Early detection, I believe, is one of the smartest investments you can make, whether we’re talking about your portfolio or your health.

That’s why I recently made the decision to get a full-body MRI scan from Prenuvo and a multi-cancer blood test called Galleri, available from GRAIL.

The experience was eye-opening. In under an hour, the Prenuvo scan assessed my entire body using AI-enhanced imaging. No radiation or needles were necessary. The Galleri test, meanwhile, screens for a molecular “fingerprint” shed by cancer cells into the bloodstream before any symptoms appear.

Together, these two tests represent a new frontier in preventive medicine, one that could detect dozens of cancers years before they’d show up through conventional means.

I was so impressed by the experience that I mentioned both tests during my presentation this week at the Weiss Investment Summit in Boca Raton. Afterward, I was flooded with questions, and not just about the health implications but about the investment opportunities behind the technology.

Cancer Screenings Have Saved $5 Trillion. AI Could Multiply That

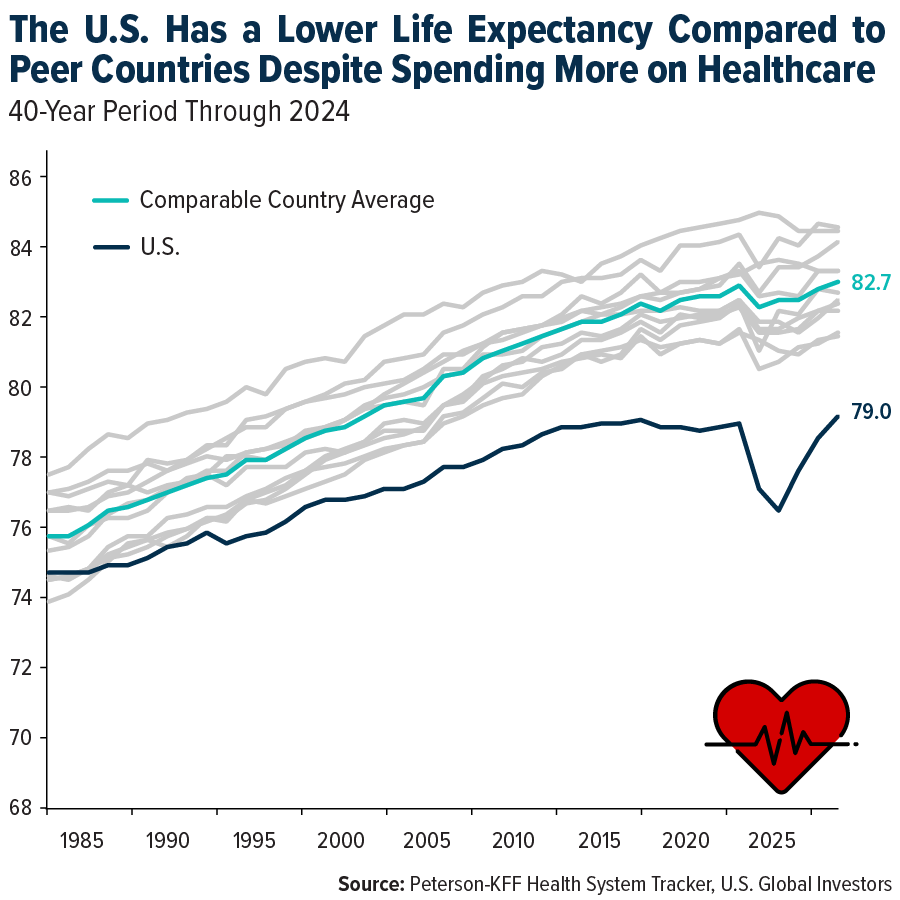

You may have noticed that healthcare in the U. S. doesn’t come cheap. In 2024, national health expenditures grew 7. 2% to a staggering $5. 3 trillion, or roughly 18% of GDP. Despite spending nearly twice as much per capita as comparable nations, life expectancy in the U. S. sits at 79, nearly four years below the peer-country average.

In other words, we’re paying more and getting less.

Part of the problem is that our healthcare system is overwhelmingly reactive. We wait until people are sick before we intervene. But the data shows that finding diseases earlier is not just better medicine, it’s dramatically cheaper.

A University of Michigan study estimated that cancer screenings alone have saved the U. S. at least $6. 5 trillion in economic value over the past 25 years, adding some 12 million years of life. This aligns with research out of England showing that early-stage cancer treatment averages about £11,200, while late-stage treatment runs to roughly £23,800, more than double the cost.

The results of early detection have been incredibly encouraging. The five-year survival rate for all cancers combined has reached 70% for the first time, a significant improvement from past decades.

It’s clear that early detection works, but the problem has been scale. That’s where AI enters the picture.

AI Beat ER Doctors at Diagnosis

The pace of AI adoption in medicine is accelerating faster than most people realize. The American Medical Association (AMA) reports that over 80% of physicians now use AI professionally, double the share from just 2023. Over three-quarters say AI provides a meaningful advantage in patient care, particularly in diagnostics and efficiency.

A landmark study published last month showed that OpenAI’s reasoning model outperformed physicians in a real-world clinical setting. At a Boston emergency room, the AI matched or exceeded human experts at every stage of patient evaluation. It was especially strong during initial triage, when information is scarcest.

Meanwhile, the Mayo Clinic found that an AI model called REDMOD can detect pancreatic cancer on routine CT scans up to three years before clinical diagnosis, identifying subtle tissue changes invisible to the human eye. In scans taken more than two years before diagnosis, the AI caught nearly three times as many early cancers as specialists reviewing the same images without AI assistance.

Everyday people are also using AI for medical purposes. Perhaps you’re one of them! A recent Gallup survey found that one in four Americans have used an AI tool for health information. Close to half say it made them feel more confident when speaking with their doctors.

Big Pharma Is Pouring Billions Into AI

For investors, the opportunity here is broad and, like AI in general, still very early.

