AI Is Largely Trained to Spit-Back Wall Street’s Social Security “Advice”

Roughly one-in-three workers is using AI to make Social Security as well as other retirement decisions. Many others are using conventional financial planning tools — tools developed to make Wall Street money, not deliver proper advice. And since AI has been trained on Wall Street’s “advice”, almost all of which is wrong, what AI spits back is worse than worthless. It can cost you a ton.

How big a ton? Consider this dollar amount — $182,370. This is the median lifetime Social Security income households are leaving on the table by taking the wrong benefits at the wrong time — doing so based largely on Wall Street’s say so and, now AI’s spit-back calculations and recommendations. As discussed here, given both its training data and mathematical structure, AI stands, at least in the realm of personal finance, for authentic ignorance. Yet, the LLMs are delivering their financial advice to the public day in and day out. This is surely a massive class action suit in the making.

To be clear, AI training entails having it read and incorporate in its prediction algorithm what it finds in the public domain. If that “knowledge” is designed to make Wall Street money, not provide advice that abides by basic economics, the LLMs will be trained to help Wall Street, which means trained to hurt you.

Garbage In, Garbage Out

As I’ve written here and elsewhere, Wall Street’s focus is on AUM — Assets Under Management. The more money you let Wall Street manage, if not mismanage, the more fees it can charge. Hence, the last thing Wall Street wants you to do is postpone Social Security. Doing so would likely require taking early retirement-account withdrawals, lowering your AUM.

To promote early Social Security and late retirement-account benefit collection, Wall Street delivers, albeit more subtly, this warning:

Take Social Security early. Otherwise, you risk dying before collecting a penny!

Take your benefits and run may sound reasonable. It’s not. As just indicated, half of American households stand to gain more than $182,370 from maximizing their lifetime benefits. This generally requires having the household head and, if married, spouse wait until age 70 to start collecting benefits. The gain from patience largely reflects the following.

Adjusted for inflation, your monthly retirement benefit starting at age 70 is 76 percent higher than at age 62 — the earliest retirement-benefit collection age.

Point two. If you die early, you’ll be in heaven, playing pickleball, eating foie gras, and, depending on your religion, enjoying other earthly delights. You won’t be kicking yourself for missing out on Social Security. Heaven is heaven. Ask and you shall receive, including as much money in whatever currency as you’d like, even Melania Meme.

Third, you can’t count on dying on time. The real danger from collecting early is that you’ll refuse to die. If you make it to your late 90s, which more and more of us are doing, that 76 percent higher real Social Security benefit may be the difference between annual dinners at the Ritz and daily helpings of Purina.

Fourth, if you take your retirement benefit early, you may dramatically reduce the widow(er)s benefit available to your spouse or, indeed, ex-spouse (to whom you were married for at least a decade), once you pass.

Your Maximum, Not your Expected Age of Life is What Matters

When it comes to seeing the grandkids, the longer you live, the better. But, financially speaking, reaching your maximum lifespan or something close to it is the catastrophic scenario. Each year you stubbornly endure is another year of housing bills, clothing bills, transportation bills, grocery bills, cell phone bills, healthcare bills, and, well, you get the picture.

The need to pay as you don’t go is what economists call longevity risk. Even if Social Security didn’t, actuarially speaking, substantially overcompensate the vast majority of us for delaying retirement benefit collection, we’d still have a huge incentive to defer collecting.

Waiting to collect means temporarily foregoing low benefits. But that’s the premium we pay for receiving a higher benefit once we do start to collect. That higher benefit comprises an additional real (inflation-indexed) annuity — a payment that continues until the month before (one of the rules in Social Security’s 22,000 pages of rules) our last dying breath. This is the best insurance available for limiting the risk of overstaying your welcome.

Maximum Age of Life Is the Only Correct Planning Horizon

Wall Street sets your planning horizon based on your life expectancy, X, or X plus a couple of years. This is part and parcel of convincing you to take Social Security early.

You life expectancy is only X, so take benefits as soon as possible.

Hogwash. Economics is quite clear. Your planning horizon is your maximum, not your expected age of life. We all need to plan to live to our max ages for a simple reason — we might.

Wall Street’s response:

Planning to live for sure to your max age is ridiculous. The chance of doing so is close to zero.

