April closed with a powerful statement from equity markets. In an impressive show of resilience, markets continued to look past headlines and focus on hard data. The S&P 500 surged 10% for the month, its strongest gain in years. Despite rising oil prices, sticky inflation, ugly consumer sentiment, and a cautious tone from the Fed, there was just no holding the market back last month.

That may seem counterintuitive at first glance, but the explanation is becoming clearer as we see example after example of a market that seems to bob and weave through crises like a prizefighter. Strong and accelerating corporate earnings continue to do the heavy lifting, helping investors look through near-term uncertainty and focus on underlying momentum. If forward projections are to be believed, Q1 will be the weakest quarter all year.

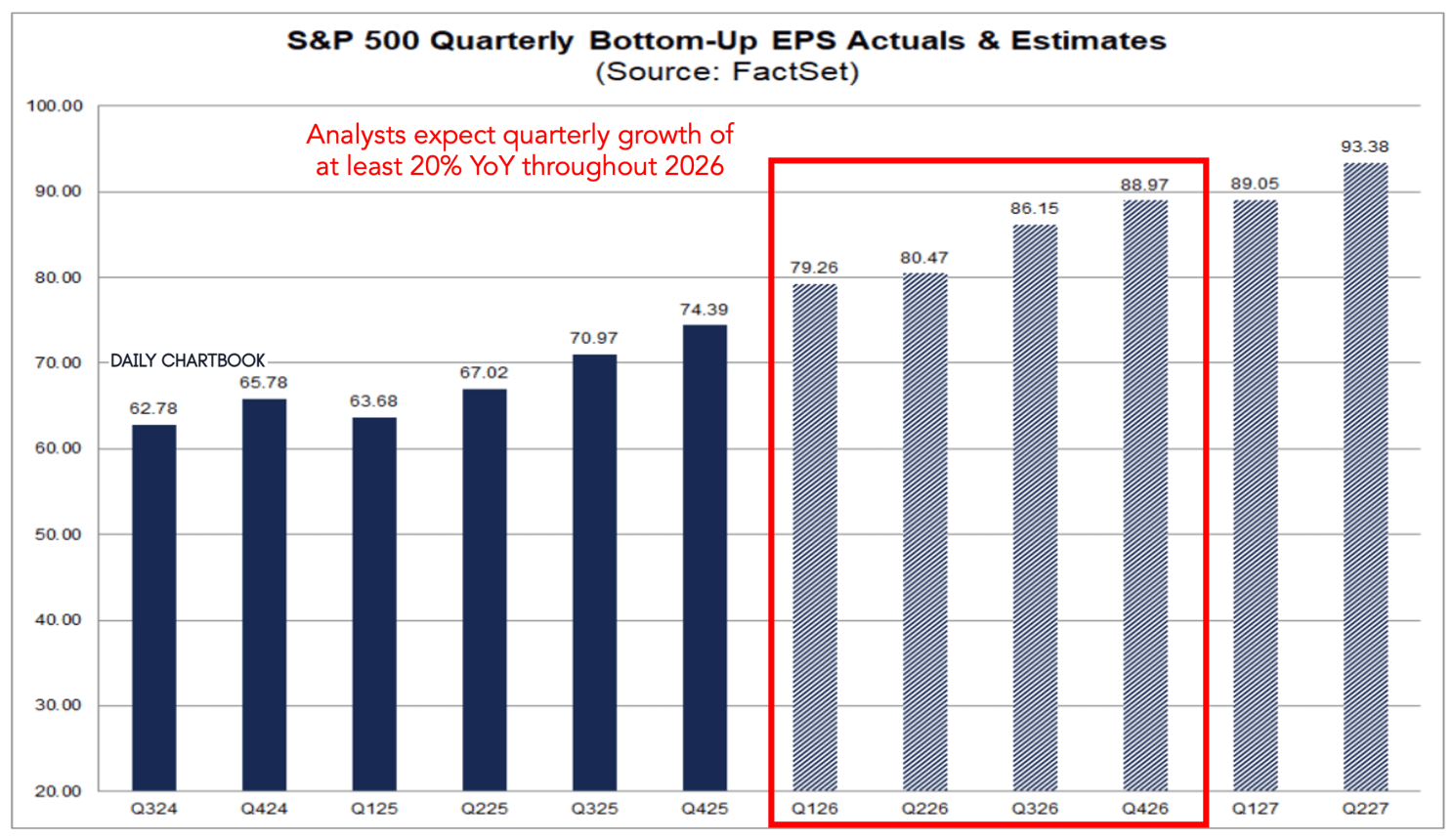

Source: FactSet via Daily Chartbook

This past week reinforced that trend. 25% of S&P 500 companies reported this past week, making up 44% of the total market capitalization of the index. Numerous mega-cap leaders such as Google, Microsoft, Amazon, Meta, and Apple (and more) reported. The overall message was consistent. Profits are holding up better than expected, and growth continues even as concerns of AI overhype simmer beneath the surface, which is keeping valuations more muted.