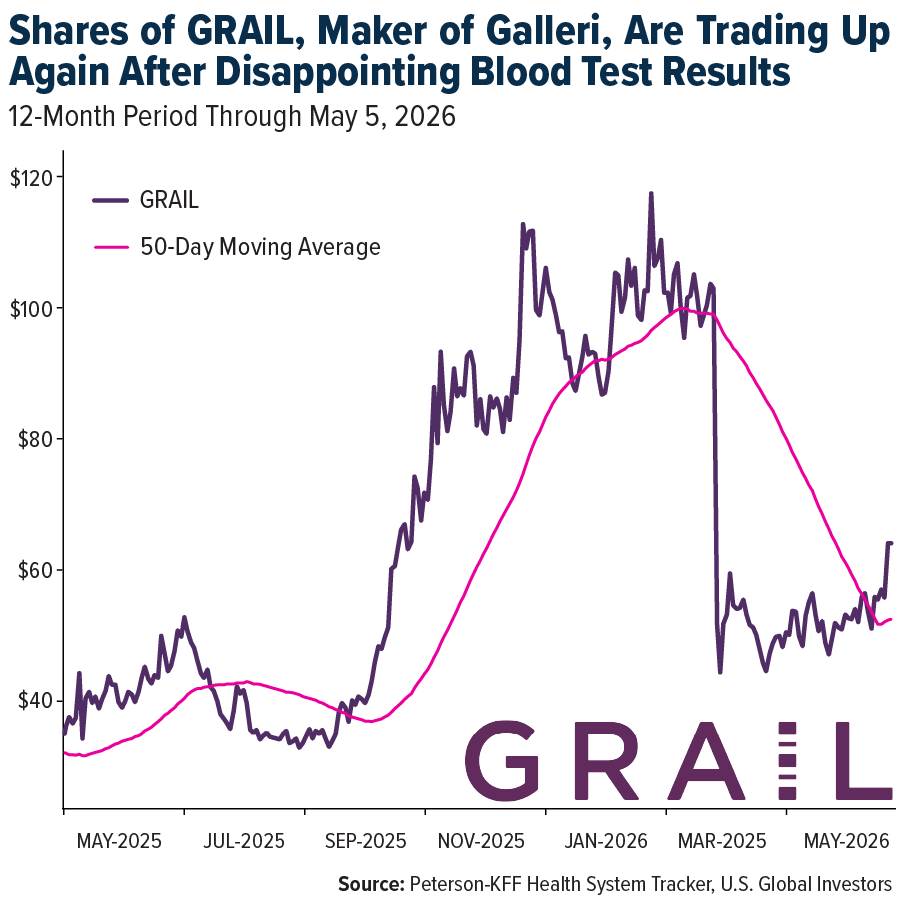

GRAIL, the company behind the Galleri test I took, reported first-quarter 2026 revenue up 28% year-over-year, with Galleri test volumes surging 50%. The company is still operating at a loss—net loss was $93. 2 million for the quarter—but the growth trajectory is hard to ignore.

Shares of the company tanked in February following reports its blood test wasn’t as effective as hoped for. But a trial of 6,000 patients in England found that a third of presumed false alarms from the Galleri test were later confirmed as cancer within 15 months, suggesting the test was detecting cancers before conventional methods could. GRAIL stock is now in recovery mode and trading above its 50-day moving average.

Prenuvo, which raised $120 million in funding last year, has secured FDA clearance for its AI-powered body composition analysis. It’s expanding beyond cancer screening into brain health and metabolic markers. The cost remains a barrier—scans run $2,500 to $4,500, and insurance doesn’t cover them—but as I said before, this is early-stage technology. Prenuvo is privately-held, with no current sign of any plans to tap public markets.

On the pharma side, Eli Lilly is interesting. The Indiana-based company recently partnered with NVIDIA to build the most powerful AI supercomputer owned by a pharmaceutical company. Lilly is already using AI to optimize production of its blockbuster GLP-1 drugs, finding manufacturing efficiencies its human engineers thought were maxed out. Rival firm Roche is reportedly building an even larger supercomputer, while companies like GSK, AstraZeneca and Merck have announced billions of dollars in AI partnerships.

How AI Could Turn America’s Most Expensive Problem Into an Investment Opportunity

In a 2024 blog post, Anthropic CEO Dario Amodei predicted that AI will fundamentally change healthcare this century. Specifically, he believes we’ll be able to squeeze 50 to 100 years of biological and medical progress into just five to 10 years. He calls this the “compressed 21st century. ”

That’s a bold claim, but when I look at the data on AI diagnostics, the trajectory supports it.

As I often say, government policy is a precursor to change. But sometimes technology is the precursor, and the market follows. Healthcare is one of America’s biggest money pits, and AI is the first tool I’ve seen with the potential to fundamentally repair it. I believe that makes it an investment theme worth following closely.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Frontier, up 32. 3%. International Airlines Group (IAG) reported first quarter 2026 results with a strong start to the year, posting EBIT of €351 million, 40% ahead of consensus, largely driven by stronger pricing (PRASK +3. 5% year-over-year). On fuel, the company now has 70% hedging coverage for the remainder of the year and expects to pass on 60% of the higher fuel costs, according to Goldman Sachs.

- According to Bank of America, Baltic Air Freight Index rates are up 26% year-over-year in second quarter 2026, with relatively tight supply and cargo airlines imposing fuel surcharges to offset higher fuel costs related to the Iran war. North Asia cargo rates are trending 25%-26% YoY higher, reflecting strong technology flows, while London rates spiked due to Middle East capacity disruptions.

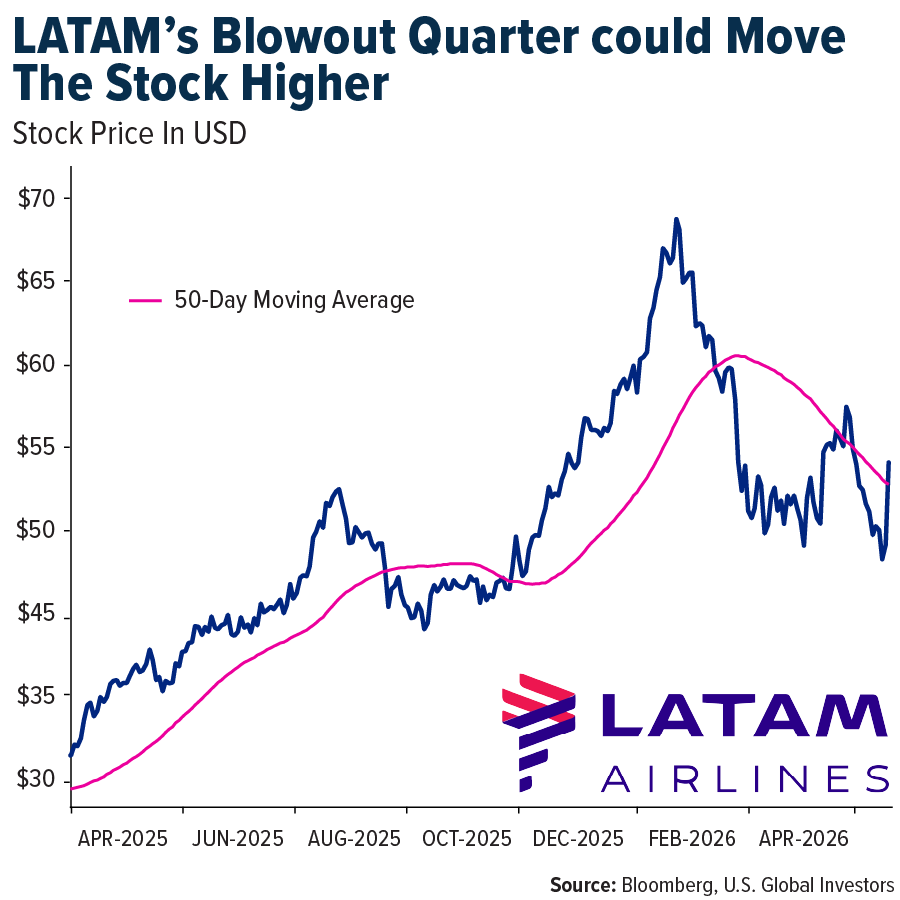

- LATAM Airlines delivered another strong quarter, mainly driven by a 9% beat in passenger yield. Adjusted EBITDA came in at $1,315 million (30% above Bloomberg consensus), while reported net income was $576 million (49% above consensus), according to JPMorgan Chase.

