Prudent investors have long been concerned about “black swans” – low probability, high outcome events that could abruptly unravel market dynamics. One of the classic black swans was the closure of the Straits of Hormuz, disrupting global oil supplies and creating an inflationary spiral. That black swan arrived over the weekend, yet the consequences have so far been minimal. Investor psychology is a major factor behind the relative calm.

Even though the S&P 500 (SPX) was essentially flat through yesterday (-9.38 points, or -0.14%), even the markets that have reacted have not reflected true stress. Indeed, crude oil prices are significantly higher, but well below the $100 level that some might have feared. Although some might have expected a flight to safety bid in the US Dollar and Treasuries, only the former occurred. Bond yields rose on inflationary concerns, outweighing the desire for a haven.

As we noted yesterday, European and Asian markets fell sharply, but those were at or near record highs before the crisis. Furthermore, the Nikkei 225 and KOSPI recovered smartly this morning from big drops in the prior session. The Nikkei was -3.6% yesterday but bounced +1.9% today; the KOSPI was off by a stunning -12.06% yesterday and up by a similarly stunning +9.63% today.

[Note: stocks took another leg lower almost immediately after I finished this.]

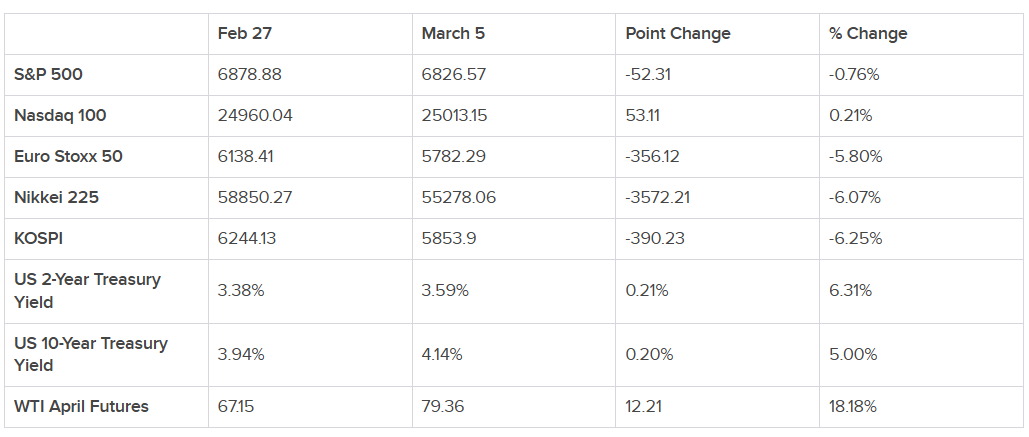

While one could certainly assert that European and Asian markets should have reacted worse than the US because of their dependence upon imported oil and liquefied natural gas, much of it from the Persian Gulf region, one should not have expected the US market reaction to be blasé (in the case of SPX) or even mildly positive (in the case of the Nasdaq 100 (NDX)). The data in the following table shows the lack of concern shown by major US indices compared to other indicators.

Changes in Selected Market Measures, Friday, February 27 through Thursday, March 5, 2026

(Note: US data through noon ET on March 5.)

