Markets continued their back-and-forth pattern amidst the back-and-forth attempts to resolve the conflict in the Persian Gulf. This morning, US traders awoke to sharply lower index futures amidst a backdrop of higher crude oil prices and bond yields. The deal enthusiasm that pervaded yesterday’s and Monday’s activity ebbed sharply overnight. Yet as I type this, less than an hour after the open, the S&P 500 (SPX) has clawed back more than half its early losses despite a lack of substantive news. Hope springs eternal.

Around 8AM EDT, when futures were about 0. 9% lower, I was asked why. Remember, I get asked questions of that sort much more frequently when markets are lower; no one reached out yesterday morning to ask why futures were higher. (It’s a good thing, too. I was standing in a TSA line at LaGuardia Airport at the time, though it turned out to only require about 20 minutes. ) Stocks are supposed to go up, so a reason is either obvious – like yesterday – or one isn’t really required.

My answer to the early inquiry was that traders’ enthusiasm for the likelihood of a quick deal to end the conflict in the Persian Gulf had faded as it appears that the Iranians have little current interest in talks. That puts us back in a situation where oil prices rise, thus dragging yields higher and stocks lower. Since then, we have seen oil futures come off their highs, with bonds and stocks improving accordingly.

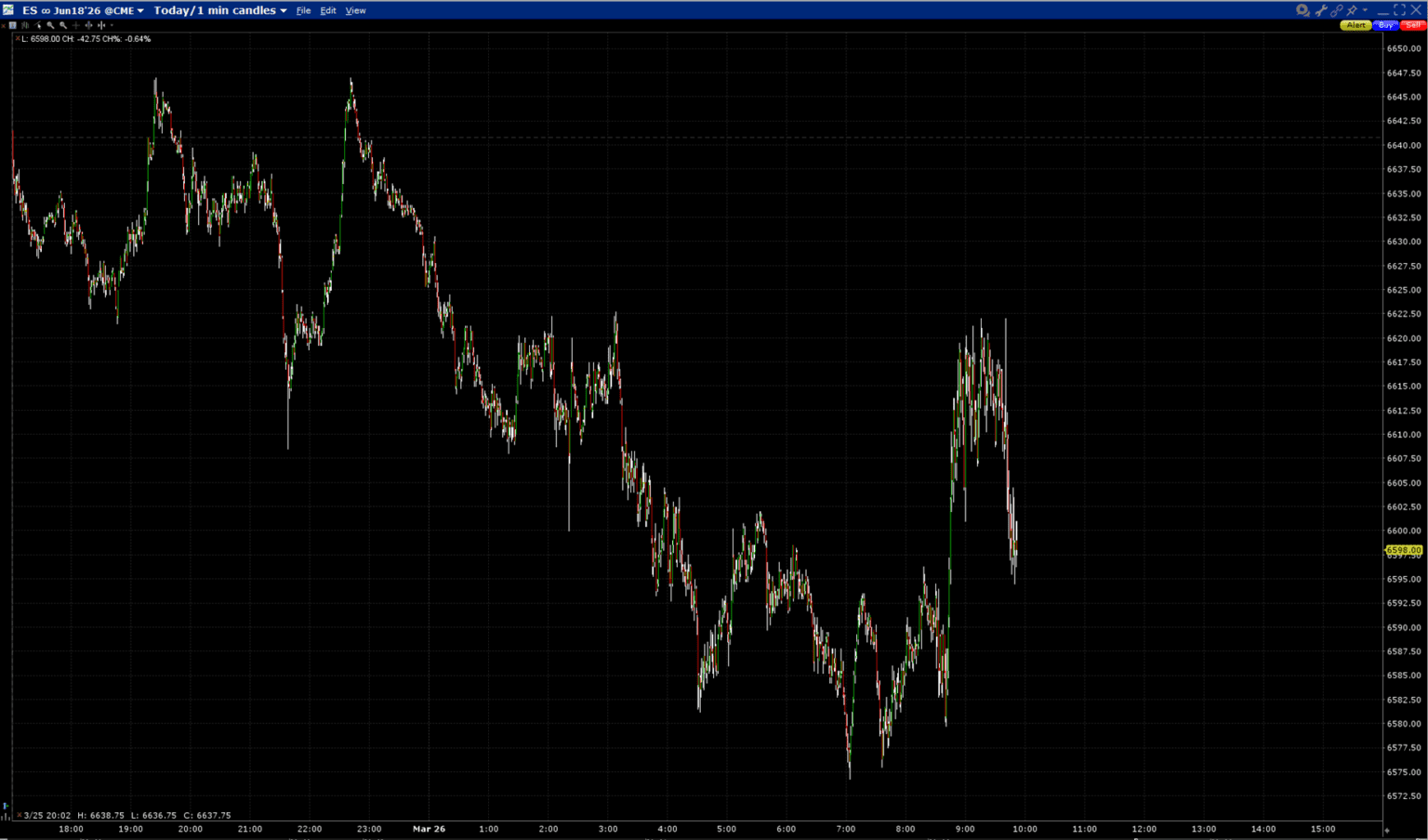

Around 10 AM EDT, well after stocks had already commenced their bounce off their lows, we got a response from Iran. They called the US negotiations claim “deception” and said that Hormuz sovereignty will remain its right. That sounds like a “no”, or at least a “not now”, yet stocks dipped only modestly and for only a short time. (They’re dipping again in the 20 minutes since I started typing, showing once again the difficulty in pinning down intraday moves. )

ES June Futures, Intraday 1-Minute Candles

Source: Interactive Brokers

My read on the situation is this: US traders are relentlessly more optimistic than those in the rest of the world, so as soon as there is a meaningful dip and a nascent bounce, buyers return to the market. They seem relatively unperturbed by the lack of a positive response from Iran because they remember the face-ripping rally that occurred in April after the President reversed course on the most egregious of the tariff announcements. Whether you considered that to be “TACO”, a “Trump Put”, or simply comfort in the belief that a President who has acknowledged using stock market metrics as a barometer for his economic performance would take remediating action, the lesson was clear. Skeptics got punished and dip buyers got richly rewarded.

Few investors, no matter how concerned they may be about the prospects of higher oil prices bleeding into broader price pressures and economic malaise, want to risk being caught wrong-footed in the event of a ceasefire or similar resolution.