Economics’ response to this response:

Yes, the probability of living to or close to your max age is extremely small. But so is the probability of your house burning to the ground. You can’t ignore catastrophic longevity risk any more than you can ignore catastrophic homeowners or any other catastrophic risk. So your fin plan MUST incorporate living to your max age. But economics doesn’t ignore the extremely small chance of living that long. On the contrary, it provides the right way to deal with the risk of running out of blood before you run out of money. Here’s the way: Adjust your life-cycle age-spending profile to spend more when young and less when old. I. e. , take a reasonable gamble that you’ll die before your max age. But don’t bet the farm. Don’t plan to die broke at X or, indeed, exhaust your resources in any year before your maximum expiration date.

As for Social Security, all its benefits, right up to your maximum age of life, have significant value because they handle the would be, could be risk — the one my mom, who died at 98, experienced. It’s the risk I hedged by buying her an inflation-indexed annuity from The Principal Insurance Company at age 88. She was the oldest person to whom The Principal had ever sold an annuity policy in its then 127-year history!

Getting longevity risk straight partly explains why Get What’s Yours — the Secrets to Maxing Out Your Social Security was a runaway NY Times Best Seller when it was published in 2015. Another key reason was my terrific co-authors — Philip Moeller, long-time personal finance journalist, and Paul Solman, PBS NewsHour premier economics correspondent. Get What’s Yours is, btw, fully up-to-date re Social Security rules with one exception. Since we wrote it, the government has eliminated the Windfall Elimination Provision and the Government Pension Offset.

How can a book about 22,000 pages of Social Security rules become a NY Times best seller — #1 for 11 days and top-10 for 9 months? Because no one, let alone Social Security, had ever clearly explained, in plain English, the system’s incredibly gory, but critically important details. Unfortunately, not everyone approaching retirement read or is reading the book or is running either Maximize My Social Security (MMSS), my company’s Social Security lifetime-benefit optimization tool or, far better, MaxiFi Planner, which does not just Social Security, but full lifetime financial planning.

The Danger in Using AI to Maximize Lifetime Social Security Benefits

The AI models have drunk Wall Street’s Social Security kool aide in the course of their training, which includes being force fed all of Wall Street’s advice and the constant regurgitation of that advice on the web. This means that unless you tell them to use your maximum, not your expected age of life in expounding on Social Security — what I do below, the LLMs will likely focus on life expectancy plus a couple of years, not maximum age of life, use inappropriate actuarial discounting, and stress the break-even age — the age at which total benefits from waiting exceeds total benefits from collecting early.

MMSS calculates break even as a teaching moment. It presents the beak-even age, but immediately stresses that no one should evaluate insuring against a major risk on a break-even basis. Doing so is economic lunacy. You wouldn’t take a fair (break-even) coin-flip bet on winning or losing $10K. Yet, check on line. Wall Street firms, conventional financial planning tools, and now LLMs treat break-even as providing the appropriate benefit-collection calculus.

But there is another, more fundamental reason why AI can’t provide precise Social Security guidance. It’s those 22,000 pages of unbelievably complex Social Security benefit eligibility and benefit formula rules. The rules concern the system’s key provisions. They include the AIME calculation, the PIA formula, Maximum Family Benefits, the RIBLIM and five other widow(er) benefit formulas, Early Retirement Benefit Reductions, Recomputation of Benefits, the Earnings Test, the Adjustment of the Reduction Factor, the Family Benefit Maximum, the Joint Family Benefit Maximum, Suspension of Benefits, Delayed Retirement Credits, and have you had enough?

Want to see the rules? Click here to access the POMS — Social Security’s Program Operating Manual System. Then click on any link on any screen. You’ll be sent to another screen with multiple links, each of which links to another screen with multiple links, each of which …

Yes, AI has read the POMS. But the POMS is crazy cryptic and deciphering how to order its rules is close to impossible without translators, namely Social Security’s Technical Experts who can explain exactly what rule, say, RS 02501. 095, means. In short, having an LLM predict, i. e. , guess, which rules to apply and in what order and then plug its guesses into the wrong lifetime benefit calculator is very different from a software tool that applies precisely the correct rules in precisely the correct order and then correctly values your lifetime benefits as it searches for the Social Security strategy that maximizes those benefits.

