A DST advisor's paycheck shouldn't depend on which investment they recommend. When they earn commissions from sponsors, their financial incentives conflict with clients' best interests. A fee-only DST advisor changes that dynamic entirely. You pay a transparent fee for advice, they recommend the best options without hidden agendas, and your money works harder because commission loads aren't eating into your principal.

The Hidden Costs of Commission-Based Advice

Commission-based advisors operate under a "suitability" standard that requires them to recommend investments for your situation. This sounds reasonable until you realize suitability may not mean "best for you. " It can mean the product fits your profile well enough to justify the sale. A fee-based financial planner might earn commissions from specific DST sponsors while also charging advisory fees, creating a dual incentive structure that prioritizes their payout over your net return.

The DST commission structure typically embeds fees into the investment to reduce your initial capital deployment. Commission-based compensation creates financial incentives that can conflict with client interests when advisors receive payments from investment sponsors.

If you invest $1 million into a DST through a commission-based broker, up-front loads reduce the amount actually working for you before a single distribution arrives. You're building wealth on a smaller foundation, while the advisor profits from the transaction itself.

When clients discover their advisor recommended a particular DST because it paid higher commissions than comparable offerings, trust erodes quickly. Your reputation as a financial professional depends on acting in your clients' genuine interests. Commission structures create inherent tension between doing what's right for the client and maximizing your own compensation. That becomes a liability when sophisticated investors start asking pointed questions about how you get paid.

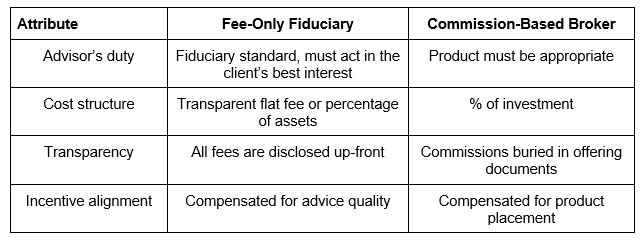

Fee-Only vs. Commission — A Clear Comparison for Your Practice

Understanding the structural differences between advisor compensation models helps you serve clients more effectively. The DST commission structure and fee-only models create vastly different incentive systems. Where commission-based brokers earn compensation tied to specific product sales, a fee-only DST advisor charges a transparent fee for services rendered.

The Legal Fiduciary Standard

A fiduciary operates under the highest standard in financial services. They have a legal obligation requiring them to put their clients' interests ahead of their own through two essential components — a duty of loyalty and a duty of care.

Advisors must avoid conflicts of interest and disclose unavoidable ones under the duty of loyalty. Under the duty of care, they exercise the competence and diligence expected of prudent professionals. Together, these obligations create a framework in which your client's financial well-being takes absolute priority over your compensation preferences.

How a True Fee-Only DST Advisor Aligns with Your Client's Best Interest

Fee-only fiduciaries like Sera Capital demonstrate how this model works in practice. It specializes exclusively in DST and 721 UPREIT exchanges, with these strategies representing over 90% of its work. One of the nation's largest wealth management organizations chose them as a preferred 1031 and 721 exchange specialist precisely because the fee-only structure eliminates product-pushing incentives.

Operating on flat fees rather than commissions allows firms to evaluate DST offerings from multiple sponsors without bias. Sera Capital's consultative approach prioritizes education and strategy over sales. High-net-worth families receive dedicated time to understand the nuances of Delaware Statutory Trusts and how a 721 UPREIT structure might serve their long-term estate planning goals.

The "family helping families" ethos becomes genuine when compensation is not tied to steering clients toward high-commission products. Before recommending any investment, a fee-only DST advisor evaluates your entire situation.

Comparing offerings across sponsors, analyzing fee structures and assessing how each option affects the tax position and estate planning objectives delivers unbiased guidance. You receive the same quality advice regardless of which DST you ultimately choose because the advisor earns the same fee.

Frequently Asked Questions on Fee-Only DST Advisory

These practical questions address specific concerns advisors and their clients raise about fee structures and fiduciary obligations.

How do different fee models impact a DST investor's long-term returns?

The math reveals significant differences over time. Assume you invest $1 million in a DST. Under a commission model with a 5% up-front load, only $950,000 actually deploys into the property. Fee-only financial advisors might charge a 1% advisory fee of $10,000, leaving $990,000 working for you.

Over 10 years, assuming a conservative 6% annual return, your commission-based investment grows to approximately $1. 7 million. By comparison, the fee-only investment reaches roughly $1. 77 million. Instead of going to broker compensation, that $70,000 difference represents wealth that stays in the family. The gap widens further when you factor in the compounding effect on distributions throughout the holding period.

What is the difference between a DST sponsor and a DST advisor?

A DST sponsor creates and manages the investment offering. Their primary objective is to place capital into their properties to earn management fees and promote compensation through property acquisition, structuring the legal entity and handling ongoing operations.

An advisor's function is different. Your advisor evaluates offerings across multiple sponsors to find the best fit for your situation. When affiliated with a sponsor, representatives are incentivized to recommend their company's DSTs even when another sponsor's offering might better serve your needs. Without preferential treatment for any particular sponsor's products, an independent fee-only advisor compares all available options.

How can investors verify an advisor's fiduciary status?

Start by requesting the advisor's SEC Form ADV Part 2A, also known as the Brochure. Explicit language stating "we have a fiduciary duty to our clients" or similar phrasing should appear in the document. The compensation section reveals whether the advisor receives commissions, referral fees or other product-based payments.

The SEC's investor bulletin on questions to ask when hiring financial professionals provides a helpful starting point. Ask whether they receive any compensation from DST sponsors, property managers or other third parties. Understanding the distinction between Regulation Best Interest for brokers and the fiduciary standard for investment advisers requires reviewing the standards of conduct of the SEC.

The SEC's Investment Adviser Public Disclosure database shows the advisor's registration status and adherence requirements. Registered investment advisers must adhere to fiduciary standards, while broker-dealers operate under the less stringent suitability requirements.

The Path to a More Trustworthy Investment Experience

Choosing a fee-only fiduciary for your DST investments protects your interests and eliminates conflicts that can diminish returns. You deserve an advisor whose compensation aligns with your success. Evaluate your current advisor relationship and ask whether a fee-only model better serves your financial goals and long-term wealth preservation.