Markets spent the week taking their cues from Middle East rumors and intrigue, with the ongoing conflict in Iran acting as the primary driver of both sentiment and price action again. For as long as the conflict stretches on, there will be little else that will dominate the market psyche, so get used to it.

Early optimism around a potential ceasefire briefly lifted equities and bonds, but that relief faded quickly as negotiations appeared to stall. The result was a volatile environment where oil prices held the reins for nearly all asset classes, although Anthropic caused a little damage to software and cybersecurity names, too.

U. S. equities finished the week mixed but broadly weaker. The S&P 500 declined by roughly 2%, weighed down in part by continued pressure on mega-cap technology stocks. The NASDAQ also extended its losses, now firmly in correction territory after falling 11% from its prior peak. The Dow Jones Industrial remained relatively steady, while the S&P MidCap 400 and Russell 2000 managed to post gains and snap four-week losing streaks.

This divergence emphasizes the persistent shift in leadership, with large-cap growth lagging and value-oriented segments holding up better for a third consecutive week.

The slide in Treasury markets may be the most unsettling. Yields pushed higher during the week, with the 10-year approaching 4. 5%. This past week’s 2-year Treasury auction was disappointing, sending yields 9 basis points higher to 3. 925% and posting the worst demand since May 2024. Investors are increasingly focused on the inflationary implications of rising energy prices, which has also led to a modest uptick in rate hike expectations. Markets are only pricing in a small probability that the Federal Reserve will tighten policy this year, but it’s still a major swing from six weeks ago. Actual tightening of any kind, as opposed to just hawkish messaging, remains a remote possibility. However, investors must face the fact that the Fed will remain cautious this year, and at least until conditions noticeably improve.

Inflation pressures reignite

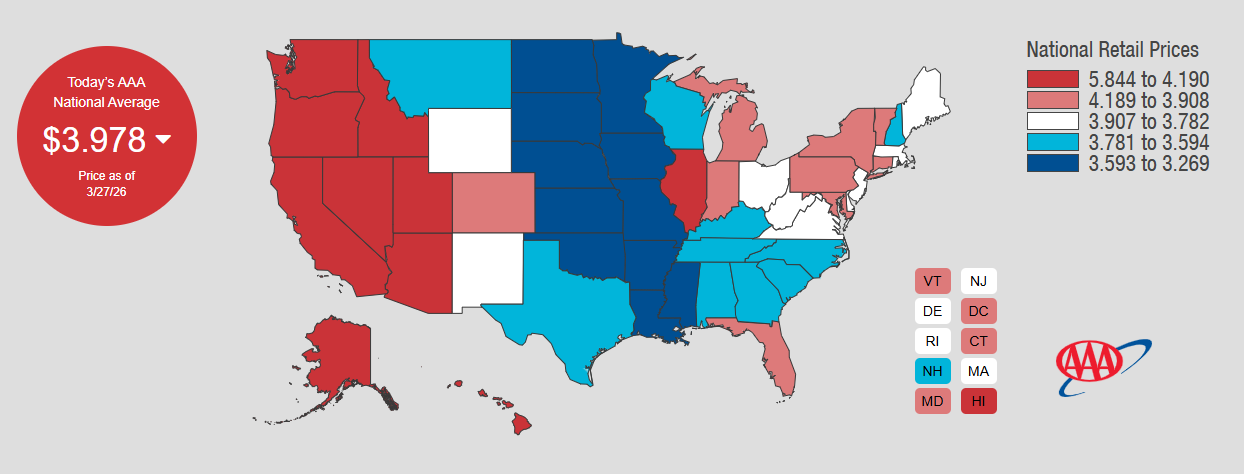

The most immediate economic impact of the conflict is being felt at the gas pump. National average gasoline prices have surged to nearly $4. 00 per gallon, up sharply from $2. 98 only a month ago. Diesel is up to almost $5. 40, up from $3. 76 last month. While energy represents a relatively small share of the consumer price index, its ripple effects are broad, feeding into transportation, food, and utility costs.

Source: AAA Fuel Prices

As a result, headline inflation is now expected to rise to around 3. 5% year-over-year in the coming months. This marks a clear interruption in the disinflation trend that had been gradually bringing price growth closer to the Fed’s 2% target. Encouragingly, core inflation is expected to rise less sharply but still stay above 3%. While painful, the underlying trend will remain far more stable than either the 1970s, 1980s, or 2022.

