I just returned from the Investment U conference in Las Vegas, where I presented on gold and the great digital transformation. Sentiment among investors was upbeat, despite great uncertainty in the world right now.

As you know, card counting is banned at blackjack tables. The casinos don’t want gamblers using probabilities to tilt the odds in their favor.

In the stock market, though, applying math, standard deviation and mean reversion to your investment decision is perfectly legal. In fact, I’d argue it’s essential.

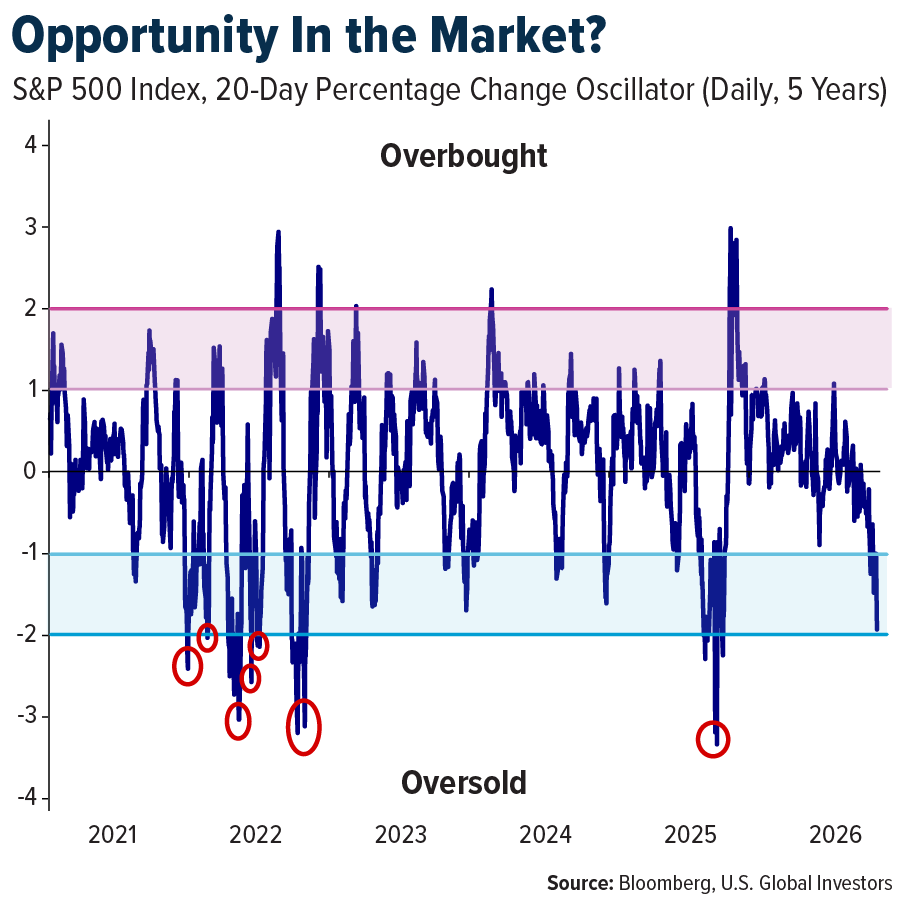

Take a look at the chart below. It shows the S&P 500’s 20-day percent change expressed in standard deviation terms over the past five years. As you can see, the market has just fallen to -2 sigma, deep into oversold territory.

That’s a level the S&P has touched only about five or six times in the past five years. And every single time, it was followed by a recovery.

The bounce doesn’t always come overnight, of course. In the worst case, during the spring of 2025, the market stayed below -2 sigma for more than a month, from mid-March through late April. The 2022 selloffs showed a similar pattern, with oversold conditions lasting roughly 30 days before reverting to the mean.

The point I’m making is that they did move back to the mean eventually. Markets don’t stay at extreme levels forever.

None of this guarantees the exact timing of a reversal. But history suggests the probabilities right now favor a move higher, and, as I’ve been saying all along, I believe investors who stay disciplined will be rewarded.

The 106-Year-Old Law Holding Back American Energy

Last Friday, the Department of Homeland Security (DHS) issued a 60-day waiver of the Jones Act, allowing foreign-flagged vessels to transport oil, natural gas, fertilizer and other resources between U. S. ports. The suspension was requested by the Department of Defense (DoD) to address supply chain disruptions caused by Operation Epic Fury.

For those unfamiliar, the Jones Act is a 106-year-old law—officially the Merchant Marine Act of 1920—that requires all goods shipped between U. S. ports to be carried on vessels that are American-built, American-owned and American-crewed.

On paper, it sounds like a somewhat reasonable protectionist measure.

In practice, however, it’s become one of the most costly and counterproductive regulations in the U. S. economy, particularly when it comes to energy.

White House Press Secretary Karoline Leavitt framed the waiver as part of a broader effort to strengthen U. S. supply chains. But as the Cato Institute pointed out, the need to suspend a law in order to strengthen supply chains is itself an indictment of that law. I tend to agree.

The U.S. Builds Almost No Ships

The Jones Act, named for Senator Wesley Livsey Jones (R-WA), was supposed to guarantee a domestic market for American-made vessels. Instead, it’s created a closed system of artificially expensive ships with no competitive pressure to innovate.

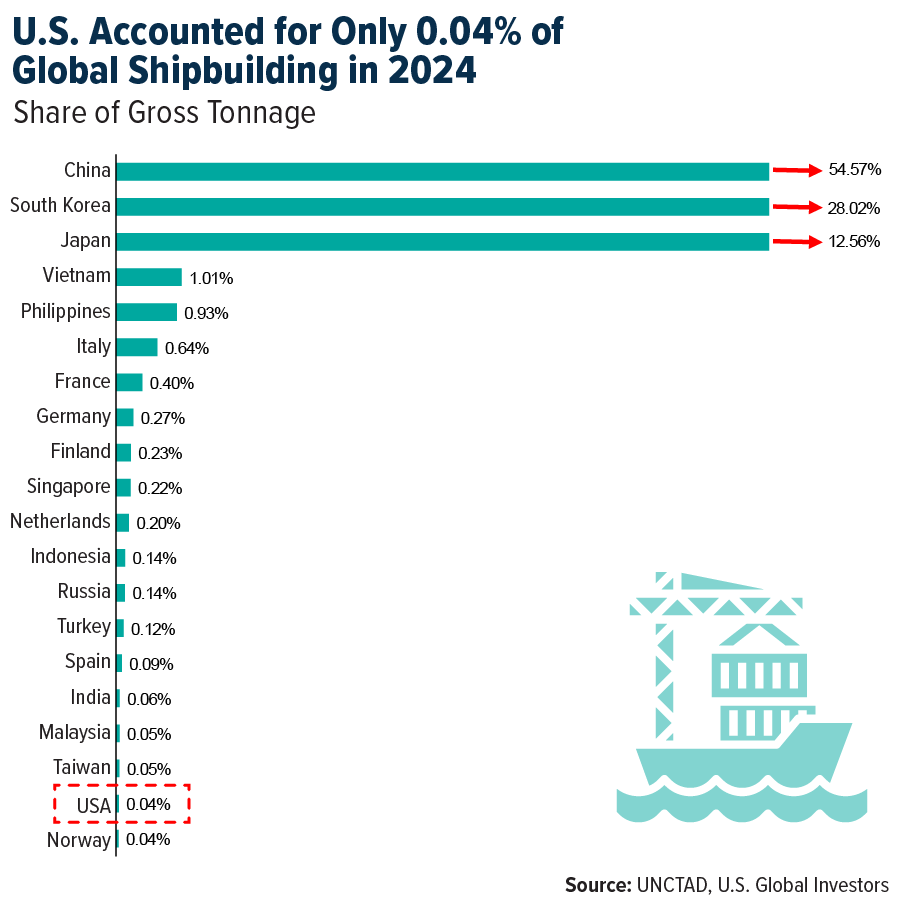

Consider the chart below. It shows each country’s share of global commercial shipbuilding. China dominates at nearly 55%, following by South Korea at 28% and Japan at nearly 13%. Those three countries alone account for more than 95% of the world’s commercial ships.

