For the third day in a row, bond yields have taken center stage in investors’ minds. Over the past few days, we have seen yields move steadily higher. This is something we noted one week ago after the higher-than-expected CPI report, and the global bond rout that took hold on Friday has not yet relented. In turn, that has punctured stock market valuations, with the semiconductor sector bearing the brunt. The tech trade gets a key test after tomorrow’s close when Nvidia (NVDA) reports earnings.

Before we delve into market expectations for the stock that has been the key pillar for the AI-related investment that has powered the three-and-a-half-yearlong bull market that coincided with the launch of ChatGPT, we need to once again address the ramifications of the bond selloff.

Inflationary expectations, many of them stemming from the side effects of the closure of the Strait of Hormuz, have been a key spur for higher short- and longer-term rates. According to Bloomberg data, overnight index swaps are now pricing an 82% chance for a 25-basis-point hike by December and more than a 100% chance for one by January. For comparison, on February 27th, the day before the start of the war, 2 full cuts plus a 43% chance for a third were priced in for December. The implied rate for December rose from 3. 03% to 3. 83% in that period. That basically explains the 75-basis-point jumps in 2-year and 10-year Treasury yields that we’ve seen since the end of February.

While stocks and bonds need not move in lockstep, higher yields have meaningful ramifications for equity valuations. It is typical to value shares as the present value of a company’s future stream of earnings, dividends, and/or cash flows. The higher the long-term interest rate, the lower the present value of those streams. Improved current earnings and near-term guidance were a key, highly valid rationale for the recent bump in stock prices, and in many cases, they were extrapolated into significantly improved current valuations. Yet if we can base improved valuations upon higher earnings, we should also expect some deterioration in valuations when interest rates increase.

This is where NVDA earnings become critical. As noted above, the current bull market has been powered by enthusiasm for the promise of generative artificial intelligence and the billions of dollars spent to achieve the new technology’s promise. NVDA has been at the forefront of that spending from the start. Thus, NVDA’s earnings have been considered among the most, if not THE most, important single earnings release each quarter. If Jensen Huang and his team report that they continue to be the recipients of copious spending by AI hyperscalers and developers, then that should have positive ramifications for the entire semiconductor sector. If not, then a potentially overstretched sector, which rose 70% from the end of March through last Monday before dipping about 7. 5% in the past week, could bear the brunt.

