Genuine versus Artificial Intelligence

I recently posted a column entitled Genuine versus Artificial Intelligence on my substack, Economics Matters. It makes two points.

First, LLMs can do conventional financial planning (CP). No surprise. CP is a keep-it-simple sales pitch with a mathematical veneer. It’s not real financial planning — at least not what economics recognizes as such. CP math comprises high school algebra, which can be done by speadsheets. Since LLMs can access spreadsheets, they can do CP instantly, on a 24-7 basis, and for free. Hence, Wall Street’s days may be numbered in using CP to gather AUM (assets under management) on which it can charge fees.

Second, LLMs can’t do economics based financial planning (EBP). Indeed, when it comes to EBP, AI is beyond hopeless. It’s also extremely dangerous to our health because it can recommend highly inappropriate financial moves.

I illustrated this second point in my column. I ran a hypothetical, New Jersey, middle aged couple through my company’s MaxiFi Planner software, comparing it with AI. MaxiFi is 33 years in the making and the only financial planning tool that does economics-based planning in accordance with economics science. Its answers are so different and so valuable compared to CP’s that Wall Street has been forced to take notice. Bankrate just named MaxiFi “the best financial planning software of 2025. ” And MaxiFi is now being taught in top business schools and even high schools.

Let me recap my MaxiFi/AI comparison before turning to the broader question of why AI can’t do EBP and likely never will. To be sure, I’ll provide only one comparison. But discovering e-Coli in a single ounce of ground beef is enough to get the message — Stay Away! Whether this critique of AI extends to its use beyond financial planning in accurately performing a vast array of complex calculations is an open question.

Economics Based Planning vs AI — a Recap

John is 46, Jane 36. They have three young children and live in a costly, heavily mortgaged house. Both draw higher than average salaries, but have very different earnings trajectories. John is self-employed, plans to retire young, and foresees flat real earnings. Jane plans to retire late and anticipates rapid real wage growth. The couple needs to fund three 529 plans, meet John’s alimony payments, and cover out-of-pocket healthcare costs. They have retirement accounts and are both planning to live to 100 for a simple reason — they might. Finally, they want to bequeath their house and, subject to RMDs, a quarter of their retirement accounts.

Yes, this household has lots going on financially and demographically. But every household’s situation is involved once you sweat the details.

To make things easy for AI, I considered a deterministic (no uncertainty) case in which the couple earns a fixed real investment return and projects a constant inflation rate. The couple’s EBP problem, to which there is only one correct answer, involves consumption smoothing, specifically finding the real (measured in today’s dollar) amounts it can spend each year, on a discretionary basis, to produce the highest sustainable living standard per household member while never going into debt.

Safety-first investing is, by the way, the fiduciarially appropriate starting point for financial planning. Taking investment risk, as opposed to investing in TIPS (Treasury Inflation Protected Securities) and other safe assets, is an option, not a starting point. Moreover, if AI can’t get this simplest form of EBP right, its self-proclaimed EBP-based investment “advice” will surely place households at even greater risk.

Discretionary spending references all outlays that aren’t fixed/off-the-top, i. e. , that aren’t taxes, housing costs, special expenses, IRMAA premiums, retirement account contributions, life insurance premiums, and bequests. As for the relationship between discretionary spending and living standard, it accounts for the lower cost of children and economies in shared living.

Consumption Smoothing — Birds Do It, Bees Do It, Even Educated Fleas Do It

Consumption smoothing is basic to animal survival. Squirrels gather acorns in the on season — the spring, summer, and fall — to make it through the off season — the winter. Retirement is our winter. We save when young to spend when old. We do this for a simple reason. The more we consume at a given point in time or over a given period of time, the more satiated we become. Economists call this diminishing marginal utility of consumption. Graphically speaking, the more we stuff ourselves at one sitting, the less the pleasure of the next mouthful. Spending more when young means, of course, spending less when old with each dollar not saved worsening our retirement to an increasing degree. This is the flip side of the satiation coin. Every additional morsel stolen from our plate before we’ve lifted our fork leaves us hungrier — unsated to a greater degree.

Saving — reallocating our acorns from periods that would otherwise feature high spending (periods of satiation) to periods that would otherwise feature low spending (periods of hunger) — makes us feel better, physically. Hence, physiology, not AUM, underlies EBP, including consumption smoothing, insurance acquisition, and portfolio diversification over our life cycles.