Weaknesses

- The worst-performing airline stock for the week was Tripadvisor, down 9. 6%. According to TD Securities, throughput in the U. S. fell 0. 8% year-over-year in April versus a 0. 5% increase in seats. Volumes lagged supply growth across most major markets. Investor focus remains on the elasticity of air travel demand and how long spending can remain resilient amid higher energy prices.

- The Iran conflict remains protracted and volatile, with 1% of global containership tonnage still stranded in the Strait of Hormuz. A brief mid-April respite saw transits rise to 43 on April 18 versus a March average of 7, but this faded as tensions re-escalated. April transits finished down 89% YoY, according to Bank of America.

- Delta Air Lines recently posted an atypical number of flight cancellations, citing crew challenges. Management noted that the elevated cancellation rate over the weekend reflected “crew resource challenges,” which had also been referenced during first quarter earnings. While several factors contributed to the disruptions, Morgan Stanley said the company is taking targeted actions to address the issues, which remain a top priority for leadership.

Opportunities

- UBS sees the bankruptcy of Spirit Airlines as driving upward pressure on industry RASM as a low-cost competitor exits the market. While carriers with the highest direct overlap, including JetBlue Airways and Frontier Airlines, are expected to benefit most in the near term, UBS also sees lasting gains for several other airlines as overall competitive intensity moderates across the sector.

- According to Goldman Sachs, laden vessels from China to the U. S. were up sequentially (+4% this week) and improved on a year-over-year basis (+25% year-over-year). Data also suggests a positive +18% week-over-week trend two weeks out.

- Ryanair’s hedge position is increasingly becoming a competitive advantage, with 80% of fiscal year 2027 fuel hedged at $670/MT, alongside its ultra-low-cost ex-fuel position. Jet fuel supply could present a risk this summer, but Bank of America does not view a material shortage as the base case. Even with flat fares, the firm estimates Ryanair’s fiscal year 2027 profit per passenger at approximately €10, rising to €12 by fiscal year 2029.

Threats

- Bank of America highlighted that Europe’s key issue is not an imminent jet fuel shortage, but rather pressure stemming from the price shock. The firm expects a 5. 5%-6. 5% contraction in the European aviation network through summer 2026 versus pre-crisis expectations as its base case, primarily reflecting capacity discipline driven by higher fuel costs.

- Logistics companies reported slower volumes across air and ocean freight markets and warned that a prolonged conflict could weigh further on demand. Consumer confidence in the U. K. and Europe also declined in April, which could further pressure demand, according to Bank of America.

- Grupo Aeroportuario del Pacífico reported total traffic declined 7. 6% year-over-year (YoY) in April. Domestic and international traffic fell 5. 0% and 10. 8% YoY, respectively. During the month, traffic in Guadalajara increased 0. 9% YoY, while traffic in Tijuana declined 10. 5% YoY. Combined traffic in Los Cabos and Puerto Vallarta was down 12. 4% YoY, according to Morgan Stanley.

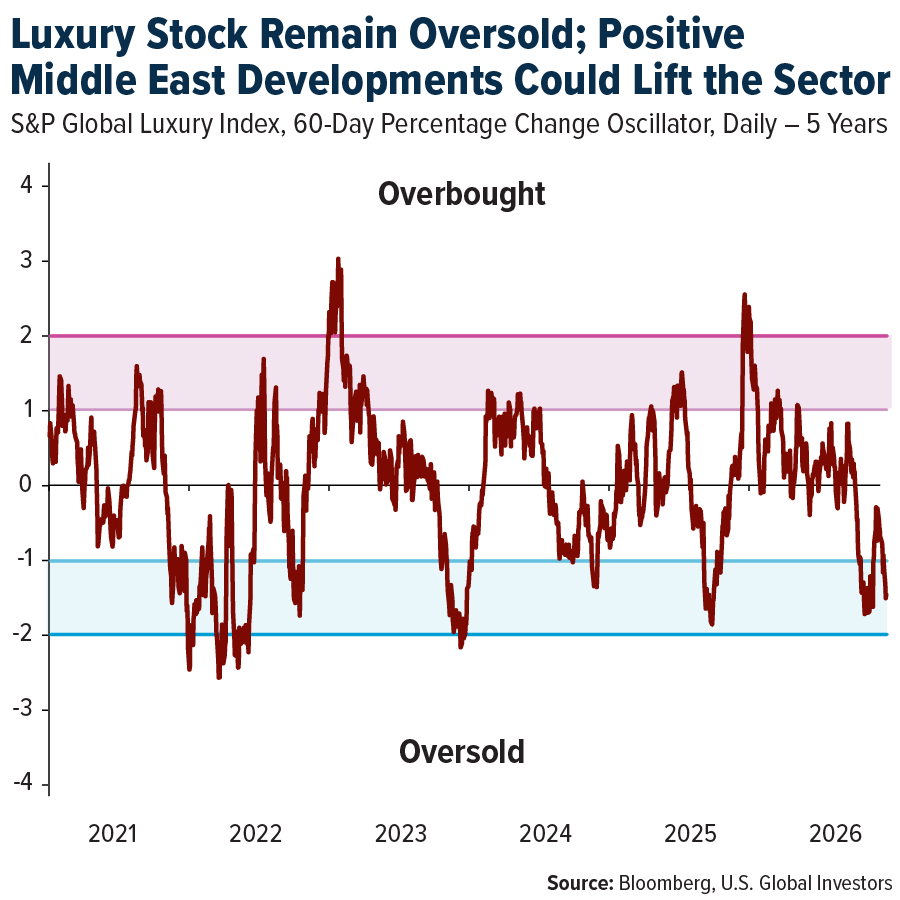

Luxury Goods and International Markets

Strengths

- Tesla shares gained this week and moved above their 50-day moving average, a key technical level often viewed as a bullish breakout signal that could support further upside momentum. Investor sentiment was also boosted by Elon Musk’s plans to build a new chip manufacturing plant in Texas, reinforcing Tesla’s long-term focus on AI infrastructure and domestic technology expansion.