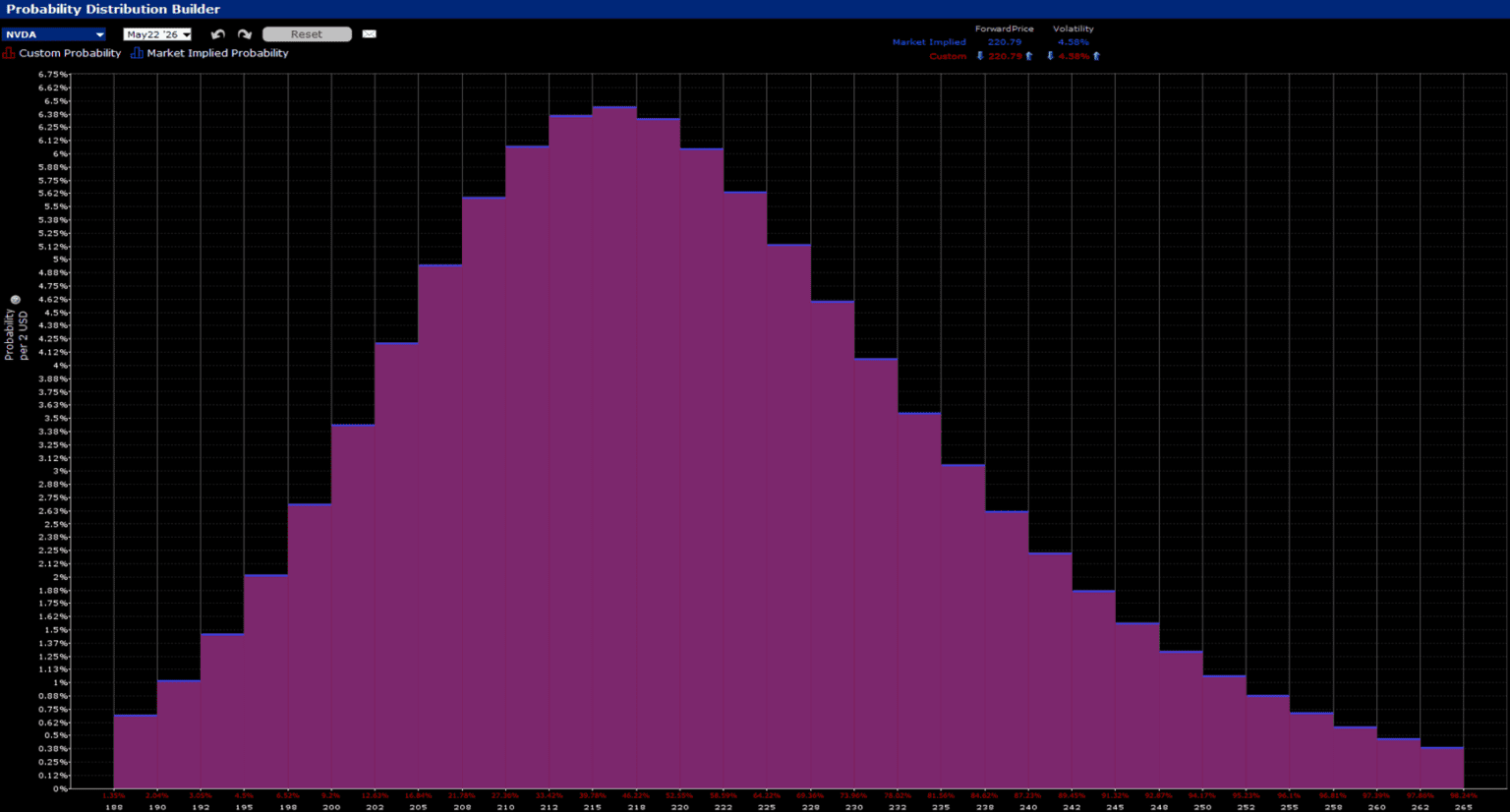

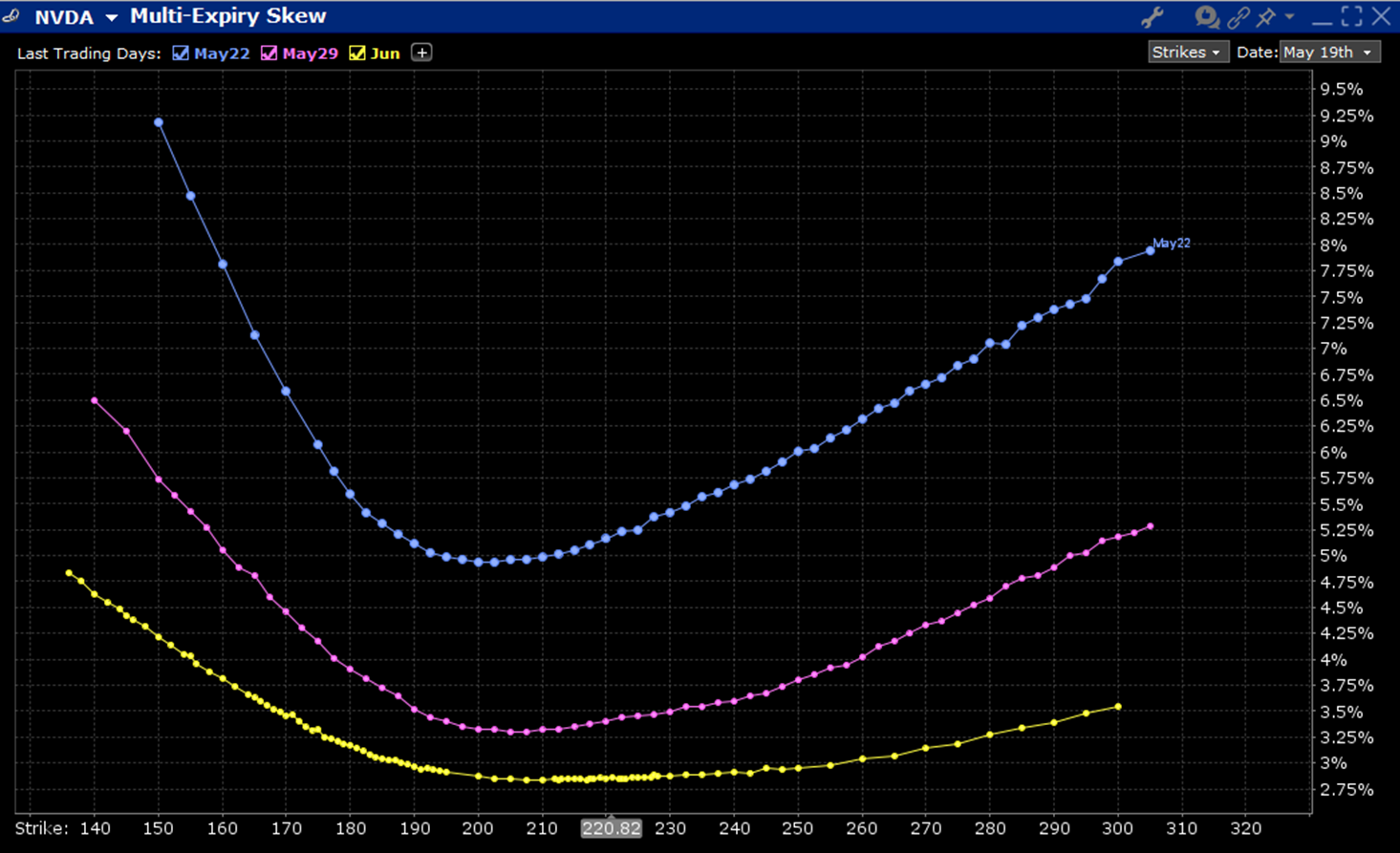

Equity options traders don’t seem particularly concerned about the latter case. For NVDA options expiring on Friday, the IBKR Probability Lab shows a peak outcome in the $215-$217. 50 range, just below the current $220. 59 stock price. The at-money daily volatility for that expiry is about 5. 2%, which is a bit higher than its 6-quarter average post-earnings move of 3. 61% (-5. 46%, -3. 15%, -0. 79%, +3. 25%, -8. 48%, +0. 53%), but not inappropriately so. Many of us remember the seemingly routine double-digit jumps in NVDA during 2023, but we haven’t seen one since a +16. 4% move after February 2024’s report. Skews are asymmetric, but the lowest implied volatilities can be found at roughly 10% below the current stock price, and they move steeply to the downside and amply to the upside.

The takeaway from NVDA options, at least so far (things can and do change in the hours just before an earnings report), is that traders are not particularly concerned about major ramifications for either that stock or the indices in which it has the largest weight. We’ll see if that proves to be appropriate by late tomorrow afternoon.

IBKR Probability Lab for NVDA Options Expiring May 22nd, 2026

Source: Interactive Brokers

Skews For NVDA Options Expiring May 22nd (blue), May 29th (purple), June 18th, 2026 (yellow)

Source: Interactive Brokers