Consumption smoothing may seem like a simple problem. Surely, LLMs, which embed tens of billions of dollars of investment and feature up to one trillion parameters — all overseen by the planet’s smartest zillionaires, can correctly solve John and Jane’s consumption smoothing problem.

They can’t. Indeed, they can’t get close.

As I described, Claude recommended discretionary spending that was far too low initially and far too high later in life. It also told John to purchase $1 million less in life insurance than he needed. It overstated — by $108K — John’s present value tax saving from contributing to a Roth rather than a regular IRA. And it understated the couple’s lifetime discretionary spending gains from Social Security benefit optimization by $220K. I could have found any number of additional major mistakes, but once you get a whiff of rotten meat, … .

As for ChatGPT, it said,

“John and Jane can spend approximately:

$52,000 per year in total discretionary spending (real, today’s dollars)”

Perplexity AI said,

“They should target roughly $95,000 of discretionary spending this year (2026) to maintain a smooth living standard per effective household member over their lifetimes, given the described assumptions and constraints. ”

And here’s Gemini’s “advice. ”

“Since Jane’s salary grows faster than inflation and a large gift arrives late in life, the “no debt” constraint is the biggest hurdle. If they spend more than ~$65k now, they risk a cash flow crunch before the mortgage is paid off. ”

AI Has No Real Clue

AI is telling John and Jane that consumption smoothing entails discretionary spending between negative $52K and positive $95K this year. MaxiFi’s demonstrably correct (verifiable by inspecting its reports) answer is $63,382. Claude came in at $53,546 or 16 percent too low. For 2050, Claude recommended discretionary spending that’s 36 percent too high. Gemini got pretty close to the right answer for 2026. For 2050, it was at $64,800 to $80,000 when the right answer is $101,326.

Why Getting Economics Based Planning Right Is So Tough

Cash Flow Constraints

John and Jane, like roughly two thirds of American households, are cash-flow constrained. They can’t borrow against the future — when their kids are out of the house, alimony payments are past tense, a Social Security check shows up every month, and retirement-account withdrawals are available at no penalty.

Cash-flow constraints don’t eliminate the need and desire to consumption smooth. They simply limit the ability to fully do so. Cash flow constraints produce what economists call corner solutions. They transform easy computation problems into nasty ones.

What’s worse, households can be cash flow constrained over multiple periods of their lives. Take John and Jane. They’re cash-flow constrained over six different sets of years reflecting the loosening of their constraints through time. And each constrained interval encompasses a different number of years.

Our Bizarre Fiscal System

Our fiscal system, comprising 500+ federal and state tax and benefit programs, is crazzzy complex. Furthermore, tax and benefit functions (formulas) are non-differentiable, non-convex, and discontinuous. Translation: They’re supremely ugly equations that require special handling. The algorithms required are particularly unusual when it comes to optimal Roth conversion and other tax minimization strategies. Those algorithms weren’t taken off any shelf that a LLM can find in the public domain. They popped out of a human brain — primarily mine — entirely out of the blue over decades, not in nanoseconds.

Simultaneity

With EBP everything depends on everything. For example, a higher path of taxes means a lower affordable path of spending. But this means more saving and, thus, even higher future taxes (due to higher future taxable asset income and/or retirement account withdrawals), which means even lower affordable spending, which means … .

Another example: Higher spending raises insurance needs, which means higher premiums, which means lower spending, which means lower insurance needs, which means … . A third example is withdrawals from retirement accounts, which can trigger higher taxes on Social Security benefits and Medicare Part B IRMAA payments. This translates into a lower lifetime spending plan, which impacts federal and state income tax paths, which impacts taxation of Social Security and IRMAA payments, which impacts … .

In short, EBP is the mother of all chicken and egg problems. The chart at the top shows these interconnections — what economists call simultaneities. The orange block references the household’s living standard. If, as assumed, there are no credit constraints, consumption smoothing entails a stable living standard path through time — the blue line. The white line is an iteration — a step in the process of finding the blue line. But finding that stable path requires incorporating the paths of all the other depicted elements and flipping between them to their unique, joint, internally consistent solution.

If the household is cash-flow constrained, the blue line will be a step function. It will look like a staircase, viewed from the side, with many long treads. But using trial and error to find where the steps occur requires more calcs than there are atoms in the universe. Consequently, using precisely the right algorithms matters.

In addition, the household may want a higher living standard when young, given that the likelihood of reaching its maximum lifespan is so low. MaxiFi also handles this with no sweat. It doesn’t pretend households will die at their life expectancies or shortly thereafter. It conforms with economic theory is treating the planning horizon as the maximum age of life with households being free to take a gamble that they will die before the max age. That gamble entails setting a higher living standard when young at the known risk of a reduced living standard when old.

