetite for non-yielding assets such as BTC and gold. The U.S. 2-year Treasury yield climbed to 4.05%, its highest level since June 2025, while the 10-year yield reached 4.5% amid persistent inflation concerns and expectations that the Federal Reserve could keep rates higher for longer. Markets are now pricing in more than a 44% probability of another rate hike by December, up from 22.5% just one week ago. Bitcoin continues trading below its closely watched 200-day moving average near $82,000, highlighting ongoing macroeconomic pressure on the crypto market despite recent regulatory progress in the U.S.

Opportunities

- The Bank of England signaled it may soften proposed stablecoin restrictions following criticism from the digital asset industry, highlighting growing regulatory openness toward blockchain-based financial infrastructure. The central bank is reconsidering a proposed 20,000-pound ($27,000) holding cap per stablecoin and reviewing reserve requirements that would have required issuers to keep 40% of backing assets at the BOE earning no interest and 60% in short-term U.K. government debt. Industry participants argued the framework risked making the U.K. less competitive than markets such as the U.S. in the digital economy.

- Turnkey, a crypto infrastructure company that builds wallet and key-management technology for digital asset applications, raised $12.5 million in a funding round backed by major investors including Circle Ventures, Sequoia Capital, Bain Capital Crypto, and Galaxy Ventures, bringing its total funding to more than $65 million. The company’s technology is used for non-custodial wallets, automated on-chain transactions, and secure digital asset operations. The new capital will support the launch of Turnkey Verifiable Cloud, a secure computing platform designed for digital assets, stablecoin payments, and AI-driven blockchain activity. The investment highlights growing confidence in the long-term expansion of crypto infrastructure and stablecoin-based financial systems.

- Fasset, a digital bank that uses stablecoins and blockchain infrastructure for cross-border payments, raised $51 million to expand across emerging markets. The company operates in more than 50 financial corridors across Asia, Africa, and the Middle East, using stablecoins to offer faster and lower-cost international transactions than traditional banking systems. Fasset currently processes more than $32 billion in annualized transaction volume across 125 countries and serves more than 1,000 small and medium-sized businesses. The funding highlights growing adoption of stablecoin-based financial services, particularly in regions with inefficient traditional financial infrastructure.

Threats

- Cybersecurity threats remain a major risk for the digital asset industry, with North Korea–linked hackers responsible for more than $2 billion in crypto losses in 2025, a 51% year-over-year increase, according to CrowdStrike. The report identified DPRK-affiliated groups as the largest threat actors targeting exchanges, Web3 projects, and users through social engineering. In one major case, decentralized exchange Drift Protocol suffered about $280 million in losses after attackers used long-term infiltration and malware. The growing sophistication of state-backed cyberattacks continues to raise operational and financial risks across crypto markets.

- Strategy announced plans to repurchase about $1.5 billion of its 2029 convertible notes, with part of the transaction potentially funded through bitcoin sales. The company issued $3 billion of 0% convertible debt in 2024 with a conversion price of $672.40 per share, while the stock currently trades near $183, well below that level. The situation highlights risks tied to leveraged bitcoin treasury strategies, where debt-heavy firms may face pressure during market weakness. Forced capital raises or bitcoin sales to manage liabilities could add volatility to the broader crypto market.

- THORChain, a decentralized cross-chain liquidity protocol that enables native asset swaps across blockchains without intermediaries, suffered a cross-chain exploit of about $10.8 million, prompting a temporary halt of trading and signing operations. Following the attack, the protocol’s token RUNE fell 12%, underscoring ongoing security risks in decentralized finance. Cross-chain bridges remain among the most vulnerable areas in crypto, with more than $2.8 billion stolen from bridge exploits since 2021. The incident reinforces concerns around DeFi security and investor confidence as cross-chain ecosystems expand.

