With tensions simmering in the Middle East and the global economy feeling the pinch of high energy prices, high-yield bonds might not be on every investor’s radar. In our view, they should be.

Valuations remain compelling, starting yields are elevated and corporate fundamentals—while softening—are coming off relatively strong levels. Technical conditions also remain supportive, with limited net supply and steady demand. As for today’s turbulent times, high yield has historically held up well in periods of low growth and has performed better than equities during market drawdowns.

Against this favorable backdrop, we see five opportunities taking shape in today’s high-yield market—plus one additional area worth watching.

1. BBB Quality at BB Yields

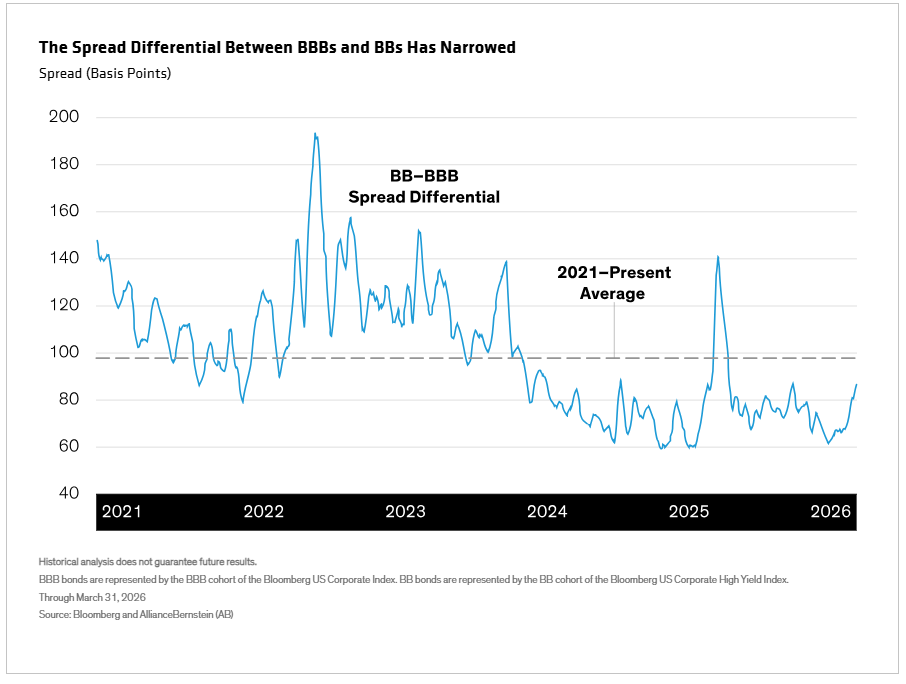

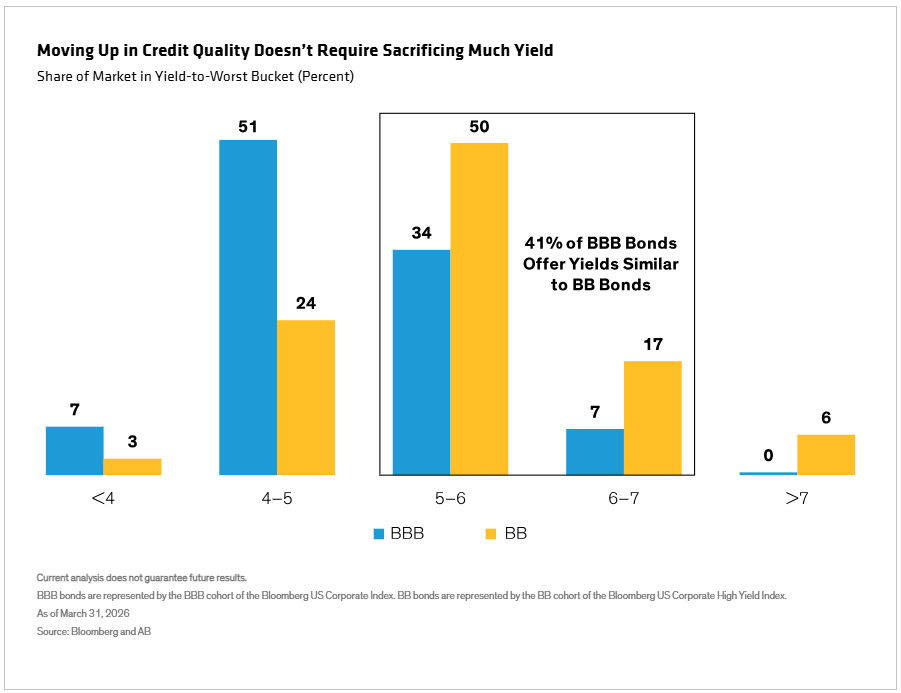

High-yield spreads are still tight by historical standards even after recent widening. With spreads this compressed, investors don’t need to sacrifice much—if any—yield to move up in credit quality. This can be seen in the historically narrow yield differential between BBB-rated bonds and BB-rated credits (Display).