Internal Consistency

When it comes to our financial lives, changing anything changes everything. EBP takes this into account. As for CP, it’s Set It and Forget It. Once the client’s retirement spending target is set, it’s locked or modified according to some arbitrary guardrail formula. This is why CP is so far off the mark and so easy for AI to replicate. MaxiFi, in contrast, won’t produce results unless what it puts in (calculates for) any of the boxes in the chart is fully consistent with what it puts in (calculates for) all the other boxes.

Solving EBP’s Jigsaw Puzzle — Advanced Algorithms, Not Crude Approximations

MaxiFi’s computation engine is chock full of sophisticated, interdependent, proprietary algorithms. Its engine can be compared with Vacheron Constantin “Les Cabinotiers Berkley Grand Complication” pocket watch. The Grand Complication has 2,877 moving parts, comprising the world’s record. If one part fails, the entire watch stops.

No one would think that the thousands of moving parts of a Porsche engine could be used to build The Grand Complication. Yes, both have parts and both have parts that move. But that’s where the overlap begins and ends. Hence, I find it passing strange that AI companies believe their neural networks, which have mathematical functions, but whose functions bear no mathematical relationship to MaxiFi’s algorithms, could crack EBP. Yet, in providing their answers, each LLM I’ve used asserts it can do EBP without so much as a disclaimer. (My preferred disclaimer — Run MaxiFi to check my advice. )

Systematic Hallucination Is a Feature, Not a Bug

The Financial Times just reported that AI hallucination is the main concern of 27 percent of AI users. AI companies say, “Not to worry. We’re fixing them. ” But we need to worry. If AI is getting John to buy half the life insurance he needs (Claude’s recommendation) and John gets run over by a bus, AI’s hallucination is no joke.

Unfortunately, the word hallucination doesn’t convey the problem with AI’s guessing game. It suggests making honest errors on both sides of the right answer. AI isn’t making random errors with respect to EBP. It’s making, as John and Jane’s case shows, massive systematic mistakes. Indeed, each LLM is making its own, quite different systematic EBP mistakes with no means of fixing those mistakes.

The reasons are simple. LLMs don’t have the right training data to correctly predict what MaxiFi will generate. They’d have to run MaxiFi a massive number of times for millions of hypothetical households to reasonably estimate MaxiFi’s answers. As for AI’s grabbing the wrong algorithms from off the public domain shelf, AI is attempting to directly do EBP but with the wrong math. Indeed, the LLMs are even grabbing simplistic CP rules of thumb dumb, which are guaranteed to contradict EBP.

Troubles With AI

AI is or will be, we’re told, not one ring to rule them all but one set of coefficients and functions to know it all. Supposedly, if you build an LLM big enough, it will hone in on precisely the right answers to any question. Indeed, it will supposedly morph from AI to ASI — artificial super intelligence.

There is no denying AI’s value. Perplexity instantly told me about that the fastest commercially sold car is the Nevera, which can go zero to 60 in 1. 74 seconds. I wanted to compare this speed with MaxiFi’s internal computation time. The Nevera takes a second longer to reach 60 mph than MaxiFi takes to internally generate its results. (MaxiFi does need another 4. 5 seconds to display its answers. ) Even better, Perplexity told me the source of its answer letting me check it wasn’t making things up.

But, a week back, when I asked Perplexity if my well laid and fully paid sabbatical travel plans were going to violate the Schengen visa restrictions, it scared the hell out of me. It said absolutely I was going to violate EU rules and then explained, in detail, how I could change my plans to get good with EU law. This put me in a panic until I realized Perplexity was wrong. I then found myself telling Perplexity about its mistake. What followed was a tender moment in which Perplexity conveyed a series of abject apologies while asking for partial credit. It explained that it got X wrong, which led it to get Y wrong, which led it to get Z wrong. I told it that it sounded like my undergrads. I also told it to raise another $100 billion and see if it can do better.

Since LLMs/AIs aren’t being trained using MaxiFi, they have no way to properly guess correct financial planning answers. Yes, AIs can instantly try algorithms they know, coding them up in real time in Python to pretend they understand what they’re doing. But guessing, in seconds, advanced, proprietary (trade-secreted) algorithms, algorithms that took decades to develop and test, let alone applying them in the right order, is prayer masquerading as hubris.