The U. S. , by comparison, manufacturers only 0. 04%. The world’s largest economy and the nation with one of the longest coastlines on the planet builds essentially zero commercial ships.

After the Reagan administration ended federal subsidies for shipbuilding in 1982, U. S. commercial production collapsed virtually overnight. Output fell from about 20 large vessels a year to just five, and roughly 75,000 shipbuilding jobs were lost.

Today, operating a U. S. -flagged ship is roughly four times more expensive as an internationally flagged one, and building ships domestically costs at least four times more than in other nations like South Korea. The result is a fleet so small and so costly that it can’t even serve America’s own energy needs.

The LNG Paradox

That brings me to what I think is the most striking irony of all.

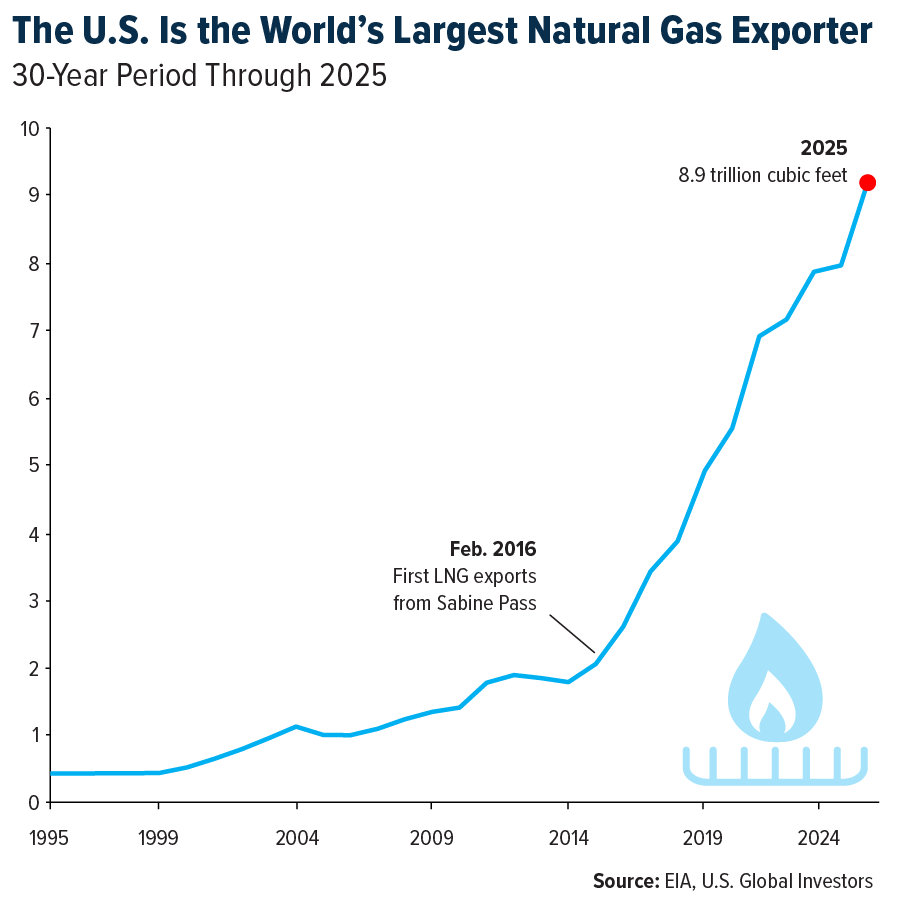

The U. S. is the world’s largest exporter of liquefied natural gas (LNG). Exports have surged from virtually nothing a decade ago to 8. 9 trillion cubic feet in 2025, according to the Energy Information Administration (EIA).

Cheniere Energy, which shipped the first commercial LNG cargo from Savine Pass in February 2016, has since committed more than $50 billion to build and expand its Gulf Coast terminals, with production capacity expected to potentially exceed 100 million metric tons per year by the mid-2030s.

Yet there’s not a single LNG tanker that fully meets Jones Act requirements. Not one.

That means the U. S. can export LNG to Europe, Asia and everywhere else, but it can’t transport LNG from the Gulf Coast to New England or Puerto Rico using the kind of large-scale vessels the trade requires.

The consequences, frankly, are absurd. It’s actually cheaper for New England to import LNG from overseas—including, until recently, from Qatar—than to purchase it from fellow Americans on the Gulf Coast. We’re the world’s largest natural gas producer, and millions of Americans can’t affordably access their own supply. As I see it, that’s a policy failure of the highest order.

Goldman Sachs notes that the 60-day waiver could ease oil and refined product transport from the Gulf Coast to the East Coast and may even reduce fuel prices. But it’s a Band-Aid, not a long-term solution.

Follow the Money

For investors, the set-up could be compelling. The Iran conflict has taken roughly one-fifth of global LNG supply offline. Iran’s retaliatory strikes damaged 17% of Qatar’s LNG export capacity, and repairs could take up to five years. Spot tanker rates are reportedly running at about $180,000 per day, and Goldman Sachs expects the LNG market to stay disrupted through 2027.