Defense and Cybersecurity

Strengths

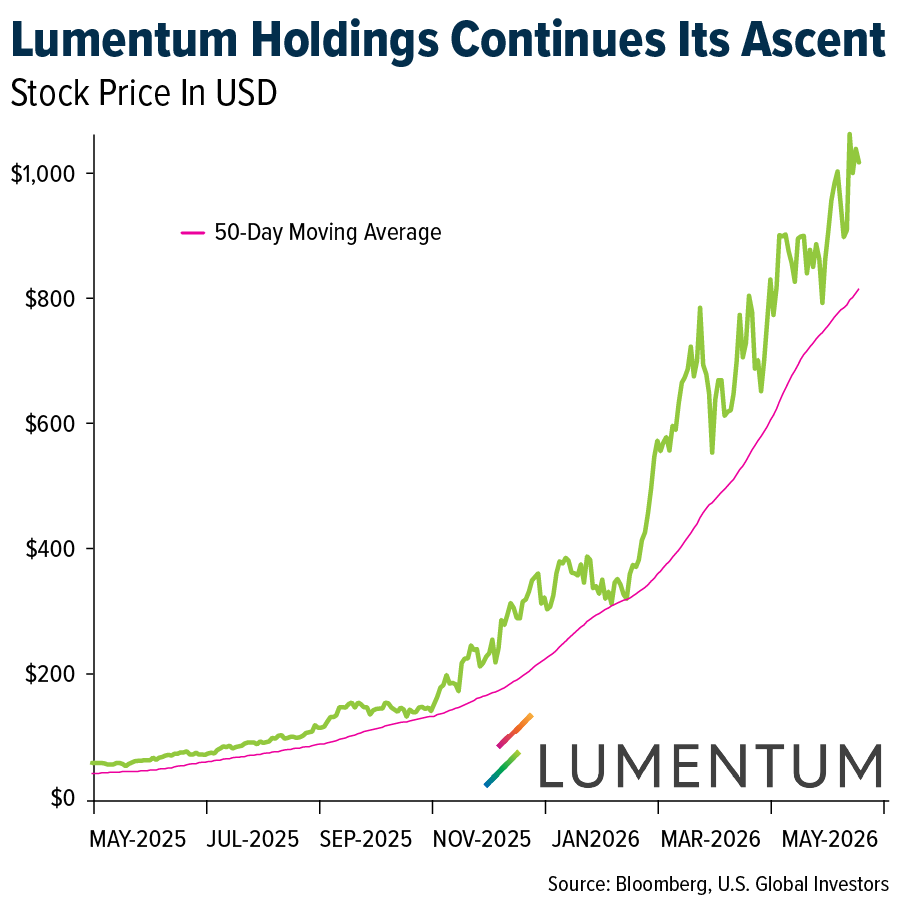

- Lumentum Holdings Inc. (LITE) will join the Nasdaq 100 Index before the market opens on May 18, replacing CoStar Group as part of a scheduled index change. The Nasdaq 100 tracks the 100 largest non-financial companies listed on Nasdaq and is followed by more than 200 investment products with over $600 billion in assets under management.

- Leidos Holdings was awarded a $2.7 billion U.S. Army contract to advance hypersonic missile capabilities. The program integrates U.S. Army and U.S. Navy hypersonic research into a single streamlined effort to eliminate duplication in development.

- OpenAI launched “OpenAI Deployment Company” with $4 billion in funding. It is embedding forward-deployed engineers into client organizations, a move that closely mirrors Palantir’s engagement strategy.

Weaknesses

- North Korean hackers stole $2 billion in cryptocurrency in 2025, marking a significant 51% increase from the previous year, with the funds believed to support Pyongyang’s military programs, according to CrowdStrike.

- AeroEdge (7409-JP) reported a standout quarter with ¥1,302 million in revenue and 14.52 EPS, marking 12.2% sequential growth and a significant year-over-year earnings surge. Despite these results and an upgraded full-year sales forecast of ¥5,050 million, the stock saw a sharp sell-off as investors reacted negatively to a projected decline in annual net income caused by technical tax adjustments. This divergence highlights strong operational momentum in aerospace manufacturing alongside a skeptical market reaction.

- Germany’s Bundeswehr excluded Palantir from a major defense cloud procurement, highlighting European tech sovereignty concerns that could limit Palantir’s role in sensitive EU defense IT.