Source: Interactive Brokers

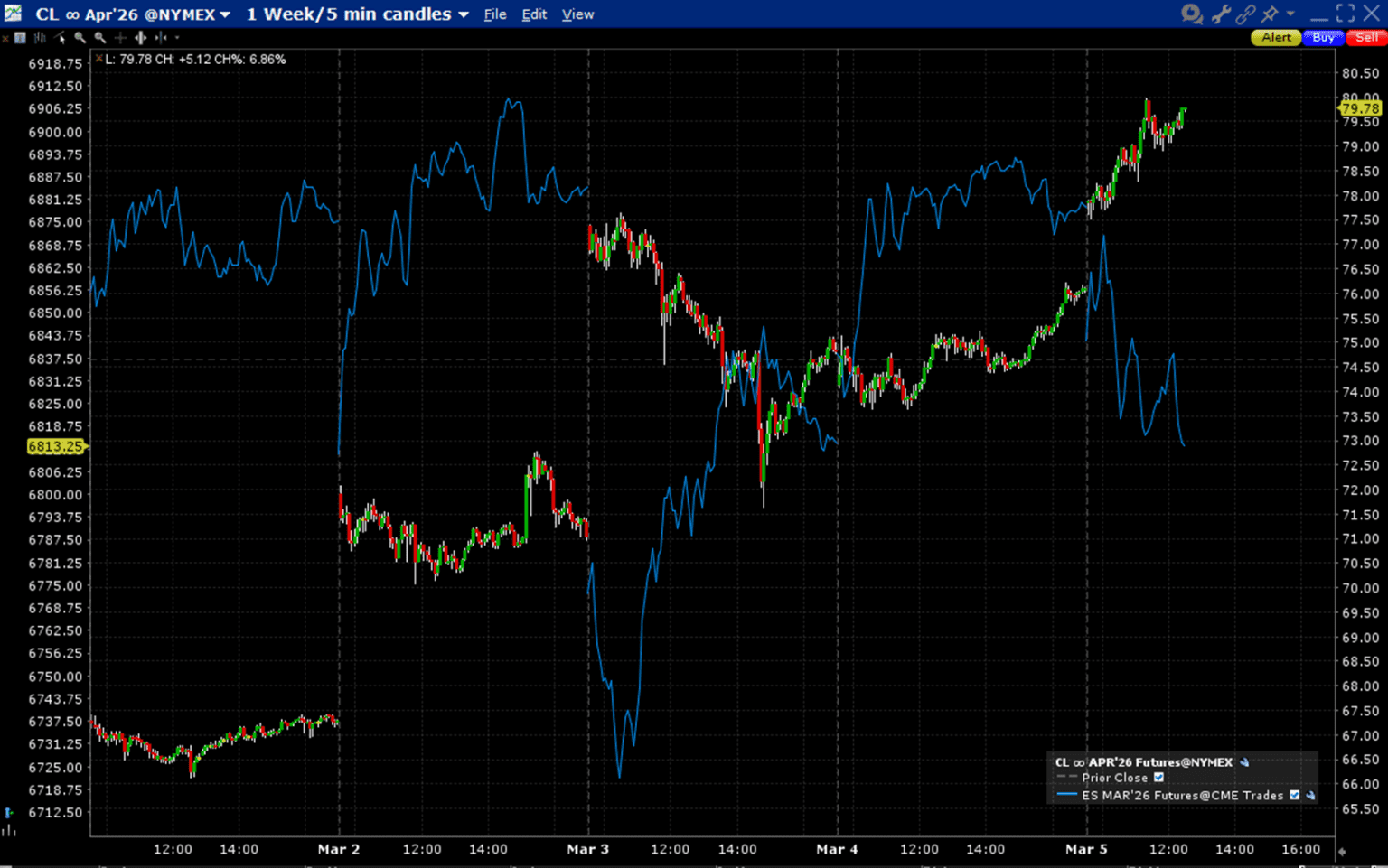

To be fair, it is not as though US equity traders have been completely oblivious to the goings-on. Stocks’ intraday moves have indeed taken their cues from gyrations in oil prices. We have discussed the concept of a “lead,” where traders utilize the movements of a certain key factor as an input for the direction of key index futures. When we look at an intraday chart of this week’s moves in April WTI Futures (CL) versus SPX, we see a definite inverse relationship throughout most of the four days even as SPX remained somewhat impervious to the fact that oil prices have ratcheted higher.

4-Days, April WTI Futures (red/green 5-minute candles, right scale), SPX (blue line, left scale)

Source: Interactive Brokers

This is a testament to the incredibly resilient psychology among US investors. On Tuesday, we attributed this to two factors, which we can recapitulate broadly:

- Investors and active traders are fully conditioned to see every dip as a buying opportunity, no matter the reason. Furthermore, active traders are quick to jump on any nascent bounce, lest they miss out on a rally.

- Equity markets are terrible at pricing in geopolitical events. Unless we can draw a direct line between them and factors that directly affect stock prices – earnings, revenues, cash flows, etc. – they tend to be ignored.

I like to define the second factor as “the Microsoft (MSFT) test,” and it is indeed rooted in fundamental analysis. Investors should ask themselves, “How might this global event affect MSFT?” (The stock in question can be any major US company.) If the answer is “not much,” then we can reasonably expect little market reaction. But in the case of an event that can create global inflation and an economic slowdown, the answer, and hence the index reaction, should reflect that possibility.

Right now, however, equity markets have decided that any Middle East disruption will be short and shallow. That is certainly how the events have been portrayed by the administration, and I have no data that indicates otherwise. But the history of Middle East involvements should cause us to at least consider the alternative. Even when they have occurred on a smaller scale than the current activity, the effects have often persisted longer than some initial hopes. But as long as FOMO, Fear of Missing Out, continues to outweigh actual fear, market optimism will prevail even if other key inputs like oil and rates might indicate otherwise.

Related: Markets Remain Strong, but AI Disruption and Correlation Shifts Flash Caution