Limits to Approximation/Prediction

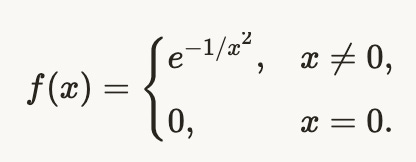

We know from mathematics that even infinite approximation with infinite amounts of correct data won’t necessarily produce the right answer. In 1715, mathematician Brook Taylor developed the Taylor Theorem, which is taught in high school calculus. It says that any nicely behaved mathematical function can be approximated precisely starting from given points, but not necessarily from all points.

A standard example is the bump function shown below (Ignore this paragraph if you are a long way from high school calculus or never took it. ) For any value of x that’s not zero, you can get infinitely close to f(x), i. e. , to the right value, by starting from a different value, call it a, and applying Taylor’s rule with ever higher degrees of approximation.

But if you try to approximate the value of f(x) starting at a equal to zero, forgetaboutit. The further x is from zero, the worse the approximation regardless of how hard you approximate — how many Taylor terms you add to the approximation.

This is one insight into the innate limitation of approximation. Another, as economists and statisticians have long identified, involves overfitting data. The lesson here is that using more mathematical structures to fit the data can worsen predictions. Sure enough, AI engineers have run into this “overfitting” problem as they layer more and more layers on their neural networks.

A third issue involves fixing the prediction of X at the cost of worsening prediction of Y. Every time an LLM is fed new data (not necessarily correct data, btw), all of its parameters change. Yes, AI engineers can control such changes, but these “controls” are arbitrary — just trial and error. The basic point is that knowing more about one thing leads, inexorably, to learning less about another. This is Heisenberg uncertainty principle applied to AI! It also applies to ASI potentially finding algorithms, at random, to do EBP.

Bottom Line

AI is here to eat CP’s lunch and that of all the financial planners and companies providing CP. But AI can’t touch EBP. Want more proof than I’ve provided? Just grab a copy of MaxiFi, run your household or client through the program, and then enter the same inputs you gave MaxiFi into your favorite LLM. You’ll smell what I smell.

But the industry’s fundamental problem goes far deeper than AI. The industry, as a whole, is selling hope, not doing real, fiduciarially appropriate financial planning. There’s a reason no top finance department in the country or, indeed, the world, teaches CP. Its doesn’t accord with the behavior of a squirrel let alone a century of personal financial theory developed by a Who’s Who of the giants who founded the field of finance.

In short, this is the time for the industry to come clean and start doing proper economics based financial planning. Financial planners will be able to sleep at night knowing their jobs are secure and that they are finally acting in their clients’ best interests.

Is there A Broader Message Here About the Hyping of AI and its Market Valuation?

Upwards of $2 trillion has been invested in AI companies over the past five years. And upwards of a quarter of the current historically high stock market appears to be AI based. To be clear, the above two sentences were informed by AI queries. Being able to instantly access global information in a far more efficient manner than engaging in successive internet searches is making me and, I’m sure you, more productive. So is being able to have AI do quick and easily checked calculations without having to program them from scratch.

But do these reflect one-time productivity improvements or ongoing improvements? The later, indeed, the latter in spades, is what’s needed to justify market valuation of AI. AI’s abject failure to handle EBP should give one considerable pause about the following statements.

- Sundar Pichai (Google): AI is “one of the most profound” things humanity is working on, “more profound than fire or electricity,” and “the most profound shift of our lifetimes,” bigger than mobile or even the internet.

- Sam Altman (OpenAI): AI “will be the most powerful technology ever created by humanity” and could be “the biggest, the best, and the most important” of the technology revolutions.

- Jensen Huang (Nvidia): AI is “the most powerful technology force of our time,” and we are “living in the age of AI” where it will transform essentially every industry.

These statements are, of course, self interested. All three of these sounding boards have vast fortunes riding on their wishes coming true or, at least, others literally buying their hype. If AI can’t get small things, like Schengen visa rules, right and it can’t get big things, like how much insurance you need right, at this stage of its game, then its promise may be far less than advertised. As the old saying goes, one picture tells a thousand words. What’s clear from the abject failure of AI to do EBP is that complex calculations involving sophisticated algorithms are far beyond its capacity. Hence, its current ability to take over the multitude of industries and processes that are based on such algorithms appears non existent. Yes, AI can assist, but it can’t yet, and likely never will be able to lead. And its assistance may be primarily cosmetic. For example, AI’s best hope of providing accurate economics based planning is by serving as a front end in guiding data and using MaxiFi as a back end to produce precisely correct, not clearly pretend results.