- The April U. S. jobs report surprised to the upside, with the economy adding 115,000 jobs versus 62,000 expected, while unemployment held steady at 4. 3%, signaling labor market resilience despite recession concerns.

- Citychamp Watch & Jewellery Group, a holding company with businesses spanning luxury watches, entertainment, and mountain resort services, was the best-performing stock in the S&P Global Luxury Index over the past five days, with shares rising 19. 0% amid improving sentiment toward Chinese consumer spending and optimism around a recovery in luxury demand.

Weaknesses

- Tapestry shares sold off despite the company reporting an earnings beat and raising its full-year outlook, as investors took profits after the stock nearly doubled over the past year. Continued weakness at the Kate Spade brand also weighed on sentiment.

- European retail sales showed further signs of weakness in March, with eurozone retail trade volumes falling 0. 1% month-over-month. Retail sales growth also slowed to 1. 2% year-over-year, reflecting softer consumer demand amid higher energy prices and declining confidence.

- RealReal was the worst-performing stock in the S&P Global Luxury Index, with shares falling about 17. 0% over the past five days after the company reported revenue that slightly missed expectations.

Opportunities

- Growing optimism around a potential easing of Middle East tensions has helped drive oil prices lower and supported a rebound in consumer discretionary stocks. A successful outcome from ongoing negotiations, combined with a sustained reopening of the Strait of Hormuz, could further reduce geopolitical risk and support global equity markets.

- China’s luxury market is showing early signs of recovery during the 2026 Labor Day holiday. Bernstein data showed traffic at luxury malls was 36% above average 2025 holiday levels, while overall holiday consumer sales in China rose 14. 3% year-over-year. Brands including Louis Vuitton, Chanel, Cartier, and Van Cleef & Arpels saw particularly strong traffic growth, with Shanghai remaining the top luxury shopping market.

- Lower oil prices are supporting travel stocks by reducing fuel costs and easing pressure on consumer travel budgets. At the same time, declining geopolitical risk is improving confidence and supporting stronger global travel demand, benefiting premium airlines, hotels, cruises, and experiential tourism. Together, lower energy prices and a more stable geopolitical backdrop are creating a favorable environment for luxury travel and discretionary spending.

Threats

- If energy prices remain elevated, consumer spending and travel demand could weaken ahead of the busy summer season. Higher fuel and transportation costs may discourage leisure travel and airline bookings, while persistent inflation could pressure discretionary spending on dining, retail, and entertainment.

- Three passengers died during a 42-night Dutch expedition voyage aboard the MV Hondius following a hantavirus outbreak among travelers. The ship, carrying about 170 passengers and crew, departed from Ushuaia, Argentina, traveled through Antarctica and remote South Atlantic islands, and was en route to the Canary Islands. Health officials believe the rare virus may be linked to rodent exposure during excursions in South America, while investigations remain ongoing.

- The EU is expected to release updated GDP data next week showing continued weak economic growth. Analysts forecast eurozone GDP growth of approximately 0. 1% quarter-over-quarter and 0. 8% year-over-year for the first quarter of 2026, reflecting soft consumer demand and slowing industrial activity.

Energy and Natural Resources

Strengths

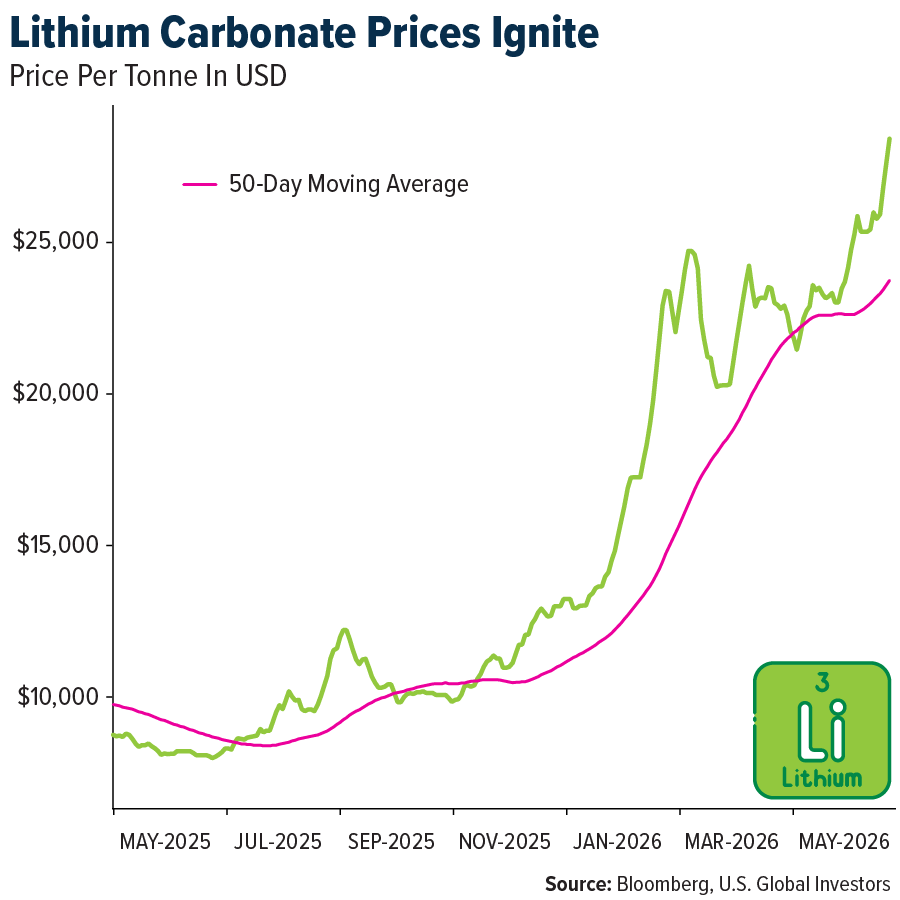

- The best-performing commodity for the week was lithium carbonate, rallying 9. 14%. Albemarle said lithium demand is up 37% this year, tracking near the high end of its forecast as energy storage deployments more than doubled and offset softer EV sales in key markets. Growth is also becoming more geographically diverse, with emerging markets such as Brazil, India, and Australia posting strong gains alongside continued expansion in Europe.

- Ontario Power Generation placed a 953 tonne foundation module 35 metres underground at the Darlington site, marking a major construction milestone for the first small modular reactor to be built in a G7 country. The GE Hitachi BWRX, 300 project, supported by more than 100 Canadian companies, remains on track to connect its first unit to the grid by the end of 2030. The milestone reinforces the broader global nuclear buildout narrative as India advanced construction on Kudankulam units 5 and 6, while Poland confirmed site suitability for its first nuclear power plant using three Westinghouse AP1000 reactors.