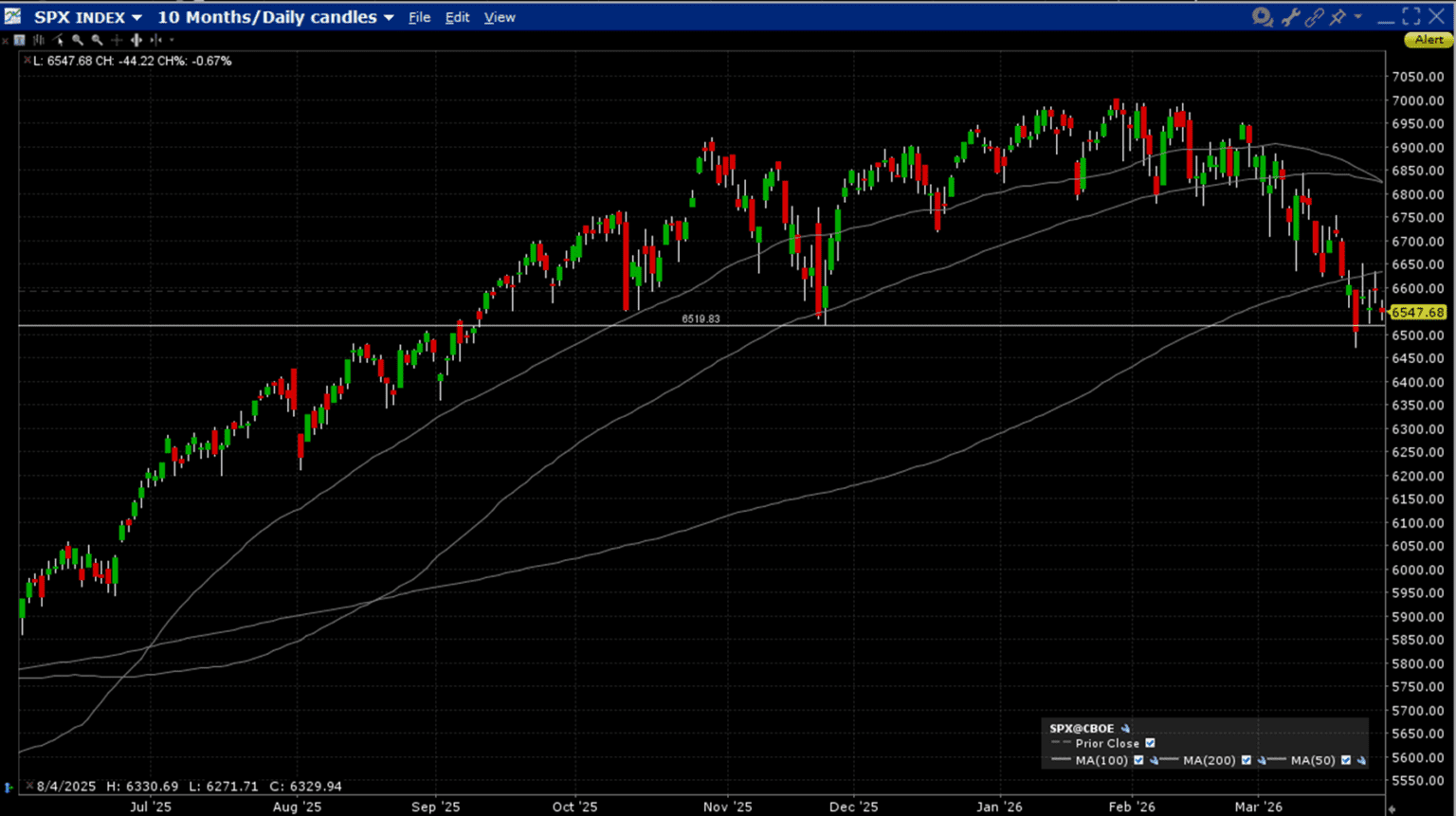

We see this reflected in SPX options pricing vis-à-vis the trends in the underlying index. A quick glance at an SPX chart should make the deterioration apparent. Since late February we have seen a pattern of lower highs, lower lows, and key moving averages pointing lower. The lone exception is the 200-day moving average, which once again offered resistance to yesterday’s bounce after providing only fleeting support last week.

Source: Interactive Brokers

A pattern like the one we are seeing would normally have obvious strategic implications: favor shorts over longs, selling rallies and using dips to cover shorts rather than to establish longs. But few seem eager to do that.