Earnings growth for the first quarter is tracking above 27% (! ), marking a sixth straight quarter of double-digit gains. Critically, this strength is not isolated to the Mag-7 companies like it was in 2025. Most sectors are participating, with technology, industrials, financials, and materials all contributing meaningfully. Even areas facing pressure from higher energy costs are showing only modest declines, with expectations for recovery already building.

The furious market rally throughout April reflects this encouraging backdrop, but also makes this another most-hated rally. Large-cap stocks continued to lead, but growth stocks lagged somewhat as rising oil prices supported the energy sector. Broader AI-related investment remains a seemingly unstoppable driver across the broader market.

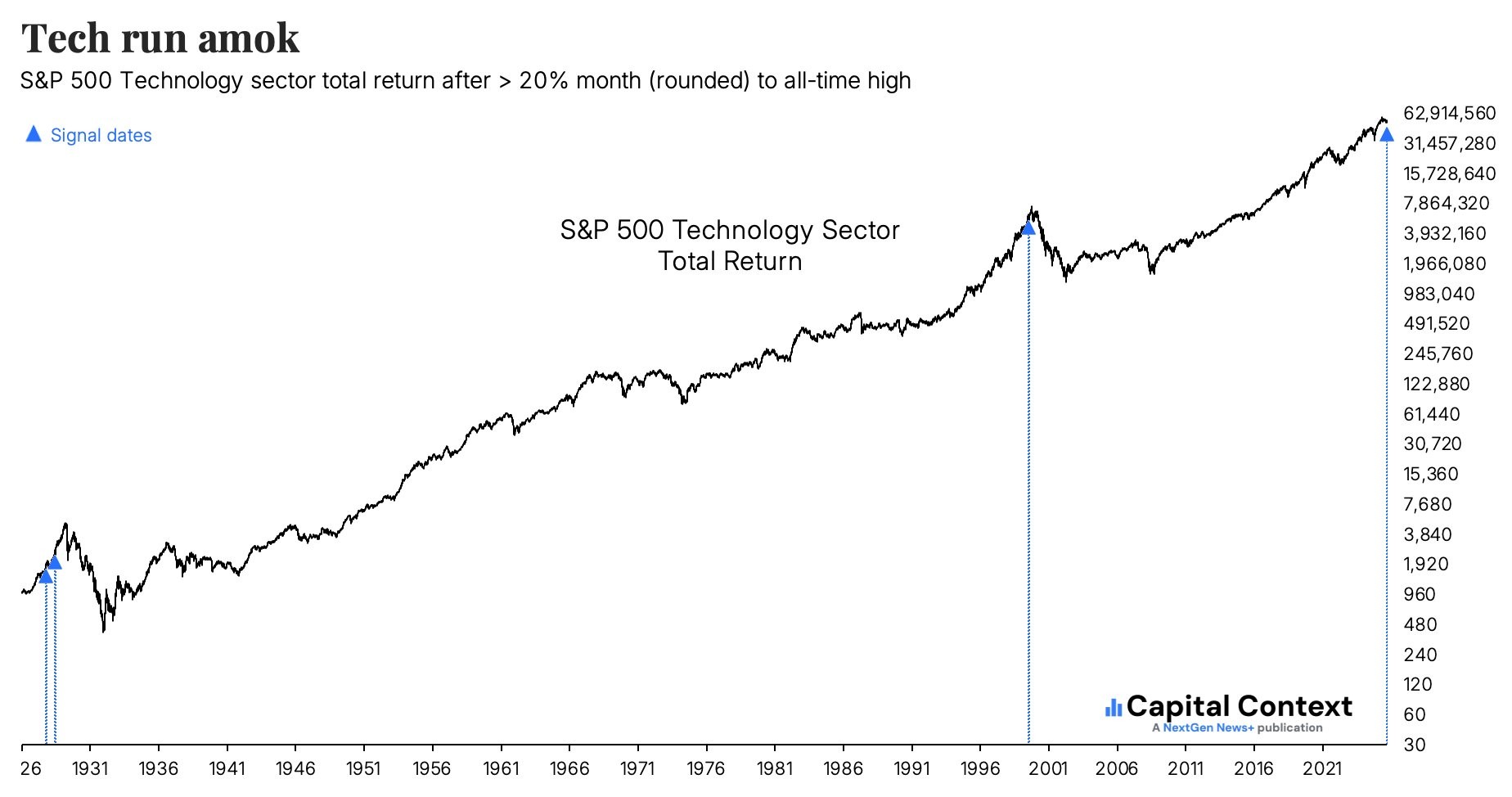

The scale of spending tied to AI infrastructure continues to expand, supporting both current earnings and future expectations. For now, the market appears comfortable betting that this trend has room to run even as comparisons to past market tops flourish on X.