- The IEA warned the Iran conflict continues to disrupt roughly 14 million barrels per day of global oil supply. U. S. oil exports climbed to a record high last week as importing nations increasingly turned to American supply amid Middle East shortages, while OPEC+ announced a largely symbolic 188,000 barrel per day output increase for June, signaling continued production discipline even as global supply remains constrained by the Strait of Hormuz closure.

Weaknesses

- The weakest-performing commodity of the week was WTI crude oil, falling 7. 15%. The U. S. is reportedly expecting a response from Iran to President Trump’s proposal that would reopen the Strait of Hormuz in exchange for lifting the American blockade on Iranian ports, potentially ending the 10 week conflict that has disrupted energy markets. However, renewed clashes, including U. S. airstrikes on Iranian oil tankers and Iranian missile strikes on the UAE, continue to strain the ceasefire despite ongoing diplomatic efforts through Qatar and ahead of a planned Trump Xi summit in Beijing.

- Sherritt International shares plunged as much as 30% after the company suspended direct participation in its Cuban joint venture operations following new U. S. sanctions targeting foreign companies in Cuba’s metals, mining, and energy sectors. The company’s 50% stake in the Moa nickel cobalt joint venture and one third interest in Energas now face significant uncertainty, while its Fort Saskatchewan refinery is expected to exhaust existing Cuban feedstock by mid June. Three board members also resigned simultaneously.

- Indonesia’s government proposed raising royalty rates on copper, gold, and tin to support President Prabowo’s welfare programs, with copper concentrate rates potentially rising to 9% to 13%. The announcement pressured mining stocks and pushed Indonesia’s benchmark index down 2. 9%, while raising renewed concerns about resource nationalism in Southeast Asia’s largest economy amid elevated global cost pressures and geopolitical risk.

Opportunities

- The USGS estimated there are 2. 3 million metric tons of economically recoverable lithium in Appalachian pegmatite formations across Maine, New Hampshire, and North Carolina, equivalent to roughly 328 years of U. S. lithium imports at 2025 levels. The discovery strengthens the case for domestic supply chain independence, although lengthy federal permitting timelines, averaging 36 months, have already forced the cancellation of two pilot projects.

- Mexico plans to invest 140 billion pesos, approximately $8 billion USD, in new gas pipelines over the next four years as part of a broader effort to meet rising electricity demand, which could increase by as much as 65 gigawatts by 2030. Most projects are aimed at expanding Mexico’s domestic network, while the Naco, Hermosillo, Guaymas pipeline will increase natural gas imports from the U. S. Mexico is also investing about $8 billion in solar and wind energy projects.

- Zhejiang Huayou Cobalt plans to acquire Atlantic Lithium for $210 million, advancing development of Ghana’s first lithium mine. Atlantic owns the Ewoyaa project, and if completed, the deal would place another major African lithium asset under Chinese control alongside existing investments in Mali, Zimbabwe, and Congo. The all cash offer represents a 26. 6% premium to Atlantic Lithium’s last Sydney closing price and follows a more than 50% rise in lithium prices this year amid global supply concerns.

Threats

- The U. S. , Iran conflict entered its tenth week with no resolution despite a U. S. proposal, delivered through Pakistani intermediaries, aimed at ending the conflict and reopening the Strait of Hormuz. Tehran said it is reviewing the proposal, but renewed clashes, including U. S. defensive strikes and intercepted Iranian attacks near the strait, continue to threaten diplomacy. The IEA warned the conflict is still disrupting roughly 14 million barrels per day of global oil supply and said any recovery in production would likely be gradual due to infrastructure damage and tanker insurance concerns.

- A subsidiary of China Railway Group is proposing a major new copper mine in Congo’s Kasai, Oriental province with potential output of 200,000 to 500,000 tons annually, which would rank among the world’s largest copper operations. The project highlights intensifying U. S. , China competition for Congo’s mineral resources as Beijing continues expanding its investments across Africa’s Copperbelt despite Western efforts to diversify supply chains.

- A GAO report found the DOE’s Office of Environmental Management faces more than $1. 5 billion in repair needs across roughly 4,300 facilities at 15 nuclear waste cleanup sites. Maintenance spending has risen 80% since fiscal year 2020 to more than $950 million in fiscal year 2026. The report highlights aging waste infrastructure as a growing challenge for the U. S. nuclear industry, competing for the same workforce and funding needed for new reactor development.

Bitcoin and Digital Assets

Strengths

- The rapid expansion of crypto exchange-traded funds continues to reinforce institutional adoption and the integration of blockchain technology into traditional capital markets. 21Shares launched the first U. S. ETF providing direct exposure to Canton Coin through the Nasdaq-listed TCAN fund, expanding crypto investment products beyond Bitcoin and Ethereum. The Canton Network, a blockchain platform designed for institutional finance, is backed by major firms including Goldman Sachs, Microsoft, and DTCC. The launch also reflects a more crypto-friendly U. S. regulatory environment, accelerating the development of tokenized financial infrastructure and institutional blockchain adoption.

- Morgan Stanley is expanding its push into digital assets by rolling out crypto trading on its ETrade platform, further integrating cryptocurrencies into mainstream wealth management services. The pilot program charges transaction fees of roughly 50 basis points, below competitors such as Coinbase, Robinhood, and Charles Schwab, while potentially giving crypto access to ETrade’s 8. 6 million customers later this year. Morgan Stanley is also expanding into Bitcoin ETFs, digital asset custody, and tokenized equities infrastructure, underscoring how major financial institutions continue integrating crypto services into traditional banking and brokerage platforms.

- Kalshi, a U. S. -regulated prediction market platform where users and institutions trade contracts tied to real-world events such as elections, economic data, and macro outcomes, raised $1 billion in funding at a $22 billion valuation, highlighting accelerating institutional adoption of event-based financial products. The funding round included investors such as Sequoia Capital, Andreessen Horowitz (a16z), Morgan Stanley, and ARK Invest. Kalshi said institutional trading volume surged roughly 800% over the past six months, while annualized trading activity reached approximately $178 billion. The rapid growth underscores rising institutional interest in prediction markets as tools for trading, hedging, and expressing macroeconomic views across both crypto and traditional finance.