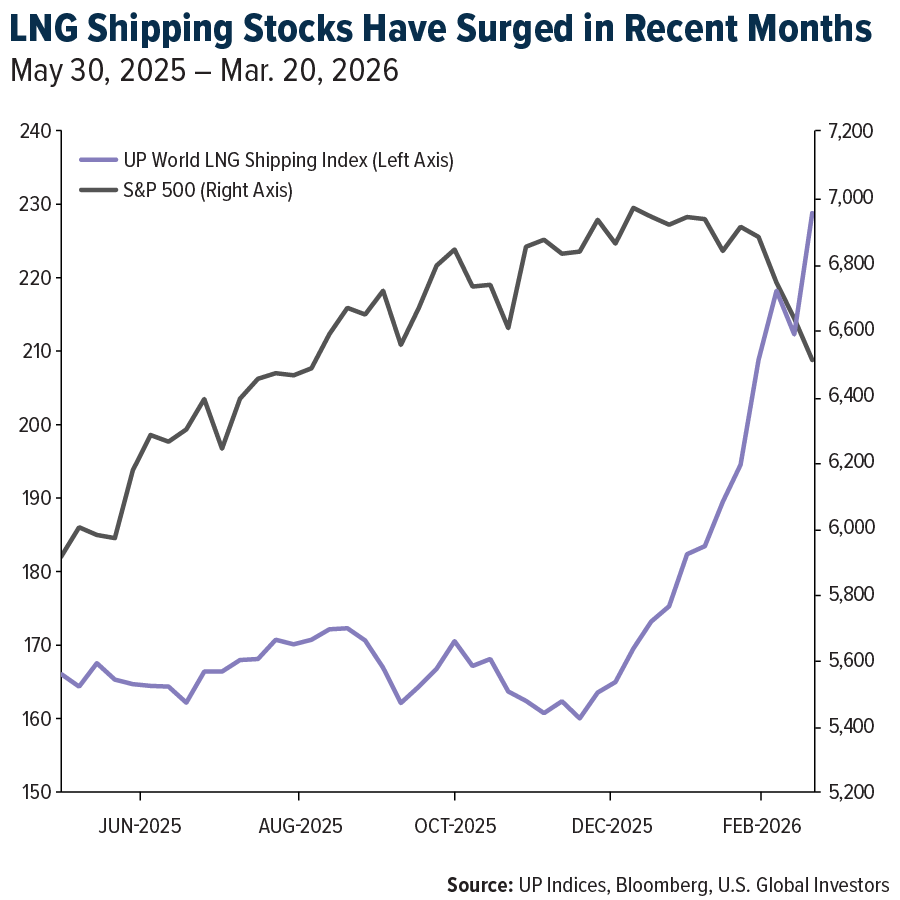

The UP World LNG Shipping Index, which tracks 20 publicly traded LNG shipping companies, surged nearly 8% in the week ended March 20, even as the S&P 500 fell almost 2%.

Goldman has identified three companies it believes are best positioned right now: Venture Global LNG, Cheniere Energy and Golar LNG. Year-to-date, Venture Global is up more than 150%, while Cheniere is up approximately 50%, Golar a little less so. These are companies with real assets, real cash flows and a strong tailwind that could last for years.

I should also point out just how different America’s situation is compared to the last Middle Eastern conflict. During the Iraq War in 2003, the U. S. was an energy importer. Today, it’s the world’s largest producer and exporter of natural gas. As I write this, the Henry Hub natural gas spot price (the U. S. benchmark) is above $3 per million British thermal units (MMBtus). In Europe, it’s over $18 MMBtus. America’s ingenuity and energy dominance have protected consumers and businesses in ways that would have been unimaginable two decades ago.

What This Means for Your Portfolio

The Jones Act waiver is a telling sign that the law has been holding back American energy logistics for over a century. Whether or not this suspension leads to permanent reform is a political question I can’t answer. But the investment implications seem clear to me.

U. S. LNG producers and exporters are the direct beneficiaries of the global supply gap. LNG shipping companies are enjoying record rates with no relief in sight. And the broader energy sector remains well-supported by geopolitical risk premiums and strong domestic fundamentals.

As always, I recommend a 10% weighting in gold—5% in physical bullion and 5% in high-quality gold mining names—as a hedge against the fiscal and inflationary pressures that wars inevitably produce.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Sabre, up 15. 2%. According to Bank of America, the Airline Reporting Corporation’s average ticket price rose higher by 6. 9% in February, above January’s higher by 4. 3%, while Airline Fare CPI was up 7. 1% and Air Passenger Services PPI was up 3. 1%.

- According to CIBC, the most significant airfreight increase was out of India, where rates increased by 30% this week to Europe. The U. S. and European markets also registered upward pressure across most outbound lanes.

- Airline credit card spend, according to Bank of America aggregated debit and credit card data, has increased higher by 12% in March (February grew higher by 4. 5%), and March spend is now higher by 4% compared with 2024 levels. Industry pricing power is also evident in airline spend per transaction, which is up more than 8% versus 2024.

Weaknesses

- The worst-performing airline stock for the week was Make My Trip, down 8. 8%. This increase in airline cancellations is occurring while a record number of TSA officers at airports have called out since the partial Department of Homeland Security shutdown began. According to ABC News, over 3,250 officers called out on Saturday, March 21, accounting for 11. 5% of the scheduled workforce.

- Bunker availability has become an issue at some Asia ports, but limited disruptions to operations are observed given relatively short voyages and sufficient supply of bunkers at China ports. One company Morgan Stanley spoke to also mentioned potential port strikes in Asia due to elevated fuel prices.

- According to UBS, Thailand has halted all fuel exports, while Chinese authorities have urged domestic refiners to curb overseas shipments of gasoline, diesel, and jet fuel. Sinopec, China’s biggest oil refiner, has reduced its run rates by 10% in response to the supply squeeze resulting from traffic disruption in the Strait of Hormuz. South Korea, a major jet fuel supplier—particularly to the U. S. West Coast—has capped refined product exports at 2025 levels to safeguard its domestic market.

Opportunities

- The Indian government has removed caps on IndiGo airfares, which were imposed in December 2025, according to Morgan Stanley. Fares in India are expected to rise sharply on April 1 as underlying jet fuel more than doubled in March. Last week, IndiGo and its peers introduced a fuel surcharge covering around 20% of the fuel increase. With airfare caps removed, further fare hikes are expected.

- Goldman Sachs believes the market is overlooking the VLCC market’s underlying and structural evolution, with much higher concentration giving tanker operators stronger pricing power. They are particularly bullish on the ongoing super-cycle for VLCCs, considering tight capacity, oil restocking and trade re-routing, and stronger pricing power from significantly higher VLCC market concentration.