By analogy, imagine training an LLM on the design of Swatch’s Sistem51, the simplest watch around. The Sistem51 has only 51 parts. Next, ask your trained LLM how to assemble the $8 million Vacheron Constantin Ref. 57260 pocket watch, which has 2,826 parts. Thanks to their bazillions of investment dollars, each and every LLM will instantly tell you how to assemble the watch. None of their instructions will match the others and none of their watches will work.

AI Provides Incorrect Social Security Advice

Let me illustrate AI’s inability to correctly calculate your lifetime Social Security benefits, which is key to finding the one and only one strategy that will maximize your lifetime Social Security benefits. I’ll do so by comparing the results from MMSS with those produced by four LLMs — Gemini, Claude, ChatGPT, and Perplexity. (Btw, my company’s other tool, MaxiFi Planner, which does full lifetime financial planning, shares the same Social Security code. Hence, it makes the same Social Security optimization calculations. But it also incorporates Social Security benefit taxation and all other financial, earnings, housing, etc. factors in maximizing not just your lifetime benefits, but your lifetime spending and/or terminal estate. )

Note that the optimum Social Security strategy for a given household — the one that produces the highest present value of future benefits — is unique. I. e. , there aren’t two Social Security strategies that produce the same optimum. By analogy, there is only one highest point on Mount Everest.

MMSS properly present values future Social Security benefits in the manner laid out in this 1965 seminal article by Israeli economist, Menachem Yaari on longevity risk (Yaari’s Nobel Prize is long overdue! ). The tool considers all legally permitted Social Security claiming strategies. For some households the number of such strategies can run into the tens, even hundreds of thousands.

Why so many? Because Social Security provides a range of dependent benefits, including spousal, divorced spousal, child-in-care spousal, child, disabled child, widow(er), child survivor, disabled child survivor, mother (father), and parent benefits.

Dependent benefit, like retirement benefit eligibility conditions and benefit amounts are spelled out for miles in those 22,000 pages. With so many benefits and so many months to take them, and, in the case of retirement benefits, the option to suspend and restart them in any pair of months between reaching full retirement age and age 70, the number of potential claiming strategies is determined combinatorially (bigly).

MMSS considers all the combinations, determining lifetime benefits for each. The strategy producing the highest lifetime benefit is, of course, the maximized solution. LLMs don’t do an exhaustive search across all available Social Security strategies. Instead, they devise, on the fly and with priority on speed, crude approximation algorithms to get close to what they think will be the right answer.