Source: @jasongoepfert on X

A (mostly) resilient economy

Economic data is telling a similar, but slightly hazier, story. Growth remains intact, even if it is not without warts. First-quarter GDP came in at a 2% annualized pace, supported by strong business investment and steady consumer activity. Beneath the surface, private-sector demand looks even stronger, suggesting that the economy is holding up despite higher costs.

Consumer spending remains a key pillar that, unfortunately, sits precariously on a cliff's edge. While rising gasoline prices are starting to take a bite, higher incomes and tax refunds have helped offset the impact for now. There is little evidence of a meaningful pullback in demand so far, but if a slide starts, it will be hard to correct.

Conveniently, business investment continues to surge, particularly in technology and software. Nonstop investment and still-unmet demand for compute are reinforcing the role of AI as both a growth engine and a source of productivity gains. However, subtract the AI bonanza, and the economy would be slowly slipping below the waterline.

Inflation remains elevated, with core measures drifting further from the Fed’s target. The weed that just won’t die, successive shocks from tariffs, and now oil are adding to inflation pressure. The Federal Reserve acknowledged this tension, holding rates steady but signaling less confidence that cuts are imminent. Bond yields have moved higher in response. A growing divide among policymakers suggests that the path forward may not be straightforward, just as a new Fed chair takes the helm.

Jekyll and Hyde

Taken together, markets are navigating an uneasy push-and-pull environment. On one side, strong earnings and steady economic growth are providing support. On the other, higher energy prices, inflation concerns, and policy uncertainty are acting as troubling counterweights. While stocks are focused on corporate results, the bond market is responding to the economic risks. Earnings are winning the game, but the margin is narrowing, and there is plenty of time on the clock.

After such a strong run over the past few weeks, it is reasonable to expect some consolidation. It’s healthy even. The rally has been fast and, in some areas, narrow, with large-cap technology stocks doing most of the work. Market breadth has not fully kept pace, which can sometimes signal a need to pause and reset. When companies like Texas Instruments are posting an RSI above 70 for over two weeks, it’s time to ease up. That does not necessarily imply a reversal of any individual names, or the index itself, but it does suggest that the next phase may look different from the last.

What this means for investors and what’s next

The coming weeks will test the durability of this narrative. Earnings remain front and center, with more reports set to provide clarity on demand, margins, and investment trends. The monthly jobs report will offer another read on the strength of the labor market, while developments in the Middle East and oil prices remain key swing factors.

For investors, the message is relatively straightforward. The backdrop is constructive, but not without risks. Strong earnings provide a cushion, but they do not eliminate uncertainty. One out-of-left-field headline (or missile) could end the party quickly. Staying diversified and focused on longer-term trends remains the most reliable approach. With some insane run-ups in some names, clarify your exit strategies on overweight positions now.

It’s 10 PM, do you know where your risk exposure is?

Markets may not move in a straight line from here, but as long as profits continue to grow, the foundation stays intact for long-term growth.

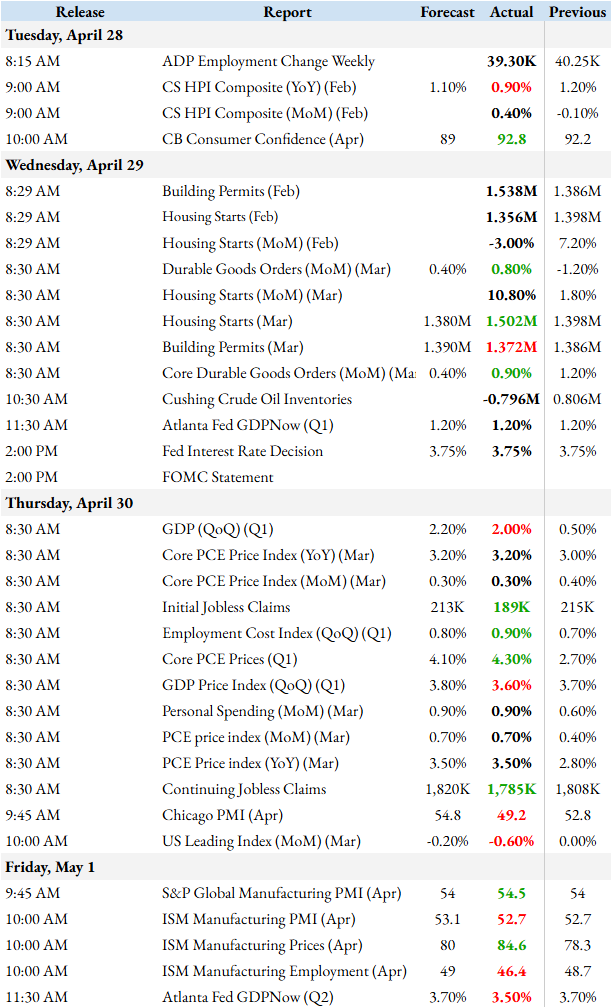

Economic Reports

Earnings Releases