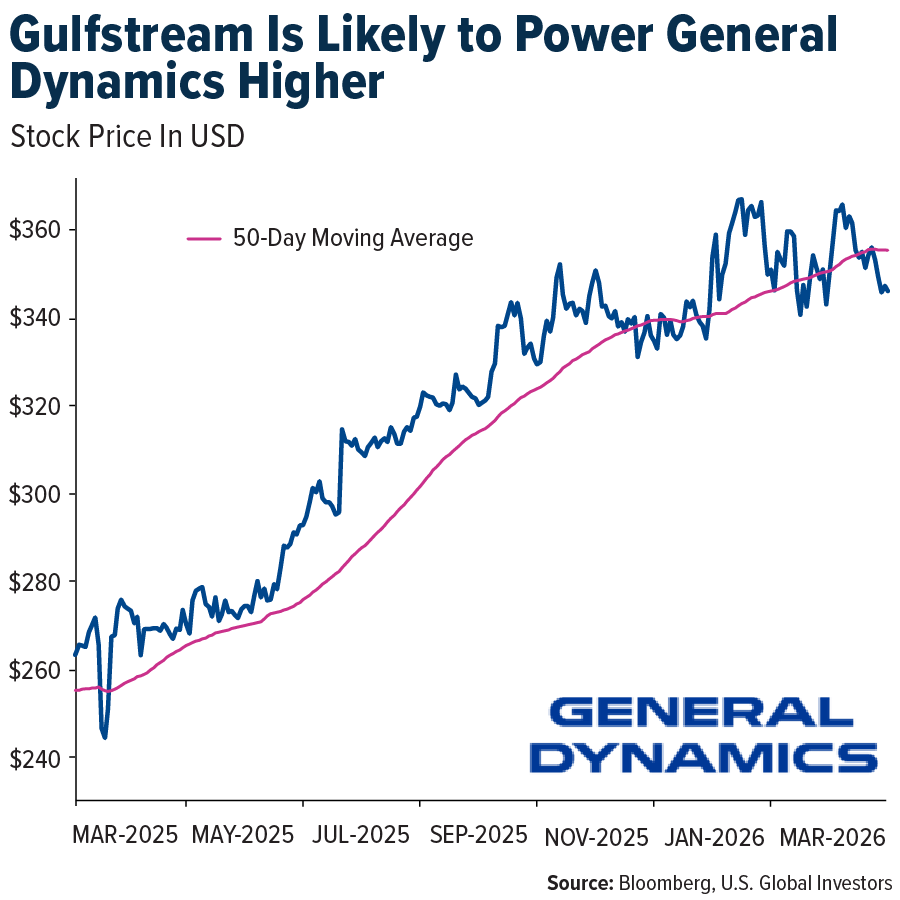

- Textron and Gulfstream are far ahead of typical seasonality, pointing to first-quarter upside versus consensus, while Bombardier and Embraer are in line and Dassault is off to a slow start, according to UBS. Gulfstream is known to have the highest quality product with the best service, and this is preferred by executives.

Threats

- Since the start of the Iranian conflict, refiners have rallied 15%, bringing year-to-date gains to 40 percent. This has been supported by a doubling of U. S. refining margins, reaching levels last seen in 2022–2023, according to Morgan Stanley.

- The Persian Gulf war is now in its fourth week, disrupting operations in the Strait of Hormuz and at Middle East airports, impacting 2–3 percent of global sea freight volumes and 15 percent of air freight capacity, according to JP Morgan.

- Media reports indicate that Cathay Pacific will introduce another round of fuel surcharge hikes on April 1, raising the fuel surcharge by 34 percent from the current level. On a cumulative basis, the fuel surcharge hikes are estimated to lift the weighted average ticket price by 11 percent compared with pre-conflict levels, according to UBS.

Luxury Goods and International Markets

Strengths

- Burberry shares saw support this week following insider buying by a company director, signaling confidence in the brand’s outlook despite recent sector weakness. Insider purchases are often viewed positively, suggesting management believes the stock is undervalued at current levels.

- Eurozone inflation expectations came in softer than expected in February, providing a supportive signal for the luxury sector. According to the ECB Consumer Expectations Survey, 1-year CPI expectations declined to 2. 5% from 2. 6%, while 3-year expectations fell to 2. 5% from 2. 6%, both below Bloomberg analysts’ forecasts.

- Shilla, a South Korean luxury hospitality and duty-free operator, led the S&P Global Luxury Index over the past five days, rising about 8% as improving travel sentiment and a potential recovery in Asian tourism supported the stock.

Weaknesses

- Carnival shares declined after the company lowered its full-year outlook, with earnings, EBITDA, and net income guidance all coming in below expectations. The revision reflects rising fuel costs driven by higher oil prices amid Middle East tensions.

- Year to date, the S&P 500 Index continues to correct and is now down about 7%. The worst-performing sector is Financials, down 12. 4%, followed by Consumer Discretionary at -12. 2% and Information Technology at -11. 6%. Energy is the best-performing sector, gaining about 40% year to date, supported by higher oil prices.

- Estée Lauder, a global beauty and fragrance company focused on premium cosmetics and skincare, was the worst-performing name in the S&P Global Luxury Index over the past five days. Shares declined about 20% on reports of a potential deal involving Puig.

Opportunities

- Luxury stocks, as measured by the S&P Global Luxury Index, have declined roughly 20% since the escalation of the Middle East conflict at the end of February. As a result, valuations appear oversold, and any signs of de-escalation or stabilization could act as a catalyst for a sector rebound.

- Tesla (TSLA) saw improved sentiment this week as European sales returned to growth, signaling potential stabilization after a prolonged decline. The company reported its first year-over-year increase in the region in over a year, supported by a broader recovery in the European auto market and rising demand for electric vehicles.

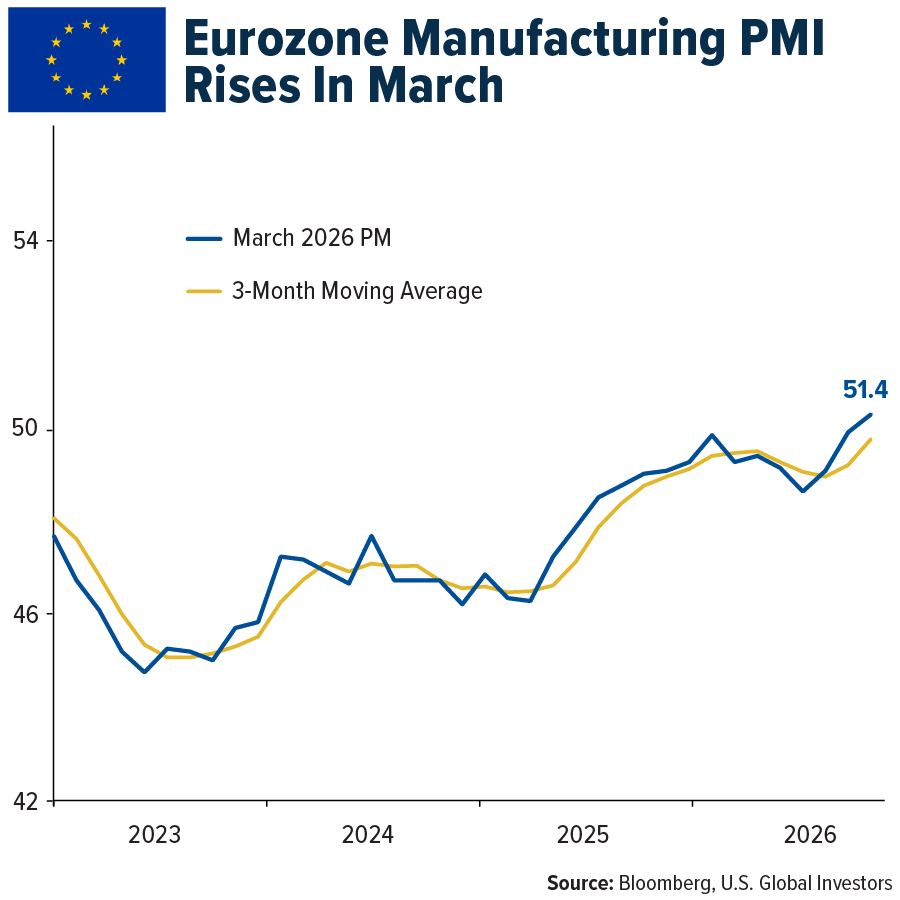

- EU manufacturing data for March came in stronger than expected, with the PMI rising to 51. 4 versus 49. 6 expected, signaling improving factory activity. A PMI reading above 50 indicates expansion, while below 50 signals contraction. Additional upside could be indicated if the 1-month moving average crosses above the three-month moving average.

Threats

- Luxury stocks are currently in oversold territory and appear due for a potential bounce. However, the key question is how long they can remain oversold before a recovery begins. The direction of equities will largely depend on developments in the Middle East, where uncertainty remains high and future outcomes are difficult to predict.