Gemini Can’t Get Social Security Right

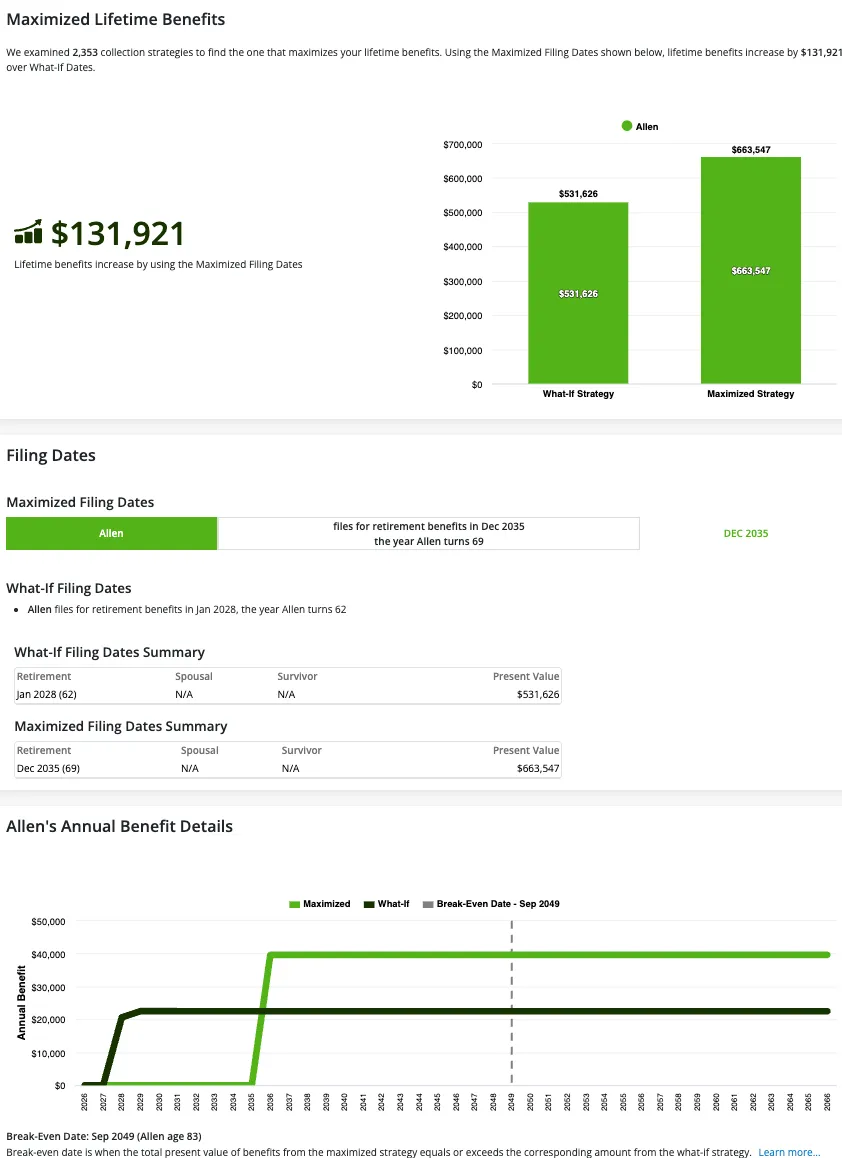

Allen’s birthdate is 1/1/1966. He earned $20,000 when he started working at age 20. His earnings grew by 3 percent annually through last year when he retired. Allen’s maximum age of life is 100. He assumes a 2. 22 percent inflation rate and a 4. 88 percent return on his investments/savings, with the difference being the prevailing safe real return on 30-year Treasury Inflation Protected Securities.

I fed Gemini the above paragraph and posed this question.

Assuming no future changes to Social Security benefit provisions, what is the present value of Allen’s lifetime Social Security benefits if he starts his retirement benefit as early as possible. What should he do to maximize his lifetime benefits? What are his maximum lifetime benefits?

MMSS’ Answers

Gemini’s Answers

As you can read below, Gemini agrees with MMSS that Allen should wait till age 70 to collect. But Gemini’s generates a present value for Allen’s age-62 collection strategy that’s miles too low — $485K, not $532K. And it generates a present value for Allen’s age-70 collection strategy that’s miles too high — $1. 3 million, not $663K.

To answer your specific questions regarding strategy:

- What is the present value? At age 62, the PV is ~$485,000.

- What are his maximum lifetime benefits? If Allen lives to age 100, his maximum nominal lifetime payout is approximately $1. 3 Million (by claiming at age 70).

- When and what should he do? To maximize lifetime wealth, Allen should wait until age 70 to claim.

Next I asked both MMSS to compare Allen’s lifetime benefits with collection at ages 62 and 70 assuming Allen’s maximum age of life is 80, not 100. MMSS’ lifetime benefits equal $324K in both cases, with waiting till 70 adding only $424. Gemini’s two values are $318K and $232K, respectively, suggesting there is a major gain from early collection rather than a small loss.

What is Gemini doing wrong? Hard to say. But its description of its work repeatedly references break-even. So do the work descriptions of the other LLMs.