Opportunities

- The U.S. Coast Guard has finalized a $3.5 billion contract with Davie Defense for five Arctic Security Cutters. This follows an initial planning phase initiated in February after the contract was awarded to the U.S. subsidiary of the Inocea Group.

- The U.S. has authorized Nvidia H200 sales to about 10 Chinese platforms, including Alibaba, Tencent, and ByteDance, though shipments have not yet occurred, maintaining tight capacity and high uncertainty.

- There is a new initiative aimed at military and cyber teams to accelerate the detection and patching of software vulnerabilities, marking OpenAI’s deeper expansion into active defense.

Threats

- Saudi Arabia prohibited the United States from using its airspace and military bases on its territory to launch operations in its brief bid to reopen the Strait of Hormuz, two Saudi sources said.

- Chinese President Xi warned U.S. counterpart Donald Trump that missteps on Taiwan could push the two countries into “conflict,” marking a stark opening salvo at a superpower summit in Beijing.

- The Kremlin stated that a ceasefire is impossible unless Ukraine completely withdraws from the Donbas region. President Volodymyr Zelenskyy has officially rejected these terms, calling any demand to cede territory an unacceptable surrender.

Gold Market

This week gold futures closed the week at $4,551.50, down $179.20 per ounce, or 3.79%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 6.73%. The S&P/TSX Venture Index came in off just 0.85%. The U.S. Trade-Weighted Dollar rose 1.43%.

Strengths

- The best-performing precious metal for the week was platinum, but it remained down 3.41%. Lack of progress on extricating the U.S. from Iran-related tensions weighed on credit markets, with yields on the 2-year note jumping 19.5 basis points, while 5-year through 20-year maturities all rose by more than 20 basis points. This strengthened the dollar by 1.4x%. South Africa’s gold production rose 17.1% year-over-year (YoY) in March versus 12.8% in February, according to Statistics South Africa. Mining production rose 2.5% YoY versus 9.7% in February, according to Bloomberg.

- Barrick Mining reported a strong start to the year with gold production of 719,000 ounces, ahead of company guidance of 640,000–680,000 ounces and a 6% beat versus Canaccord’s estimate of 677,000 ounces. Costs also came in better, with all-in sustaining costs (AISC) of $1,708 per ounce. 2026 guidance was unchanged, and the board authorized a $3 billion share repurchase program in addition to its dividend.

- K92 Mining reported results modestly ahead of estimates on pre-released production. Solid cost control and positive provisional pricing tailwinds supported earnings. Guidance was reiterated, weighted to the second half of the year on the ongoing Stage 3 mill ramp-up and supporting infrastructure development, according to RBC.

