To clear up that headline, the sector being referenced here is financial services, but “bank” was used for the purposes of alliteration. The second-largest sector weight in the S&P 500 merits consideration today because following the August jobs report, it appears the Federal Reserve has no choice but to lower interest rates this month.

Throw in the fact that there are now more unemployed folks in the U. S. than job openings and it’s not a stretch to say the Fed doesn’t have much room to dither when it comes to propping up the economy. Predictably, financial services stocks and funds are relevant in this conversation, but not for the reasons many think.

Old school investing wisdom holds that banks and insurance providers, two of the largest industrial weights in the financial services sector, are beneficiaries of higher interest rates because that scenario lifts net interest margins for those companies.

So in theory, the last several years should’ve been a rewarding time in which to own financial stocks and exchange traded funds such as the Financial Select Sector SPDR (NYSE: XLF) and it has been. Since the start of 2022, the year in which the Fed set out on its rate-tightening campaign, XLF is higher by 45. 5% (as of Sept. 5), slightly ahead of the 42. 9% returned by the S&P 500 over the same span. However, that doesn’t mean XLF and friends will be doomed by rate cuts. Actually, the opposite could be true.

Believe It: Rate Cuts Help Banks

Some sectors, such as real estate and utilities, are viewed as clear rate cut winners so it may surprise some investors to learn the same is true of financial services.

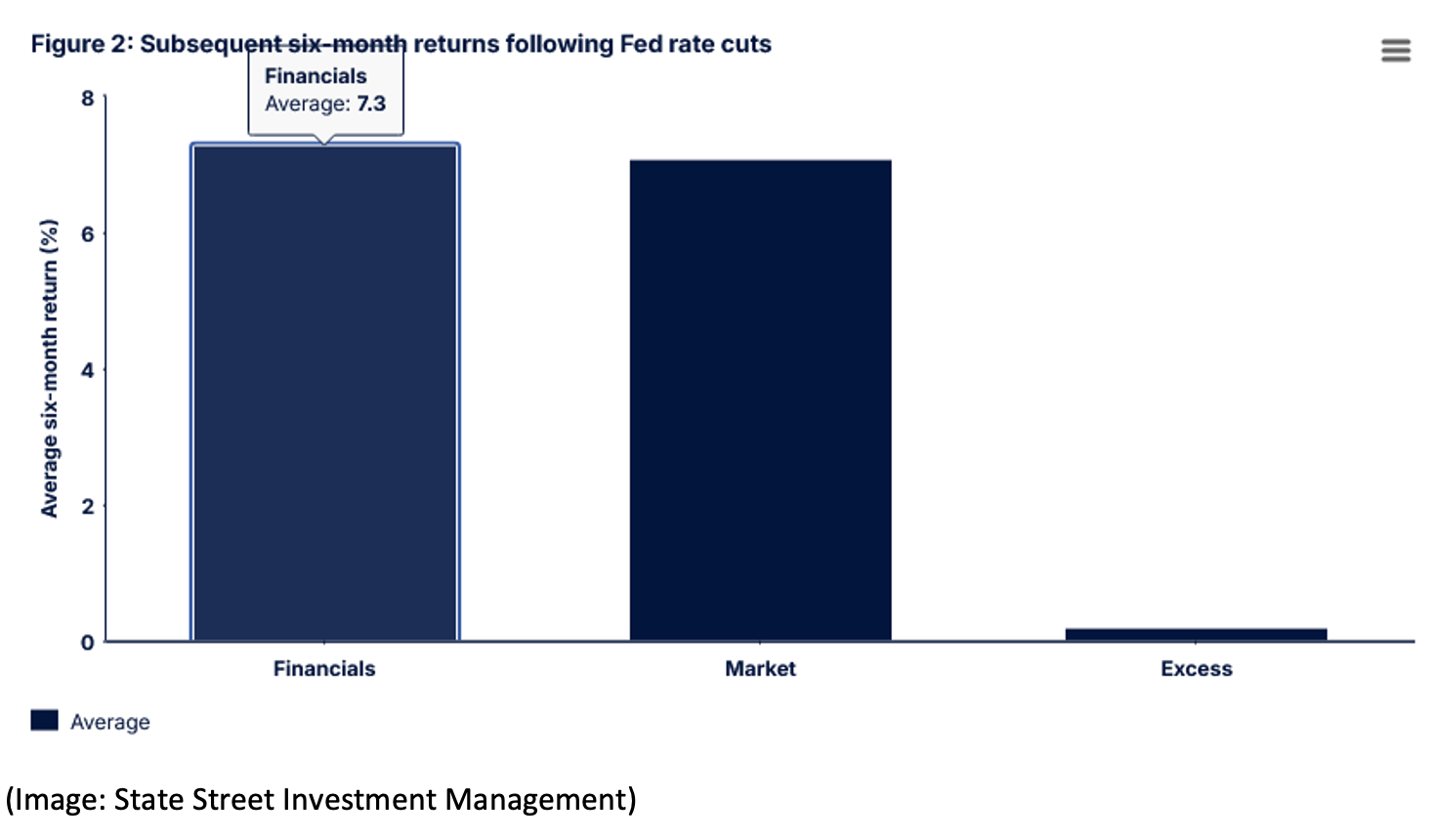

“Analyzing the six-month returns following every Fed rate cut since 1970 shows that Financials’ average six-month return following a Fed rate cut was 7. 3%. This compares favorably to the market’s average 7. 1% return,” notes Matthew Bartolini of State Street.

(Image: State Street Investment Management)

Alright, so naysayers are apt to say that some of financials’ post-rate-cut performances is attributable to the Fed taking action following a recession, which often acts as a rising tide lifting all boats. But even when stripping out recessionary periods, financial stocks shine after Fed easing.

“The bias to these returns (absolute and excess) skews positive. In non-recessionary periods when the Fed cut rates, returns were positive 75% of the time (versus 70% positive in all periods),” adds Bartolini. “And Financials outperformed the market 60% of the time, both in recessionary and non-recessionary periods. ”

Financials Have Tailwinds

While not as glamorous as technology and communication services, the financial services sector doesn’t lack for tailwinds, including recent news that banks are expanding shareholder rewards efforts after passing the Fed’s stress tests.

There’s more to the sector’s fundamental story. In the second quarter, 87% of its components beat earnings estimates, the second-best rate among the 11 sectors, according to State Street. Eighty-three percent of the group’s components have issued positive full-year guidance, also good for second-best among all sectors. Throw in a steeper yield curve, which could be amplified by rate cuts, and the stage could be set for upside by financial stocks.

“A steeper yield curve (lower rates on the short end and higher rates on the long end) can benefit Financials’ profitability and net interest margins (NIMs),” concludes Bartolini. “Borrowing short term and lending long term is a crucial funding dynamic for banks and financial institutions. While US banks’ NIMs rose slightly to start the year, they remain below pre-pandemic levels—indicating the potential for further improvement. ”