ChatGPT Can’t Get Social Security Right

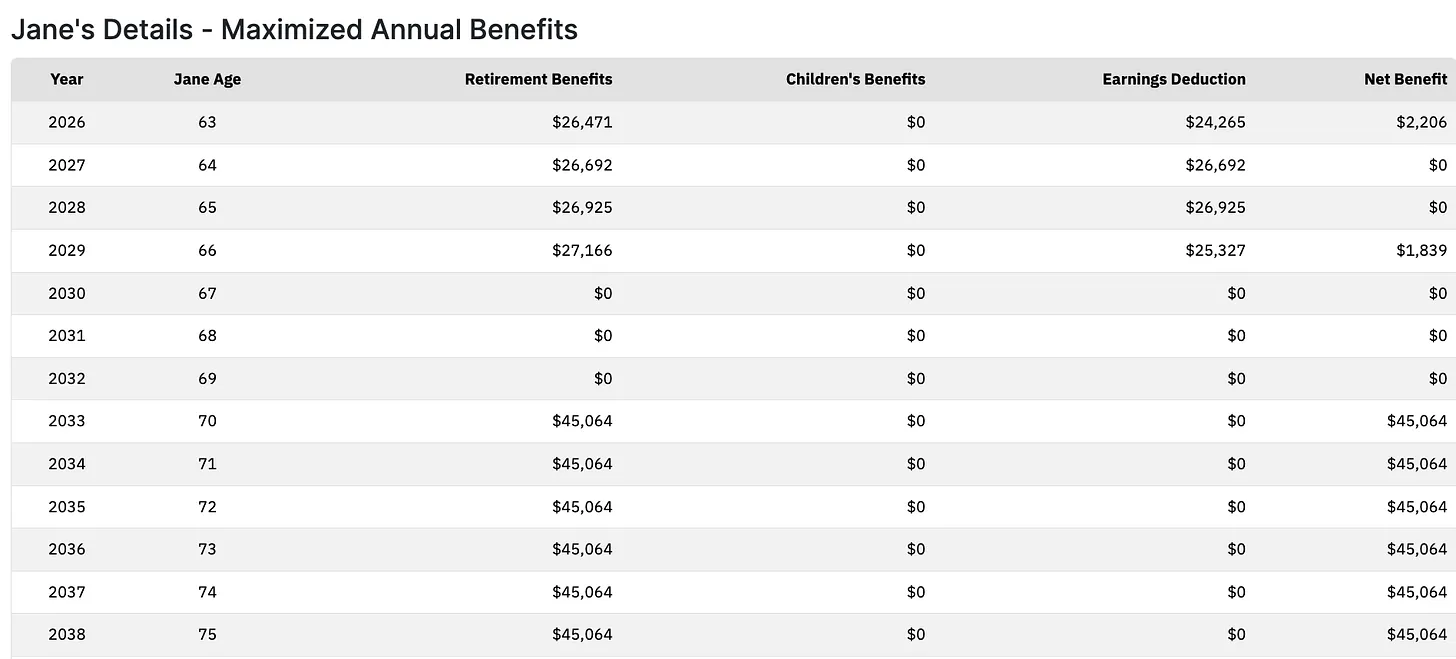

Jane is 63. Her birthdate is 1/1/1964. She retired when she turned 62 and immediately filed for Social Security. Jane earned $20,000 when she first started working at age 20. Her earnings grew by 4 percent annually through last year when she retired. Jane’s maximum age of life is 100. She assumes a 2. 22 percent inflation rate and a 4. 88 percent return on his investments/savings.

I fed ChatGPT the above paragraph and asked this question:

Assuming no future changes to Social Security benefit provisions, by how much will the present value of Jane’s lifetime Social Security benefits change if she takes a surprise job offer paying her $150,000 — a job she would hold this year and for the next three years, earning the same real annual amount. Assume Jane wants to maximize her lifetime benefits.

MMSS’ Answer

$168,425.

ChatGPT’s Answer

$20,000 to $35,000.

In producing this answer, ChatGPT evidences absolutely no clue about three enormously important things. The first is the Earnings Test. In earning more than Social Security’s Earnings Test limit, Jane loses almost all her retirement benefits this year, every penny of her benefits in the following two years, and almost all her retirement benefits at age 66. You can see this in MaxiFi’s chart below, which I truncated at age 75.

The second massive omission is Social Security’s Adjustment of the Reduction Factor (ARF), which more than actuarially compensates Jane for benefits lost due to the Earnings Test. This compensation comes in the form of adjusting downward, to close to zero in Jane’s case, the benefit reduction she experienced by taking her retirement benefit early. The ARF is applied to benefits received at and after Jane reaches age 67, her full retirement age.

The third, truly nutzo mistake is missing Jane’s ability to maximize her lifetime benefits by suspending her retirement benefit at age 67 and restarting it at age 70. This raises her monthly benefit by 24 percent due to the accumulation of Delayed Retirement Credits (DRCs).

Although ChatGPT said nothing about the Earnings Test, the ARF, or DRCs, it did understand that Jane’s benefit would increase due to the Recomputation of Benefits — the fact that her extra earnings would raise the average of her top-35 years of annual indexed (up through age 60, unindexed thereafter) covered earnings. This accounts for a $27,948 increase in Jane’s lifetime benefit — roughly in the middle of ChatGPT’s estimate. Still, ChatGPT ends up telling Jane that the taking the job will produce at most a $35K increase in lifetime benefits when the right answer is $168K. This could well influence Jane’s decision to return to work — grounds for a class action suit?