- Markets have been highly volatile recently, with sharp swings driven by uncertainty around geopolitical developments. The ongoing conflict in the Middle East continues to weigh on investor sentiment, particularly through its impact on energy prices, global trade routes, and overall economic stability. As long as tensions persist and the outlook remains unclear, markets are likely to experience continued volatility in the near term.

- Ahead of Hermès’ Q1 2026 trading update on April 15, JPMorgan Chase lowered its sales forecast, citing Middle East conflict, softer tourist spending in Europe, and continued volatility in China. The firm now expects sales growth of 8% this year, down from 10% previously. Middle East sales, about 4% of group revenue, are now projected to decline 3%, compared with prior expectations of 17% growth.

Energy and Natural Resources

Strengths

- The best-performing commodity for the week was lithium carbonate, up 4. 63%. Prices rose as grid-scale battery storage demand, especially for LFP batteries, remained firm despite weak electric vehicle demand. The move was amplified by supply constraints, including tight spodumene availability and continued production discipline, rather than a surge in buying. Higher petroleum costs also make renewable energy more attractive.

- The Dallas Fed Energy Survey showed a sharp rebound in oil and gas activity in Q1 2026, with the business activity index rising from -6. 2 to 21. 0 and company outlooks improving, though uncertainty remained elevated at 53. 7. Oilfield services firms saw equipment utilization jump from -12. 2 to 30. 2, while prices turned positive. Executives expect WTI at $74 per barrel year-end and Henry Hub natural gas at $3. 60 per MMBtu, rising to $4. 42 over five years.

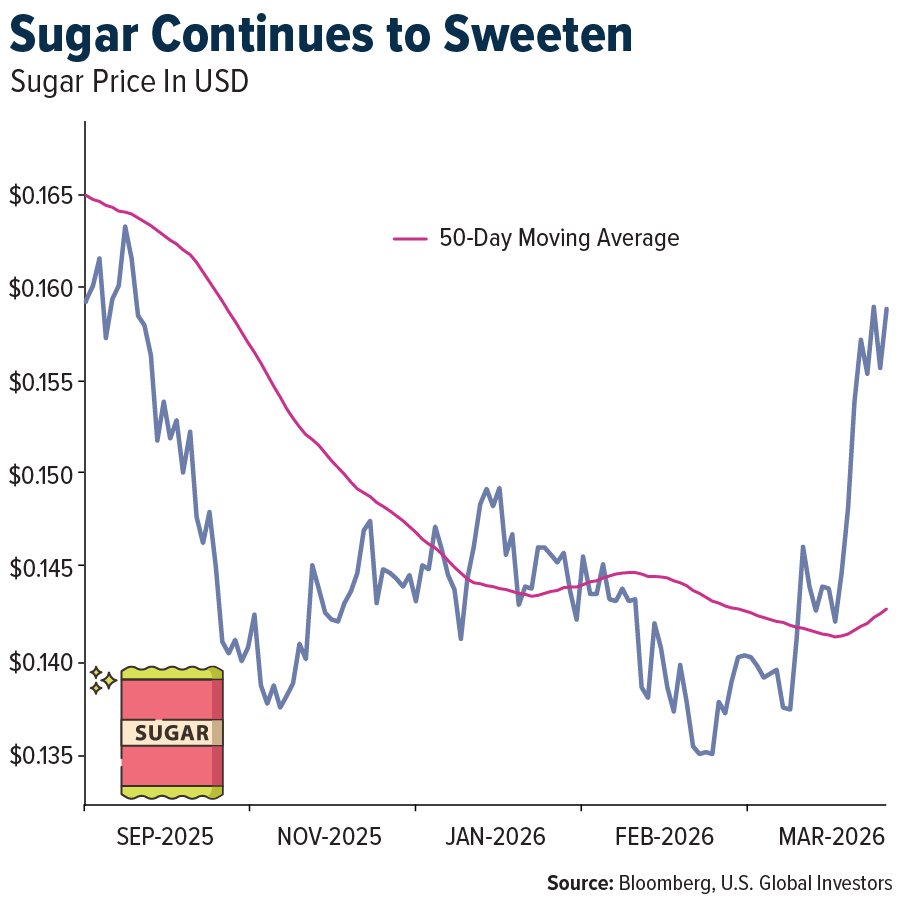

- Sugar futures have rallied to 5. 5-month highs, driven by reduced supply from droughts in major exporters like India and Thailand. Rising energy costs are increasing refining expenses and encouraging sugar cane diversion to ethanol production. Technical indicators remain bullish, with a breakout above 16. 05 cents potentially targeting 18. 50 cents, supported by tight supply and elevated oil prices. At these levels, consumers may shift to alternatives or reduce consumption.

Weaknesses

- Arabica coffee futures dropped as much as 2. 7% as expectations of a record harvest in Brazil continue to weigh on prices, despite near-term supply tightness caused by low shipments and East African shipping delays linked to the Middle East conflict. While prompt delivery premiums have widened due to tight availability, returning rainfall to Brazilian growing regions is reinforcing optimistic crop forecasts and keeping broader price pressure intact.

- At least 600 Australian service stations have run out of fuel as the near closure of the Strait of Hormuz following U. S. -Israel strikes on Iran cut off roughly a fifth of global oil supplies. Import-dependent Australia has about 38 days of gasoline and 30 days of diesel in reserves. The government is lowering diesel standards to broaden supply options, has doubled antitrust penalties to A$100 million amid price gouging concerns, and attributes the shortage to panic buying rather than an immediate supply crisis, though South Korea, its largest supplier, has announced export caps.

- A refinery explosion at Valero’s Port Arthur facility on Monday night forced nearby residents to shelter in place, though no injuries were reported. The incident may cause temporary supply disruptions, potentially supporting near-term crude and refined product prices as the extent of the damage is assessed.

Opportunities

- JPMorgan warns that aging U. S. grid infrastructure poses a “national security risk” amid rising threats from extreme weather, cyberattacks, and geopolitical energy disruptions tied to the Iran conflict. The bank sees grid modernization as a major investment opportunity, with $5. 8 trillion in global grid spending expected through 2035 as countries prioritize energy resilience and self-sufficiency.

- U. S. energy leaders at the CERAWeek conference warned that despite LNG facilities operating at 135% capacity, the country lacks the infrastructure to offset the global shortage caused by Iran’s blockade of the Strait of Hormuz, which has disrupted nearly 20% of global oil and LNG supplies. The crisis has increased pressure on U. S. producers to expand capacity, but permitting delays and litigation continue to stall new projects, leaving Europe and Asia seeking alternative supplies ahead of next winter.

- The global nuclear buildout across Asia and the U. S. is driving strong demand for a limited group of reactor builders, including GE Vernova, Westinghouse, and Korea’s KHNP. Uranium suppliers such as Cameco and Centrus Energy are also positioned to benefit from a structural supply deficit, as enrichment capacity remains concentrated in Russia. Transmission and grid infrastructure companies should see additional tailwinds, as new nuclear capacity requires significant upgrades to connect baseload power to data centers and industrial users, with the U. S. projecting 166 GW of new peak load by the end of the decade.