Weaknesses

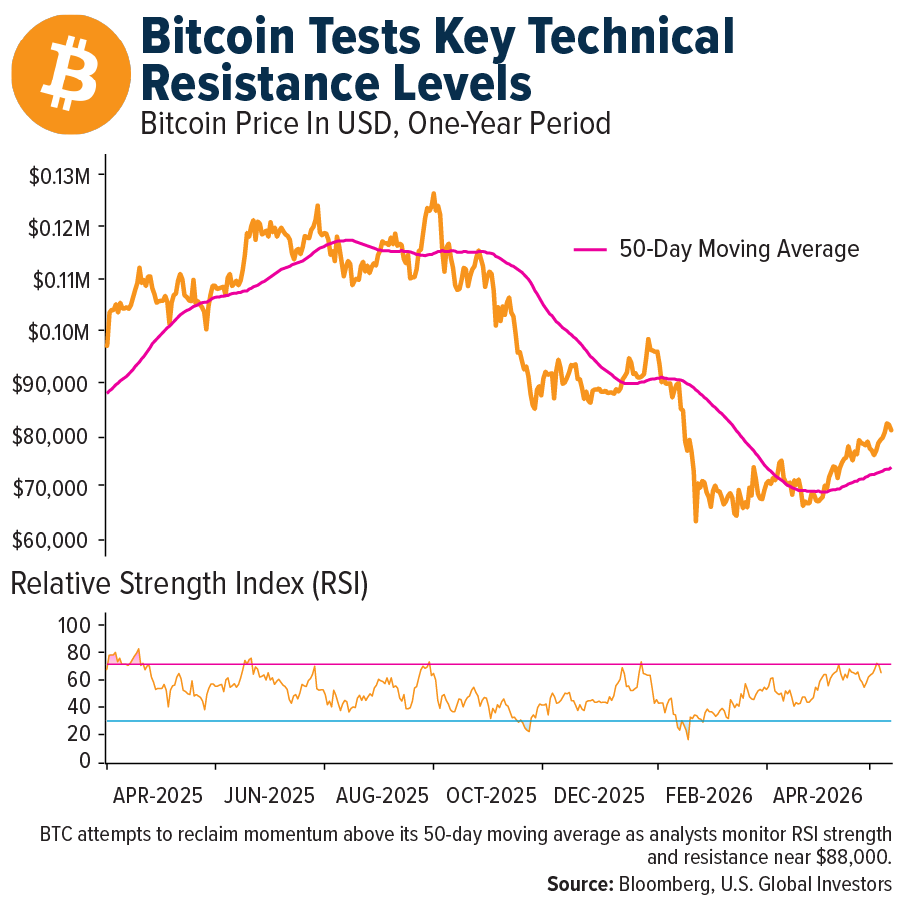

- Strategy, formerly known as MicroStrategy and the world’s largest corporate holder of Bitcoin, is signaling a potential shift away from its long-standing “never sell” Bitcoin strategy as financial pressures increase. The company reported a $12. 5 billion net loss in the first quarter following Bitcoin’s early-year decline and disclosed it may sell BTC to manage debt obligations or improve shareholder returns. Strategy currently holds 818,334 BTC worth approximately $61. 8 billion, representing nearly 4% of total Bitcoin supply, while maintaining a $2. 25 billion U. S. dollar reserve for dividends and debt payments. The move raises concerns about the sustainability of highly leveraged Bitcoin accumulation strategies during periods of volatility.

- Coinbase announced it will reduce its workforce by approximately 14%, or about 700 employees, as the company responds to ongoing crypto market weakness and increasing pressure to improve efficiency through artificial intelligence. CEO Brian Armstrong said the restructuring is intended to help reposition Coinbase as a “lean, fast, and AI-native” company. The cuts come as Bitcoin remains down roughly 6% year-to-date and Coinbase shares have fallen about 12% over the same period. The layoffs highlight continued earnings pressure across the crypto industry as exchanges shift toward more disciplined and cost-efficient operating models.

- Bitcoin’s recent recovery rally continues to face significant technical and structural resistance, raising concerns that the market may not have established a durable bottom. Analysts at Glassnode said BTC must reclaim and hold the $88,000 level to confirm a stronger recovery trend, while long-term holders are currently realizing approximately $180 million in profits per day, increasing potential sell pressure. At the same time, realized losses remain elevated near $479 million daily, more than double the historical cycle baseline of $200 million, signaling ongoing market stress and fragile investor sentiment. Analysts warned that failure to sustain momentum above key resistance levels between $85,000 and $88,000 could trigger renewed volatility across the broader crypto market.

Opportunities

- Amazon Web Services partnered with Coinbase and Stripe to enable AI agents to execute payments using USDC stablecoins, advancing the “agentic economy. ” Through its Amazon Bedrock AgentCore Payments platform, AWS will allow autonomous AI agents to make real-time micropayments for APIs, digital services, and web content using blockchain-based rails powered by Coinbase and Stripe wallets. The initiative underscores growing adoption of stablecoins as programmable payment infrastructure for AI-driven and machine-to-machine transactions.

- The expansion of tokenized investment products continues to drive institutional adoption of onchain capital markets. Bitwise Asset Management, with approximately $11 billion in assets under management, will take over Superstate’s $267 million tokenized Crypto Carry Fund. The strategy uses crypto cash-and-carry trades to generate yield while leveraging blockchain infrastructure for 24/7 trading, transparency, and efficiency. The move highlights rising demand from institutional and crypto-native investors for tokenized financial products.

- Payward Inc. , parent of crypto exchange Kraken, acquired Hong Kong-based Reap Technologies for $600 million to expand stablecoin payment infrastructure in Asia. The deal values Payward at approximately $20 billion and follows recent acquisitions including NinjaTrader and Bitnomial. Reap connects traditional banking systems with stablecoin-based cross-border payments, reflecting growing institutional demand for blockchain-powered financial services and continued convergence between traditional finance and crypto infrastructure.

Threats

- The collapse of Polish crypto platform Zondacrypto is intensifying regulatory and reputational risks for the digital asset industry in Europe. The exchange, which reportedly raised nearly $100 million from Polish investors through aggressive marketing and sponsorships with clubs such as Juventus FC and AS Monaco, is now under fraud investigation after suspending withdrawals. The scandal has triggered political backlash in Poland, with Prime Minister Donald Tusk alleging possible links to Russian organized crime and criticizing delays in Europe’s MiCA crypto regulations. The case highlights how weak oversight and political pressure could slow crypto adoption across Europe.

- Binance is facing renewed regulatory scrutiny after reports that more than $1 billion flowed through the platform to Iran-linked entities during 2024 and 2025, raising concerns over sanctions compliance and anti-money laundering controls. The U. S. Department of the Treasury has reportedly demanded full compliance with the independent monitoring program imposed after Binance’s 2023 guilty plea involving sanctions and AML violations. The exchange previously agreed to pay over $4 billion in penalties and operate under a multi-year compliance monitor. The case underscores persistent regulatory and geopolitical risks for major crypto exchanges.