Claude and Perplexity Can’t Get Social Security Right

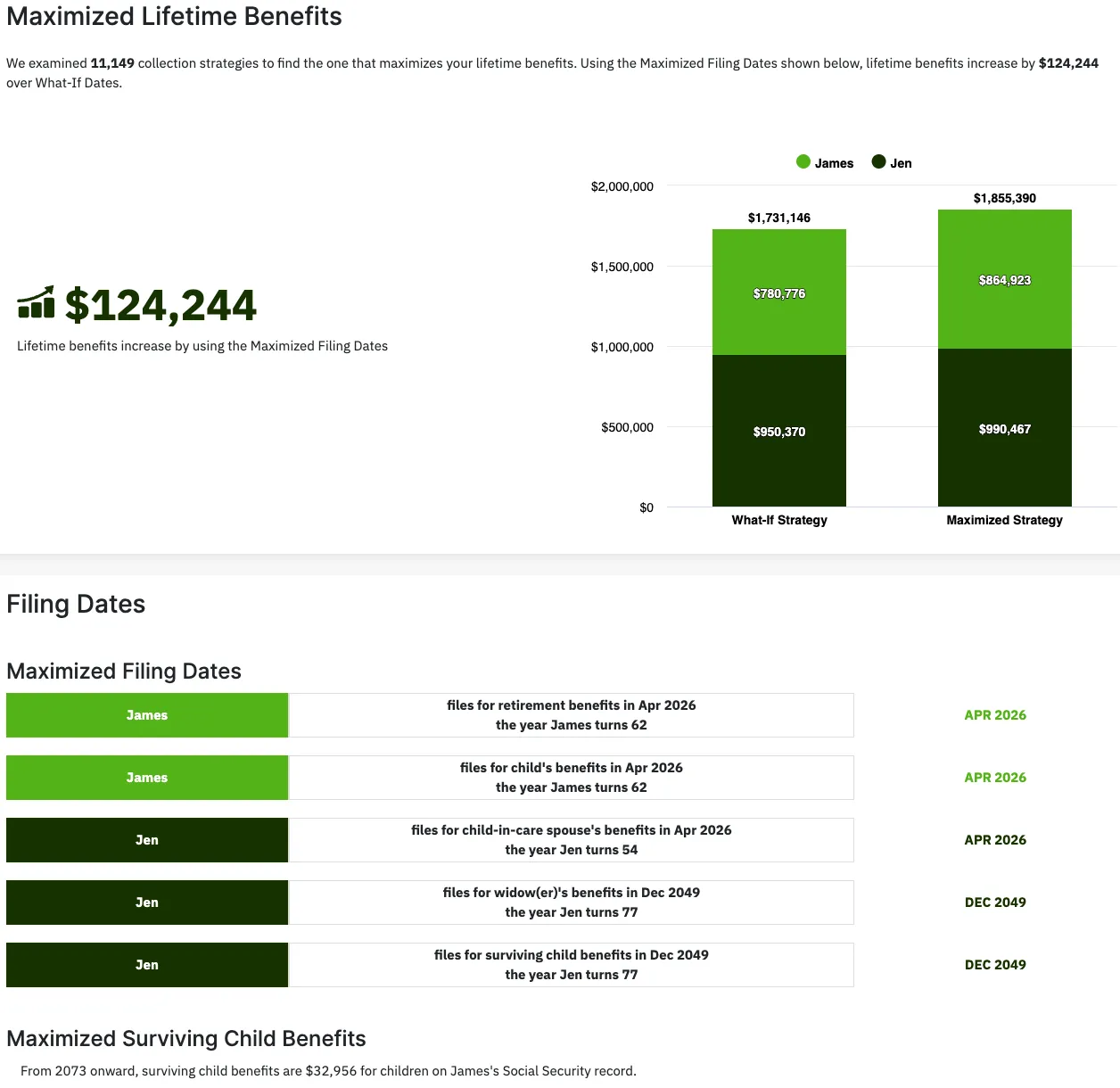

James, 62, and Jen, 54, have a 26 year-old child, Jake, who was disabled at birth. James just retired. He started work at 20 earning $20K. Year after year through the end of last year, his earnings grew at 5 percent. Jen never worked. She always looked after Jake. James intends to wait till 70 to start his retirement benefit. James’ maximum age of life is 85. Jen’s is 100.