Roughly 40% of the BBB market now offers yields comparable to BBs, providing similar income with less credit risk (Display).

Quality opportunities also extend to fallen angels—formerly investment-grade securities downgraded into the high-yield universe. Rating agency activity has skewed to the downside, with downgrades outpacing upgrades and fallen angels outnumbering rising stars. Historically, fallen angels have tended to outperform following their transition into high yield.

2. Conviction Required in CCC Bonds

In our view, the lowest rung of high-yield universe requires the most stringent due diligence. Roughly one-quarter of CCCs trade at distressed levels, with spreads of 1,000 basis points or more—implying significant default risk. But most CCCs offer insufficient compensation for that risk, underscoring the need for strong, research-driven conviction when identifying the few attractive opportunities that do exist.

3. US Consumer Cyclicals

Despite higher energy prices, consumer spending has stayed resilient in the US—particularly among higher-income households. These consumers disproportionately support discretionary industries such as gaming, lodging and retail. Spreads in these industries have widened relative to non-cyclicals, creating more attractive valuations. That said, investors should be selective.

4. Caution in Communications and Tech

To us, valuations look stretched in parts of communications and technology, where structural headwinds are making risk harder to justify. Communications companies face shrinking subscriber bases and high debt burdens, while many tech issuers have added leverage even as growth slows and interest expense rises. We think investors should be cautious when it comes to these industries.

However, some software issuers may be an exception: software recently sold off on concerns about AI disruption—creating a dislocation that, in our analysis, may justify selective holdings at attractive levels.

5. North and South American Midstream and E&P Issuers

With energy prices elevated, we think both midstream and independent exploration and production (E&P) companies warrant a closer look. We favor midstream issuers in North and South America, which are less exposed to Middle East supply disruptions and may benefit from higher oil prices, rising energy demand and a looser regulatory environment in the US.

Independent E&P issuers also stand out after strengthening their balance sheets in the years following the COVID-19 pandemic. In addition, rising M&A activity in the energy sector may provide upside for bondholders in the event of a corporate action.

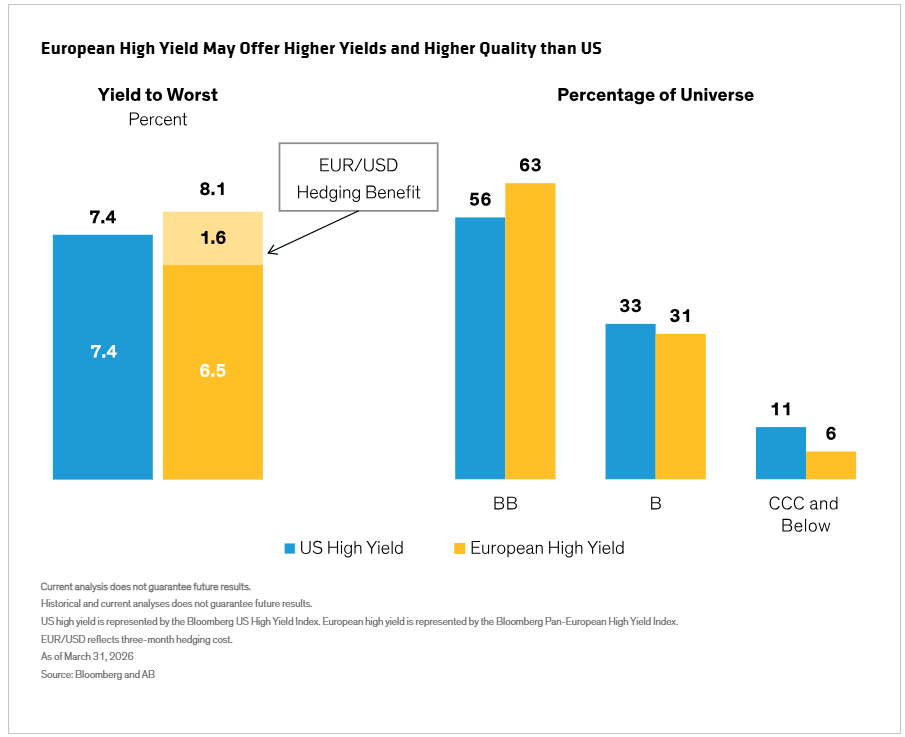

Bonus Opportunity: Select European Issuers

High-yield opportunities can be found globally, and Europe stands out on a relative basis. For US dollar-based investors, European high yield offers a yield-to-worst of 8. 1% when hedged into US dollars—70 basis points higher than the US market (Display). Europe also skews toward higher-quality issuers than the US, with more BB-rated credits and fewer CCCs.

Selectivity remains critical, however. Growth prospects in Europe may be more challenged than in the US, reinforcing a preference for defensive credits that are likely to face fewer cyclical headwinds.

For high-yield investors, the word of the day is judgment. Today’s backdrop is supportive, yet nuanced—which is exactly when disciplined, active credit selection can matter most.