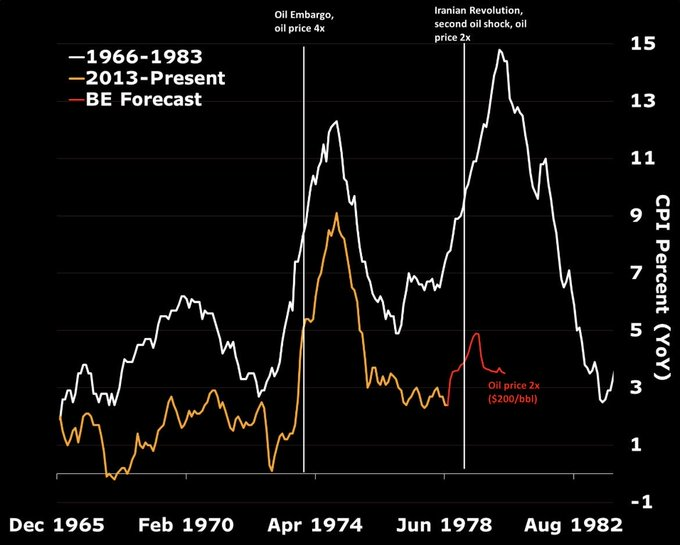

Anna Wong posted an excellent forecast chart for how $200/barrel oil prices would impact inflation. If you’ve seen the overlay of 2020s and 1970s inflation over the past year, this should look familiar. Let’s put this piece of Doomer propaganda to bed once and for all.

“[T]he red part of the forecast out to 2027 under the scenario that oil goes to $200/bbl. It will take a lot to get a 1970s redux. Even $200/bbl oil won’t do it. ”

Source: Anna Wong, @AnnaEconomist

Just because we aren’t going to see soaring inflation doesn’t mean we aren’t going to see any. Business data is already reflecting pricing pressures. Unlike tariffs, there is no argument over who is paying what.

The latest Purchasing Managers’ Index (PMI) showed a slowdown in overall activity, with the composite reading falling to an 11-month low. Firms reported the fastest increase in input costs in ten months and passed those costs along at the quickest pace since 2022. This combination of slower growth and rising prices is a headwind, but it is not yet signaling a broad deterioration in economic conditions.

Cracks worth watching

Despite rising prices, the consumer remains the driving force within the U. S. economy. While sentiment has weakened, it has not collapsed. The University of Michigan’s consumer sentiment index declined in March but remains above 2025 lows. Households are concerned about both current conditions and the future outlook all over again, yet they are still spending. 1-year inflation expectations moved higher, marking the largest monthly increase in nearly a year.

Hard data hasn’t completely cracked, and household balance sheets are still solid. The labor market continues to hold steady, with no indication that layoffs are accelerating. Jobless claims remain stable, and while weak hiring continues to punish job seekers, there is no clear evidence of faltering employment conditions. As I said to the Schwab Network this week, we're still in an uneasy equilibrium for the foreseeable future.

The longer geopolitical unrest pushes prices higher, the more risk will be building at the margins. Tax cuts were expected to offer some cushioning for stretched household budgets, but now they might barely paper over the spiking inflation. Higher energy costs act as a tax on consumers, and rising mortgage rates could weigh on housing activity just as the spring season begins. Investment in AI infrastructure could help offset some of that weakness in other parts of the economy, but that trick can’t last forever without a measurable return on investment in the next 18-24 months.

Central banks seek balance

The Federal Reserve finds itself in a frustratingly familiar and uncomfortable position. Higher energy prices are pushing inflation up, while they also weigh on growth. This creates a difficult trade-off, and so far, the Fed appears inclined to sit on its hands through the near-term inflation spike. The next CPI and PCE reports could change that.

Current pricing suggests only a small chance of a hike this year, and those odds have little predictive power right now. No one has an edge on how conditions will evolve, so take it all with a grain of salt. Compared to the hawkish expectations in Europe and Japan, the Fed seems downright Zen. The Fed’s balanced stance has helped prevent a more significant tightening in financial conditions, which will make Kevin Warsh’s plan to unwind it that much harder (assuming he gets the chance at all—where is he by the way?).

Looking ahead, the path of Fed policy will depend heavily on energy prices and the evolution of the conflict. A sustained rise in oil could complicate the outlook, while any de-escalation could shift the narrative back to where we were at the end of January.

What this means for investors and what’s next

All eyes now turn to the upcoming JOLTS and payroll reports, which will provide a timely read on the labor market’s resilience. Expectations call for modest job growth and a stable unemployment rate, which would help calm concerns following February’s shocking data.

At the same time, markets will continue to monitor the developments in the Middle East, with oil prices jerking the wheel for equities, bonds, and inflation expectations. For investors, the key takeaway is that volatility may persist, but it is being driven by a narrow set of factors rather than a broad deterioration in fundamentals. If earnings expectations hold, valuations are improving.

The S&P is down 8. 74% from its January all-time high. If you’re getting nervous, you’re either getting impatient or you’re overleveraged. Exiting markets now means you risk sitting out the future recovery. If the past few years prove anything, the move higher will be swift and unrelenting. There is no way to know when that is happening, but it will happen. Staying focused on long-term objectives remains the most reliable strategy in a market that is reacting more to headlines than to any clear structural change.

If you don’t have the time or the constitution for that, choose sector rotation or rebalancing over outright selling. One way or another, the oil pressure will come down.

Torsten Slok of Apollo struck an optimistic tone on Friday morning:

Markets are overreacting to what will likely be a 4- to 6-week period of volatility, which will ultimately result in 50 years of stability in oil markets, supply chains and geopolitics. . . The bottom line is that the Iran shock is not big enough to offset the strong tailwinds to the US economy from AI spending, the industrial renaissance and the One Big Beautiful Bill.