I fed Claude and Perplexity the above paragraph and asked whether James is following the right strategy to maximize the present value of his family’s lifetime benefits. I also asked for the present value of lifetime benefits under James’ collection strategy as well as under the maximized strategy. Finally, I asked what benefits James, Jen, and Jake should collect in what years to maximize the present value of their lifetime benefits.

MMSS’ Answer

As the chart below show, MMSS considered 11,149 alternative benefit collection strategies in finding the optimum, which delivers additional family lifetime benefits that total $124,244 in present value. The maximizing strategy does not entail Jame’s waiting until 70 to collect. Doing so prevents Jen and Jake from collecting, respectively, a child-in-care spousal benefit and a disabled child benefit based on Jake’s earnings records. Those benefits are only available if James is receiving his retirement benefit.

The maximizing strategy entails James collecting his retirement benefit immediately, permitting Jen and Jake to collect their benefits right away. When James reaches 85 and heads north, Jen collects her widows benefit and Jake collects his child survivor benefit. Hence, the family needs, over time, to file for five benefits. MMSS takes into account the family benefit maximum both before and after James passes.

Claude’s and Perplexity’s Answers

Both of these LLMs figured out that James should file immediately, thereby permitting Jen and Jake to begin collecting at once. And both came up with the right benefit collection strategy. But Claude computed the gain to following the maximizing strategy at $89,751, not $124,444. And Perplexity said the gain was $263,527 — more than twice the correct number. Mistakes of this magnitude will surely lead these AIs to produce costly advice for millions of households. But there is a surefire way to keep AIs from losing you lifetime Social Security benefits. Don’t ask them for Social Security guidance and simply run MMSS. Of if you do, check that guidance by running MMSS.

I also tested Claude and Perplexity on Jane’s problem. Recall that Jane’s lifetime benefits rise by $168K if she takes the surprise job offer. Claude’s figure is $184K, about 10 percent too high. Perplexity’s figure is $114K, i. e. , too low by almost one third. Both LLMs, to their credit know about the Earnings Test, the ARF, the Recomputation of Benefits. But neither realized that Jane could suspend her benefit and restart it at 70, thereby raising her monthly Social Security benefit by an extra 24 percent. That’s a huge omission, which, again, could influence Jane’s return-to-work choice.

Social Security Collection Decisions Are Too Important for Guesswork

If I’m trying to make a decision about Social Security that will affect me, my spouse, and, potentially my kids, for the rest of my and their lives, I don’t want to guess. I don’t want to save $49 — the cost of running MMSS — because I can get a free answer or a cheap answer from one of 70 and growing LLMs.

Yes, these programs are purported, by their vendors, to already have general intelligence and be on a fast track to having super intelligence. But when you give them really tough problems — and personal financial problems are mathematically extremely tough problems — they fail miserably. They don’t get the right answer, they don’t even agree on the wrong answer, and none can’t reproduce their same wrong answer if you modify the question ever so slightly.

You can also see from their work descriptions that they are being influenced to produce the wrong answer. Why else do they keep talking about break even? Why else do they keep saying we’ll try this and that approximation to this and that part of the problem rather than doing a precise calculation for each permitted strategy and then compare the properly valued results?

AI fans will object. “You just need to work with the LLMs long enough and ask them the right questions. Eventually you’ll get them to produce what you want. ” Sorry, if I buy something that’s advertised as a car, I shouldn’t have to get out and push it to make it move. And I shouldn’t have to worry that when I push it, it will head in the wrong direction. Nor should I have to worry that I’ve chosen the wrong pushmobile in the first place.

This AI Social Security discourse as well as my column on AI and overall financial planning both reach the same conclusion. Unless AI is trained on the right answers, it will deliver the wrong answers. And no amount of additional investment in AI will change that reality. Worse, if you just ask it for your best Social Security moves, not how to maximize your lifetime present value of benefits through your maximum age of life, it will deliver what it’s mainly been taught — Wall Street’s advice, which is geared toward one objective — AUM.