- Germany is considering major crypto tax reforms starting in 2027 that could eliminate its one-year tax-free holding exemption for Bitcoin and other digital assets. The proposal is part of a broader plan to raise about €2 billion ($2. 3 billion) in tax revenue and strengthen oversight under the EU’s DAC8 reporting framework. Industry participants warn the change could weaken Germany’s position as one of Europe’s most crypto-friendly jurisdictions and push activity toward offshore markets. The move reflects increasing fiscal and regulatory pressure on digital assets across Europe.

Defense and Cybersecurity

Strengths

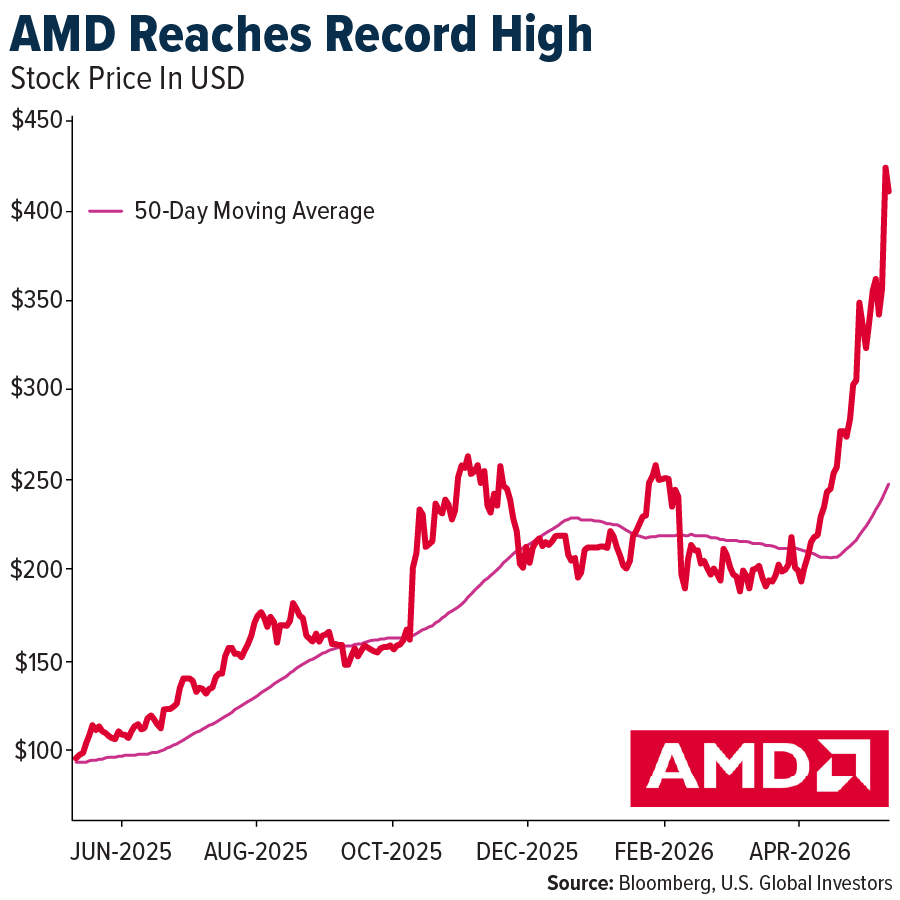

- AMD reached a record high after projecting second-quarter revenue of $11. 2B, driven by strong AI data center demand from hyperscalers such as Google and Amazon seeking alternatives to Nvidia. Despite a potential slowdown in the PC market due to memory shortages, the company expects data center CPU revenue to grow more than 70% this quarter as it scales capacity to meet accelerating demand.

- Lumentum delivered an exceptional fiscal third quarter 2026 report, with revenue surging 90% year-over-year (YoY) and 21. 5% quarter-over-quarter to a record $808. 4M. Non-GAAP EPS rose 316% YoY from $0. 57 to $2. 37 and increased 42% from the prior quarter’s $1. 67. Driven by strong AI and cloud infrastructure demand, the company issued fourth quarter guidance above expectations, with Wall Street estimates at roughly $805M in revenue and $2. 27 EPS.

- The U. S. State Department cleared over $8. 6B in emergency arms sales to several Middle Eastern allies, including Patriot missile defense systems and Advanced Precision Kill Weapon Systems, supporting demand for Lockheed Martin’s advanced munitions and air defense offerings.

Weaknesses

- Amprius conducted a significant balance sheet cleanup, paying $20. 6M to terminate costly lease obligations and eliminating $30M in future liabilities as it pivots toward a leaner, contract-based manufacturing model. Despite record-breaking revenue and a $500M contract pipeline, shares fell more than 25% in a single day as investors raised concerns that the remaining $62M in cash may be insufficient to fund execution without additional shareholder dilution.

- A critical vulnerability (CVE-2026-0300) in PAN-OS allows unauthenticated remote code execution on PA-Series and VM-Series firewalls and is already being actively exploited. Security patches are scheduled, with fixes planned between May 13 and May 28, 2026.

- An explosion at a Safran factory in Blagnac, France, injured two people and prompted an evacuation. Authorities have launched an investigation into the cause of the blast at the aerospace and defense manufacturing site.

Opportunities

- Anthropic’s deal with SpaceX to utilize more than 220,000 Nvidia GPUs at the Colossus 1 data center strengthens Nvidia’s position in AI infrastructure, while AMD’s collaboration with OpenAI and others on a new AI networking protocol aims to improve performance in large-scale AI clusters.

- The Pentagon is expanding the use of artificial intelligence across warfighting, intelligence, and enterprise operations through new agreements that bring frontier AI systems into classified networks. Eight companies were selected for the program, including OpenAI, Google, Microsoft, Amazon Web Services, Oracle, Nvidia, SpaceX, and AI startup Reflection, combining major providers with emerging players.

- Alphabet is set to significantly expand its AI capabilities through a $200B investment involving Anthropic’s use of Google Cloud, while also committing up to $40B into Anthropic, marking a major strategic move in the AI sector.

Threats

- Russia issued a warning urging all nations to withdraw their diplomats from Kyiv, citing expectations of a Ukrainian attack on Red Square during May 9 Victory Day. Russia also stated that if such an attack occurs, it would respond by striking Kyiv’s city center.

- A ceasefire between Iran and the U. S. is under strain as both sides exchanged fire over the strategic Strait of Hormuz, with the UAE reporting attacks for the first time since the truce was declared nearly a month ago.

- A legal dispute has emerged between Lockheed Martin and Northrop Grumman as they trade filings with the FTC over control of the solid rocket motor supply chain. The conflict risks worsening existing production bottlenecks for key missile systems and could weigh on revenue growth for defense sector holdings.

Gold Market

This week gold futures closed the week at $4,732. 70, up $88. 20 per ounce, or 1. 90%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 8. 15%. The S&P/TSX Venture Index came in up 0. 27%. The U. S. Trade-Weighted Dollar fell 0. 27%.