Threats

- Oil theft in the Permian Basin has escalated to an estimated $1–2 billion annually, with thieves using vacuum trucks to siphon crude from storage tanks in broad daylight, posing as waste haulers and laundering stolen barrels through disposal facilities or smuggling them to Mexico. Despite new Texas legislation, an FBI task force, and a Railroad Commission study, local law enforcement solves only about 2% of cases. While federal involvement has increased visibility, officials say it has not added resources to the understaffed counties where 40% of oil executives report being affected.

- Russia has temporarily banned ammonium nitrate exports from March 21 to April 21, 2026, to secure domestic supply for spring planting, suspending all export licenses except those under intergovernmental agreements. As a key exporter to Brazil, the U. S. , and Europe, the restriction could tighten global nitrogen fertilizer supply and support agricultural commodity prices during a critical planting season.

- America’s nuclear expansion faces key bottlenecks, including fewer than 5,000 certified nuclear welders, a projected shortfall of 320,000 welders by 2029, and reliance on Russia for 40–45% of global uranium enrichment while domestic HALEU production remains limited. First-of-a-kind SMR costs range from $89 to $180 per MWh versus $40 to $65 for natural gas, and a history of budget overruns suggests continued cost risks, even as major technology companies like Meta, Microsoft, and Amazon drive demand through large power purchase agreements.

Bitcoin and Digital Assets

Strengths

- Coinbase has partnered with Better Home & Finance, a Fannie Mae-approved digital mortgage lender, to let homebuyers use bitcoin or USDC as collateral for down payments. This expands crypto’s practical use by helping borrowers access housing without selling digital assets or triggering taxes. As a conforming loan backed by Fannie Mae standards, the partnership adds credibility to crypto and signals growing institutional acceptance in traditional finance.

- Despite trading in a tight range for nearly 50 days, bitcoin’s price action reflects structural consolidation rather than a bearish continuation pattern. Unlike prior cycles, the market has built stronger support, with significant demand reported between $50,000 and $70,000. Short-term momentum remains muted, but bitcoin shows resilience and a more stable foundation than in previous drawdowns.

- Trust Wallet, the self-custody digital wallet acquired by Binance founder Changpeng Zhao, launched AI-powered agents that execute crypto transactions across 25+ blockchains for its 220+ million users. The toolkit automates recurring buys, cross-chain swaps, and portfolio actions while keeping users in control of assets and permissions. The launch demonstrates how digital asset platforms are evolving beyond storage into intelligent, scalable, and user-friendly financial tools.

Weaknesses

- Proposed restrictions on stablecoin rewards in the latest U. S. market structure draft highlight a key weakness in digital assets: user adoption can still be driven by incentives rather than transactional utility. Citigroup noted the development is not a fundamental threat to Circle’s USDC but could slow growth by making certain platforms less attractive. The episode shows parts of the stablecoin market remain vulnerable to policy changes and evolving monetization models.

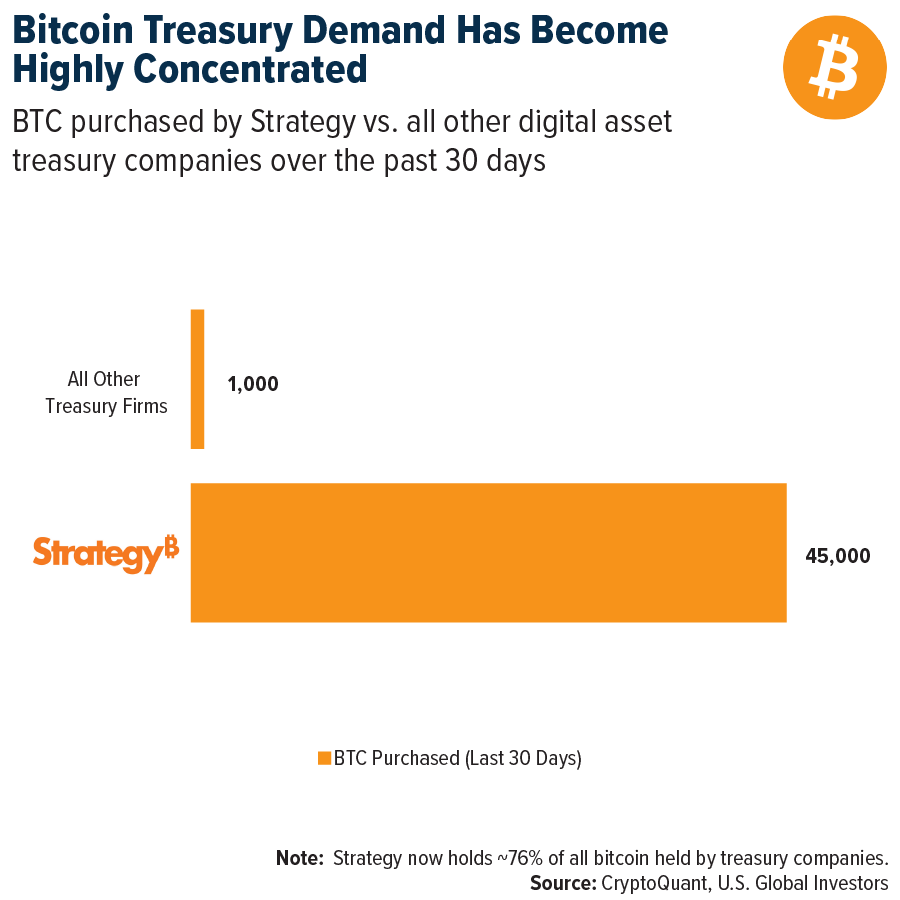

- Over the past 30 days, Strategy purchased about 45,000 BTC, while all other digital asset treasury companies combined bought around 1,000 BTC, according to CryptoQuant. Strategy now holds roughly 76% of all bitcoin owned by treasury companies, underscoring how reliant the narrative is on a single buyer. This concentration weakens the case for broad corporate adoption and raises concerns about the durability of treasury-driven demand in challenging market conditions.

- Bhutan’s government transferred another 519. 7 BTC, worth about $36. 8 million, bringing its total crypto outflows in 2026 to more than $152 million, according to Arkham data. Its bitcoin holdings have fallen from a peak of roughly 13,000 BTC in late 2024 to about 4,453 BTC today, a decline of nearly 66%. The increasing pace of these sovereign sales adds persistent supply to the market and raises concerns about whether state-backed bitcoin accumulation stories are as durable as previously believed.

Opportunities

- Elon Musk’s X is advancing its push into payments with the upcoming launch of X Money across 40+ U. S. states, while hiring a senior crypto-native design leader with experience at Coinbase’s Base and Aave. The platform plans to offer peer-to-peer payments, bank deposits, debit cards, and up to 6% yield on balances, signaling ambitions to become a full financial super app. While crypto integration has not yet been confirmed, the addition of experienced DeFi talent highlights growing optionality for future blockchain-based features.

- BitGo, a leading institutional digital asset custodian, and ZKsync, an Ethereum-based scaling network developed by Matter Labs, are building infrastructure that allows banks to issue, transfer, and settle tokenized deposits on blockchain rails while staying within regulatory frameworks. The platform combines BitGo’s custody and wallet services with ZKsync’s permissioned, privacy-preserving network and is already being tested by regulated financial institutions ahead of a broader rollout later this year. This underscores growing momentum for bringing traditional banking activity on-chain in a compliant, scalable way.