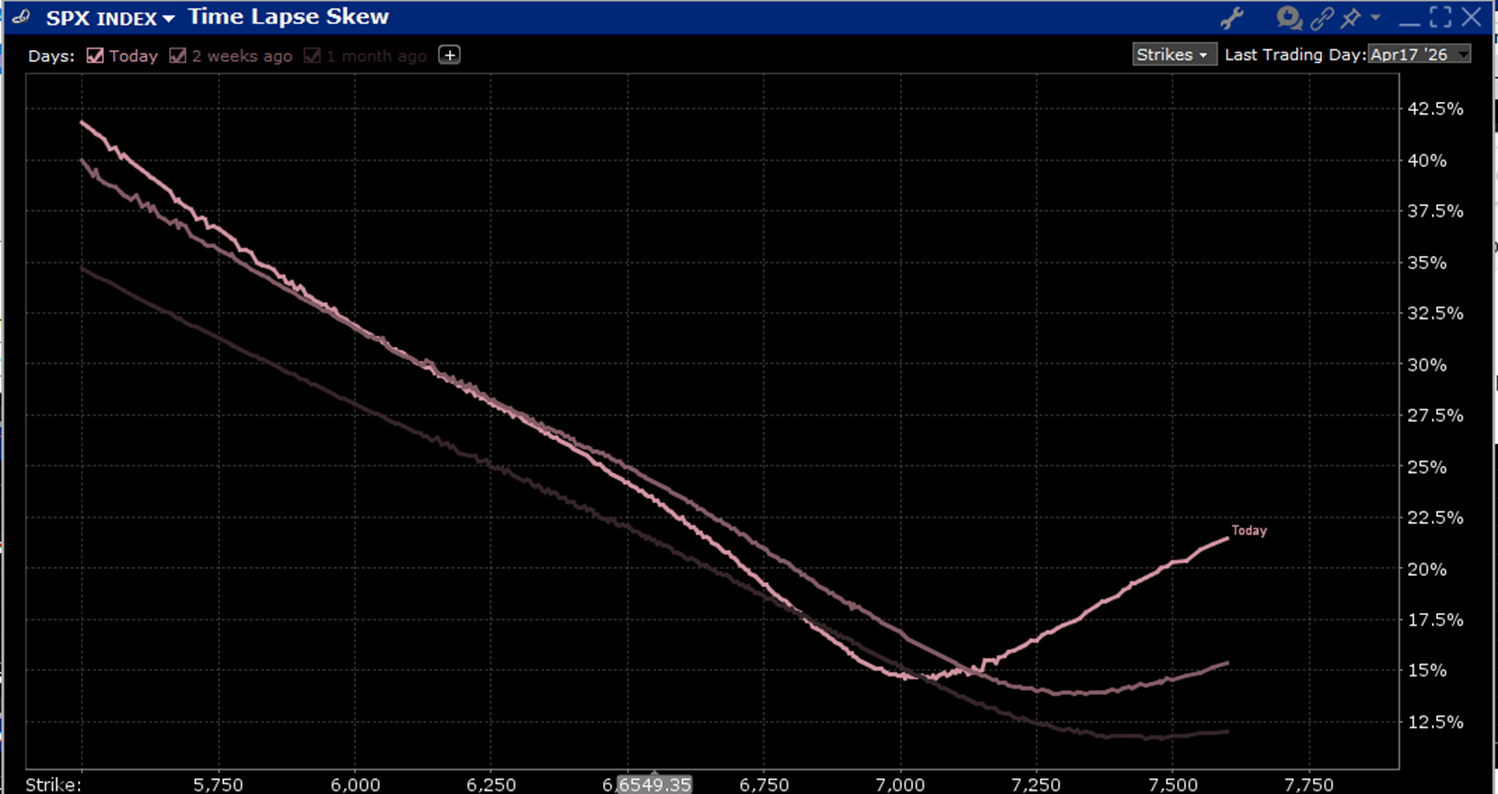

To be fair, fewer traders are comfortable trading from the short side than the long. It’s quite understandable. Markets go up over time and the economics of going long tend to be more favorable than the opposite. Yet the repeated attempts to chase rallies that ultimately fade tell us that no one really wants to risk being caught severely offsides. This is one of the possible explanations for the change in SPX options skew over the past month. It is clear why volatility overall and downside skew have risen. But we also see upside skew increasing dramatically.

SPX Skews, Today (brightest), 2-Weeks Ago (less bright), 1-Month Ago (faintest)

Source: Interactive Brokers

It appears that the key hedging activity is to the upside. Some traders seem willing to use the playbook outlined above, but only if they can protect themselves from the potential of a war-ending rally. They’re certainly paying high premiums for that insurance. Can you blame them? Indeed, even the pessimists are displaying a streak of optimism, whether they fully believe it or not.