We’ve certainly discussed the changing outlook for Federal Reserve rate cuts, but we have been remiss in noting the similarly changing perceptions in many other key global economies. Indeed, while the market has essentially priced out rate cuts in the US, traders are expecting serial hikes from other major central banks. Considering the magnitude of the changing perceptions, one might be tempted to wonder whether stock markets are too sanguine under the circumstances.

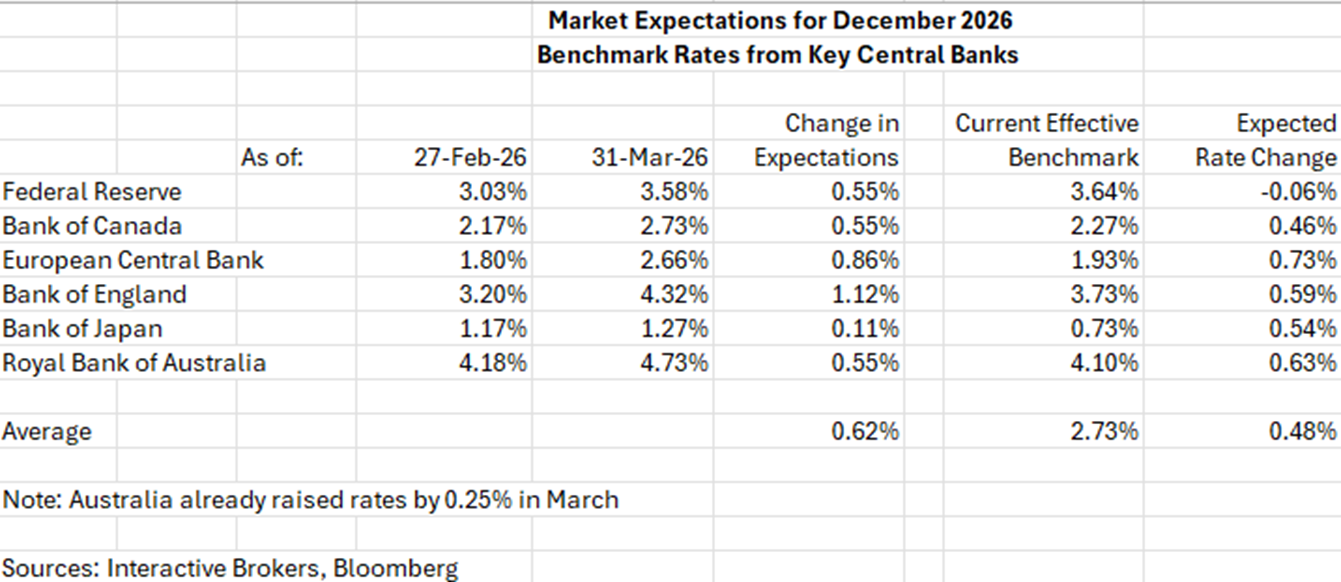

Many of you are familiar with the notion that rate cut expectations in the US have plummeted since the outbreak of hostilities in the Persian Gulf, but I doubt that as many are abreast of the global interest rate outlook. Perceptions for the rest of the world have moved quite similarly. The outlook for the December Fed Funds rate has risen by 55 basis points, meaning that slightly more than two rate cuts have been priced out of the market. As the table below shows, this is commensurate with the changed perceptions that we see in several other key markets, with Japan as the outlier.

The starting point for US expectations was vastly different than we saw in most of these other economies. Indeed, as we priced out rate cuts in the US, that still leaves expectations quite stable. Fed Funds futures are pricing in a target rate for December that is only fractionally lower than the current effective Fed Funds rate. (ForecastEx traders anticipate a modestly higher chance of a rate cut by December, with a 22% “Yes” for one cut by then. )

In Canada and the Eurozone, traders expected rates to remain relatively stable throughout the year, but now they price in roughly two and three hikes, respectively. Australia was pricing in a hike, but for later in the year. The current 4. 1% effective rate includes a 25-basis point hike that occurred at the RBA’s March meeting, and now another two are priced in by December. The move in UK perceptions was even more extreme, with two anticipated cuts now turning into two expected hikes. Only in Japan, a perpetual outlier, have perceptions remained quite stable. A bit less than two hikes were priced in before; a bit more than two are priced in now.

Against that backdrop, first, it is not surprising that short-term rates have risen around much of the globe. They are simply pricing in the new benchmark rate paradigm. Second, that is why expectations for dollar strength have not been fully realized. There is indeed a bit of a flight to safety bid, but if interest rates in other countries are set to rise, then the relative advantage of the dollar is minimized.

Finally, although global stock markets have swooned since the end of February, the last day before the conflict began, I would argue that this is another reason to assert that the reactions have actually been more benign than one might have expected. Let’s do a little thought experiment. Suppose I told you about six weeks ago that we would not be getting any rate cuts in the US and that several major central banks would be raising rates by a half-percent or more. How much of a drop in stocks might you have expected? Would single-digit percentage drops seem relatively fair, or in fact a bit small under the circumstances? Consider your answer to those questions when you assess whether stocks have fallen too much, too little, or about right.