- Tether’s omnichain stablecoin, USDT0, is expanding to Tempo, a payments-focused Layer 1 blockchain co-developed by Stripe and Paradigm. Powered by LayerZero Labs, USDT0 surpassed $70 billion in cumulative transaction volume within its first 12 months, and this integration will mark its 23rd blockchain deployment. The expansion highlights growing momentum for stablecoins as scalable payment and settlement rails across an increasingly interoperable digital asset ecosystem.

Threats

- Political uncertainty ahead of the U. S. midterm elections poses a risk to the digital asset industry, as a shift in congressional control could weaken support for crypto legislation. Advocacy groups like Stand With Crypto are mobilizing, but priorities such as market reform, crypto tax rules, and a potential U. S. strategic bitcoin reserve could lose momentum, creating a more uncertain regulatory backdrop heading into 2027.

- Brazil’s government enacted a law allowing authorities to seize, freeze, and repurpose cryptocurrencies linked to criminal activity, highlighting growing state oversight. Confiscated crypto can fund public security initiatives, and judicial powers over wallets and exchanges are expanded. While aimed at organized crime, the measures raise concerns about broader state control and legal risks for crypto holders.

- TRM Labs, a blockchain intelligence firm used by law enforcement and financial institutions, launched an AI-powered investigative assistant as illicit crypto activity grows. Illicit crypto volume reached $158 billion last year, while AI-enabled fraud and scams surged 500%, driven by automation, deepfakes, and more sophisticated criminal tools. The trend shows a rising threat to the ecosystem, intensifying regulatory scrutiny and potentially weakening user and institutional trust.

Defense and Cybersecurity

Strengths

- Lockheed Martin secured a $478 million contract for the Integrated Submarine Imaging System, with potential expansion to $1. 19 billion through options, providing engineering and technical support from Manassas, Virginia, through an expected completion in 2036.

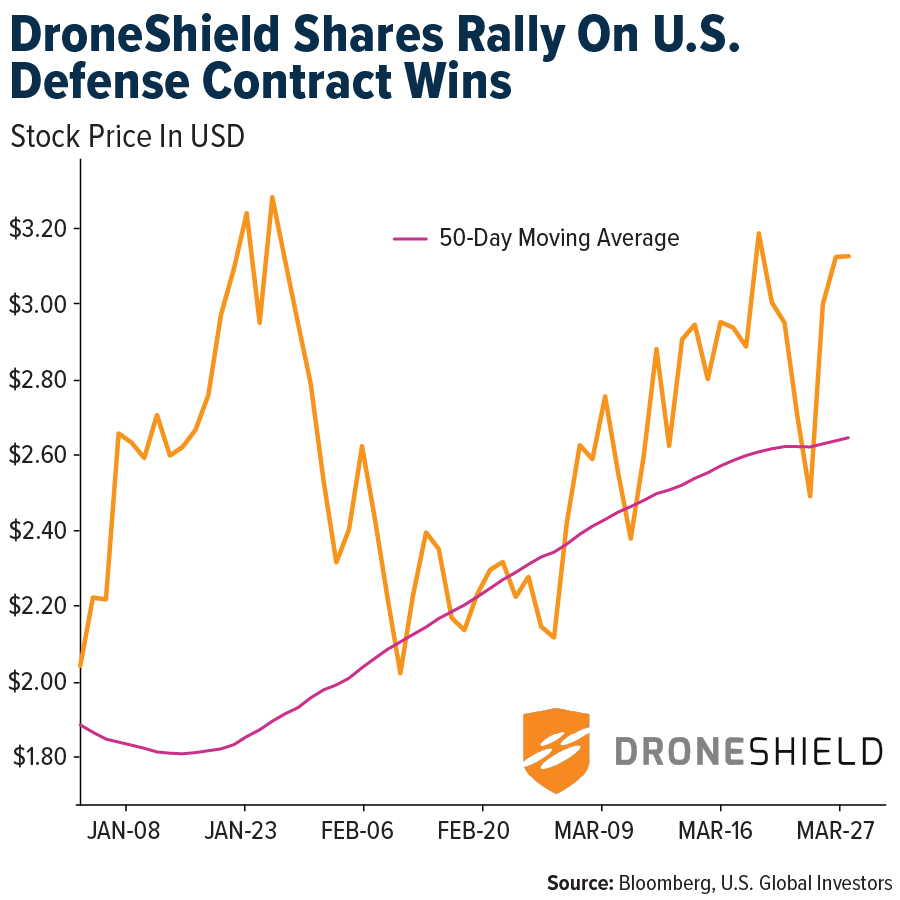

- DroneShield shares have rallied year-to-date as new military orders, including a U. S. Department of Defense contract, boosted revenue visibility and positioned the company in the global counter-UAS spotlight. The move was reinforced by JPMorgan disclosing a 5. 3% stake in late March, signaling growing institutional confidence in DroneShield’s scale-up potential.

- Leonardo DRS secured a major contract worth over $25 billion under the Advanced Technology Support Program V to support the U. S. military. In addition, the U. S. State Department approved a $1 billion AUKUS submarine support package for the UK, involving key contractors like Lockheed Martin and Huntington Ingalls.

Weaknesses

- Senator Rick Scott has filed a lawsuit against Booz Allen Hamilton over a tax return leak involving high-profile individuals, highlighting a serious failure to protect sensitive information.

- CoreCivic faces scrutiny over mishandled sexual assault investigations at the Otay Mesa detention center, raising concerns about detainee safety and oversight.

- Iran rejects any ceasefire, calling U. S. negotiations “illogical” and dismissing reports of a deal as “total nonsense. ” Tehran denies any current agreement, mockingly claiming that former President Trump is “talking to himself,” while asserting that the U. S. continues efforts to secure a ceasefire.

Opportunities

- Arm launched its first in-house AGI-focused CPU for AI data centers, co-developed with Meta and manufactured by TSMC, marking a strategic shift from its pure licensing model and directly challenging x86 incumbents like Intel and AMD. Arm claims roughly 2× performance per rack versus competitors. Early partners including Cloudflare, Meta, and OpenAI highlight real-world adoption and the architecture’s relevance for next-generation AI infrastructure.

- Nvidia’s partnership with Samsung on next-generation ferroelectric NAND is highlighted, and Alphabet’s TurboQuant algorithm is introduced as a method to reduce memory requirements for large language models, potentially easing hardware bottlenecks.

- Micron announced a $25 billion capital expenditure plan for 2026 to expand AI infrastructure capacity, raising investor concerns about future investment needs despite strong financial performance.

Threats

- U. S. juries found Google and Meta liable for addictive platform designs that harmed a young user’s mental health, raising the prospect of product redesigns, higher compliance costs, and tighter youth-safety rules for algorithmic systems.

- Google unveiled the TurboQuant algorithm, claiming to reduce AI inference memory requirements by up to six times, directly challenging the assumed trajectory of AI-driven memory demand. If widely adopted, this efficiency could pressure volumes, pricing, and valuations across memory suppliers such as Micron, SanDisk, and peers.