Strengths

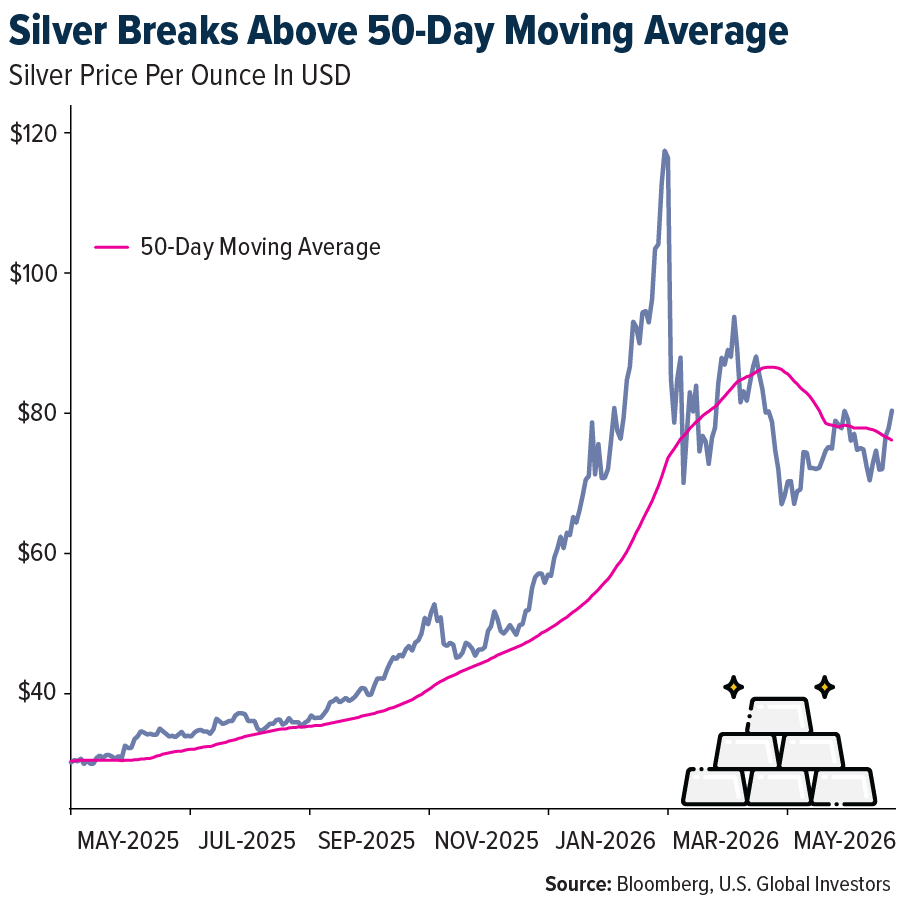

- The best-performing precious metal for the week was silver, up 6. 00%. Silver futures surged to an intraday high of $82. 16 per ounce on Friday as hopes for a U. S. –Iran peace deal and the potential reopening of the Strait of Hormuz lifted precious metals for a fourth straight session. In addition, rising demand for solar power to offset higher energy prices has pulled forward demand for silver.

- According to Scotia, SSR Mining reported first quarter 2026 results with adjusted EPS of $1. 15 versus consensus of $0. 84, on production of 109. 9K ounces versus an estimate of 107. 7K ounces, at all-in sustaining costs of $2,433 per ounce.

- According to BMO, Torex’s first quarter EPS beat expectations, with costs coming in below forecasts and free cash flow of $157M exceeding the $133M estimate. The company also announced an enhanced capital returns program, targeting $350M in shareholder returns in 2026, returned $121M in the first quarter, and increased its dividend by 7%.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 2. 88%. Palladium continued to face headwinds as ETFs shed another 366 troy ounces, extending a year-to-date decline of 9. 3% in fund holdings to just over 1 million ounces. Supply-side pressures also weighed, with Zimbabwe’s largest PGM producer, Zimplats, reporting a 56% quarter-over-quarter decline in total 6E production, including a sharp drop in palladium output to 29,694 ounces after a prolonged smelter shutdown. However, roughly 63,000 ounces of accumulated concentrate stocks are expected to be processed by December.

- Gold declined earlier in the week as escalating Middle East tensions threatened a ceasefire between the U. S. and Iran, keeping energy prices elevated and fueling inflation risks. Bullion fell as much as 2. 4% after reports that the United Arab Emirates’ air defense systems were responding to a missile threat from Iran, while Tehran warned it was tightening control over the Strait of Hormuz, according to Bloomberg. Gold later recovered as interest rates moved lower and geopolitical tensions eased.

- Two contractor employees at Sibanye-Stillwater’s Kloof 8 shaft near Glenharvie, South Africa, died when an inspection platform detached and descended uncontrollably down the shaft during preparations for a routine inspection on May 3.

Opportunities

- China is set to ease licensing rules for gold imports and exports to facilitate trade, according to an announcement by the People’s Bank of China and the General Administration of Customs. The move will expand the use of “multi-use permits” for importing and exporting gold starting June 1, according to a notice published on April 30.

- Australian gold producers Regis Resources and Vault Minerals agreed to merge in an all-scrip deal to create a combined entity valued at around A$10. 7 billion ($7. 67 billion). Under the proposal, Regis will acquire all shares in Vault by offering 0. 6947 Regis shares for each Vault share, implying a deal value of A$5. 15 billion, according to UBS. Vault shares rose 9% on the announcement.

- Tether added 210K ounces of gold in first quarter 2026, down from an average of 700K ounces over the previous two quarters. However, the value of its gold holdings rose to $19. 8B due to higher gold prices, with gold now representing 10. 3% of reserves, up from 9. 0% last quarter, according to Canaccord.

Threats

- U. S. inflation and rising rate expectations have weighed on gold prices, while higher input costs, not just diesel, continue to pressure earnings and cash flow expectations. Last year was not quite a “sell in May” environment, but the gold sector did experience a flat period from June to August as the market digested disappointing fiscal year 2026 guidance, according to UBS.

- Treasuries sold off earlier in the week, pushing 30-year yields to their highest level since July as traders increased bets that the Federal Reserve may need to reverse course and raise rates to contain inflation following a surge in oil prices. Yields rose by at least seven basis points across the curve on Monday, with 30-year yields reaching 5. 03%, according to Bloomberg. However, the move reversed later in the week as expectations for a potential peace deal improved sentiment.

- Orla Mining announced steps it has taken, and is continuing to implement, to safeguard labor rights and address concerns at its Camino Rojo gold mine in Zacatecas, Mexico. This follows a determination by a panel under the Rapid Response Labor Mechanism of the Canada–United States–Mexico Agreement. In late March 2026, the panel issued its final ruling concluding there had been a denial of rights related to freedom of association and collective bargaining at Camino Rojo, according to Scotia.