Weaknesses

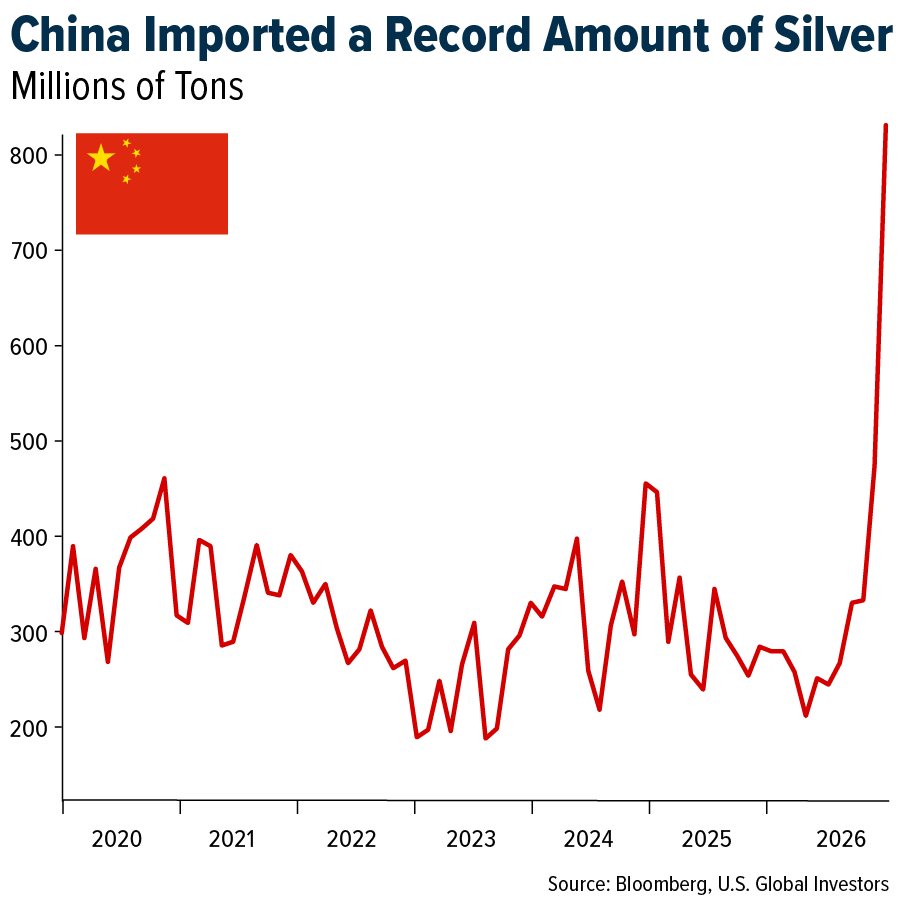

- The worst-performing precious metal for the week was silver, down 5.10%, as surging interest rates weighed on credit markets, effectively tightening financial conditions without Federal Reserve intervention. While silver is taking the hit this week, it remains a long-term market with multiple reasons to maintain a diversified portfolio. The chart below shows monthly silver imports by China. Over most of the past six years, China imported around 300 million grams of silver, or just under 10 million ounces per month. However, the most recent data point in March shows imports jumped to 836 million grams, or nearly 27 million ounces.

- First Majestic Silver Corp. shares fell after the miner reported first-quarter revenue that trailed the high end of analyst estimates. Adjusted EPS also came in slightly below consensus, according to Bloomberg. The stock declined by about 6.7%, slightly more than the average silver mining peer performance for the week.

- China’s Zhaojin Mining Industry Co. shares slumped as much as 15% in Hong Kong, the most since 2011, after a fatal accident at one of its mines prompted a broader suspension of production across its operations. An incident at a mine under construction during slag removal resulted in three fatalities and two injuries, the company said in a filing.

Opportunities

- China’s Zhaojin Mining Industry Co. is looking to acquire more gold mines in Africa and other regions, Chief Investment Officer Xu Jianzhuo said in an interview. The Shandong-based miner is targeting assets in West African countries with stable political regimes such as Côte d’Ivoire, Ghana, and Guinea, as Western miners continue exiting the region.

- Barrick Mining Corp. said it will repurchase up to $3 billion of its shares as the world’s third-largest gold producer seeks to attract investors ahead of spinning off its North American assets later this year. The latest buyback plan, which would be double last year’s repurchase program, follows a historic rally in gold prices, according to Bloomberg.

- Equinox Gold and Orla Mining announced a definitive agreement for an at-the-market, all-share combination to create a new North American intermediate gold producer with an implied market cap of approximately $18.5 billion. The deal is structured as a merger of equals with no significant price premium for investors. In contrast, Elemental Altus Royalties made an offer to acquire Vizsla Royalties this week for about $239 million, sending Vizsla’s share price up about 17.5% on the announcement.

Threats

- Precious metals refiner Heraeus noted that banks in India have been unable to import gold and silver since the start of the new Indian tax year on April 1, due to the trade ministry delaying the publication of its list of banks eligible to import precious metals until April 17. India is the second-largest jewelry market after China and has little domestic gold production, meaning it relies heavily on imports.

- Gold prices were falling on Monday after India’s prime minister told citizens to stop buying the precious metal for a year in an effort to boost the country’s foreign-exchange reserves. Prime Minister Narendra Modi said in a speech on Sunday that citizens should avoid purchasing gold, according to Barron’s.

- India, the world’s third-largest oil importer, more than doubled tariffs on gold and silver to 15% as part of broader austerity measures aimed at cushioning the economy from inflation pressures caused by energy disruptions in the Persian Gulf.

Related: AI Could Cut U.S. Healthcare Costs by Trillions—These Companies Are Positioned to Win