- Recent reporting shows the U. S. deploying thousands of Marines and airborne troops to the Middle East while refusing to rule out limited ground operations against Iran. This posture increases the risk of rapid escalation, as even a limited operation could carry disproportionate casualty, political, and market consequences.

Gold Market

This week gold futures closed the week at $4,538. 30, down $71. 30 per ounce, or 1. 55%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5. 82%. The S&P/TSX Venture Index came in up 0. 38%. The U. S. Trade-Weighted Dollar rose 0. 48%.

Strengths

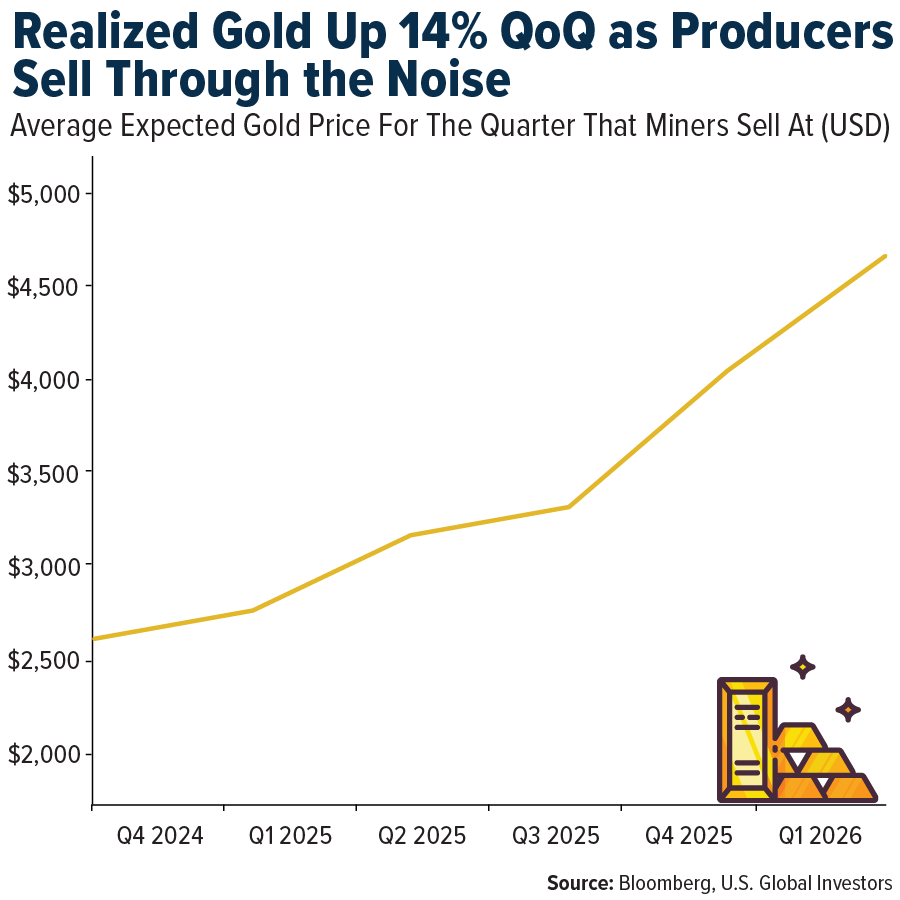

- The best-performing precious metal for the week was silver, up 0. 63%. First quarter’s record-setting environment pushed average realized gold prices up 14% quarter over quarter, which should support strong revenue growth for miners in the first quarter of 2025. Even as spot gold pulls back from its highs, the quarterly average that drives gold company revenue remains at historically elevated levels, reflecting a market that spent most of the quarter at prices the industry has not seen before.

- Zijin Gold International reported FY25 net profit of $1. 6 billion, up 233% year over year, at the upper end of its profit guidance. The strong performance was driven by higher gold prices, solid volume growth, and effective cost control. In FY25, gold prices rose 44%, lifting the company’s average selling price by 53% to $3,524 per ounce, according to Bank of America.

- Uzbekistan’s gold holdings rose to 13. 1 million troy ounces as of March 1, up from 12. 8 million a month earlier, according to the central bank. The value of reserves reached $67. 7 billion, compared to $55. 1 billion at the beginning of the year.

Weaknesses

- The worst-performing precious metal for the week was platinum, down 5. 95%. Platinum ETF holdings declined for a fifth consecutive session, shedding 1,521 troy ounces in the latest trading day, bringing the year-to-date decline to 7. 3%.

- Turkey’s central bank reportedly sold or swapped about 60 tons of gold in the first two weeks of the U. S. attack on Iran. Some of the gold was sold outright, but most was used to secure foreign exchange or lira through swap agreements, according to Bloomberg. Turkish policy aims to maintain a stable or depreciating lira.

- Zhaojin guided 2026 gold production down to 16. 5 tons, compared with 17. 5 tons in 2025, and expects high-single-digit cost inflation, mainly due to a mine accident at Canzhuang. Management noted that Canzhuang accounts for about 1 ton of annual production, while the accident led to a broader suspension of nearby operations, according to UBS.

Opportunities

- DoubleLine Capital CEO Jeffrey Gundlach is calling the recent correction in precious metals a strategic entry point, urging investors to view the current “revaluation phase” as a chance to increase exposure. Despite a slide from recent highs near $5,500 down to the $4,400 level, Gundlach remains confident in his long-term thesis.

- Gold’s latest pullback may appear like just another leg lower, but the technical setup is showing signs of potential strength. Momentum has weakened to its lowest level in over a year, with the relative strength index slipping into oversold territory for the first time since 2023, according to Benzinga Newswire. Although gold futures were down this week, spot gold looks set to finish the week with a 0. 5% gain, marking the first weekly increase in the past three weeks.

- Singapore is positioning itself as a major Asian gold-trading hub by expanding vaulting services for foreign central banks and developing a clearing system for local OTC settlement. The working group includes JPMorgan, UBS, DBS, and ICBC Standard Bank. The initiative could attract nations seeking alternatives to London and New York, as central banks globally hold nearly 39,000 tons of bullion and increasingly look to diversify storage locations amid geopolitical uncertainty.

Threats

- Several Chinese banks, including Industrial & Commercial Bank of China, China Construction Bank, China Merchants Bank, and Bank of Jiangsu, plan to tighten rules for investing in gold accumulation products. These products allow regular or flexible small cash investments in gold. Retail participation has grown substantially in recent years, with many households using them as savings vehicles. Flows are reportedly not captured in ETF data. Given recent price volatility, banks are advising clients to “act rationally,” with some considering capping purchases or raising transaction fees.

- Russia has begun selling physical gold from its central bank reserves for the first time in 25 years, as the government seeks to offset a widening budget deficit driven by sustained military spending. The Central Bank of Turkey reported a $7. 6 billion reduction in gold holdings over the past week, with $4. 5 billion through swaps and the remainder likely sold outright, according to Bank of America. Russia could continue gold sales as Ukraine struck Russia’s Baltic oil ports twice this past week.

- With 88% of platinum group metal demand tied to consumer discretionary sectors, including autos and jewelry, demand tends to decline in recessionary environments. Reviewing the last three global slowdowns over the past 25 years, PGM demand fell 14–21%. In two of those cycles, the weighted average price basket declined significantly, by 32% in 2002 and 35% in 2009, according to UBS.