Last week, Matt Shumer published something I haven't been able to stop thinking about. Matt builds AI companies. He's been living in this world for six years. And he wrote something I've been trying to articulate to people in my own industry for months: we're past the "interesting dinner conversation" phase. The future is already here. It just hasn't knocked on your door yet.

He wrote it for the people in his life who keep asking what the deal with AI is. I'm writing this for mine — the advisors, firm owners, technology leaders, and compliance people I've worked alongside for 25 years who are doing one of two things right now: quietly experimenting and saying nothing, or dismissing this as something their firm will address eventually.

Neither is the right response. Matt's piece is worth reading in full here. But wealth management has its own version of this story, and it doesn't map cleanly onto what he described. Some of this will move faster here than anywhere else. Some will move slower. Understanding which is which is the only thing that matters right now.

What Matt Got Right (And It Applies To You)

The core argument is simple: AI isn't incrementally improving. It crossed a threshold. The models available today are doing things that would have seemed like science fiction 18 months ago, not because anyone predicted they would, but because the progress is genuinely non-linear.

Matt describes walking away from his computer for four hours and coming back to find finished software that he didn't have to correct. That's the version most visible in tech. But the same shift is happening in every domain where work happens on a screen: reading, analyzing, synthesizing, recommending, drafting, communicating.

That is a fairly complete description of what a financial advisor does all day.

I've spent nearly a decade at a global wealth management software company. I've tracked over 1,000 wealthtech companies through WealthTech Select. I've done hundreds of CRM implementations and data conversions. I've watched this industry adopt technology slowly, reluctantly, and then all at once. I've seen what early looks like and what late looks like.

This is the moment where early and late start to matter permanently.

What's Already Here

Let me be concrete, because this industry deserves specifics, not abstractions.

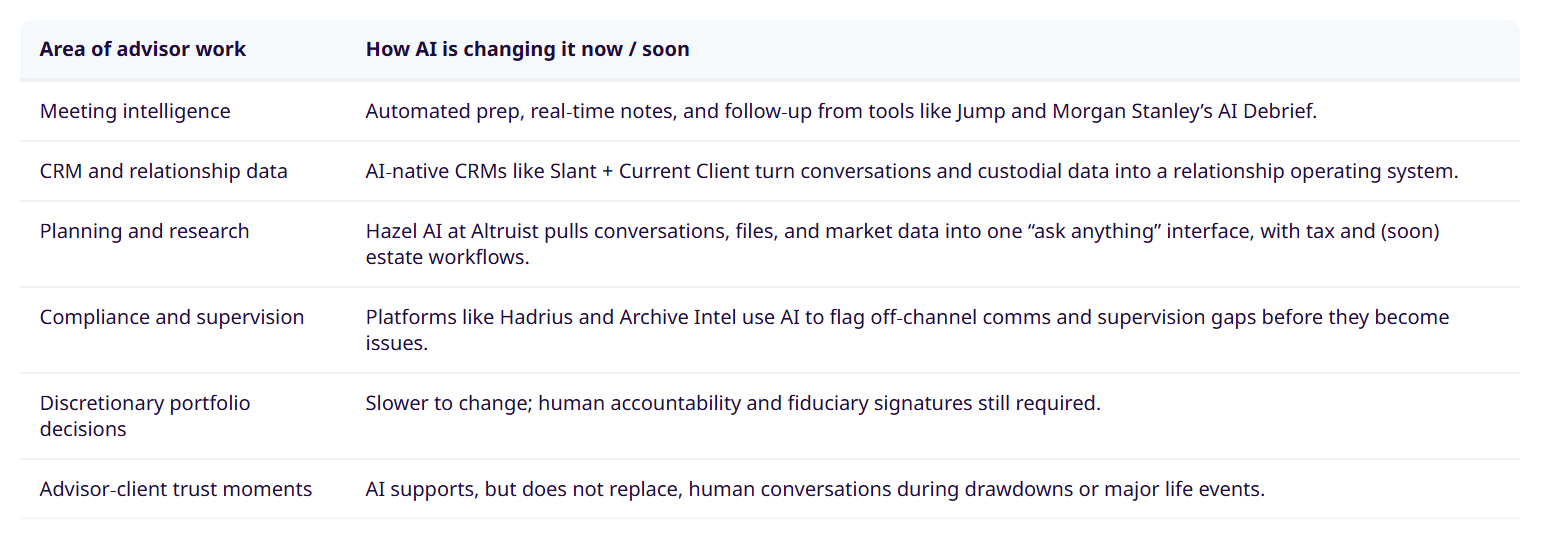

Meeting intelligence is the most visible beachhead. Tools like Jump are already saving advisors over an hour per workday through automated preparation, real-time notetaking, and follow-up generation. Jump had 35% monthly growth through 2024 and landed enterprise clients including LPL Financial and Cetera. As of the most recent data, 18% of advisory teams have adopted AI meeting tools. That number is moving fast.

The notetaker conversation has been almost comically undersold. The industry spent a year debating whether AI notetakers were a "race to the bottom." Meanwhile, advisors were quietly building an entirely new kind of institutional memory, possibly without realizing it; conversations, decisions, commitments, all structured and searchable in ways that email threads and handwritten CRM notes never were. The notetaker wasn't the product. The conversation data was.

The CRM layer is being rebuilt from scratch. Slant CRM is one of the more interesting signals I've watched recently. It's AI-native, built around the household rather than the contact record, and it starts capturing relationship data before someone becomes a client. Prospect conversations, early interactions, unstructured notes alongside structured data — all of it feeds the relationship context from day one. When you pair that with something like Current Client, which surfaces the right insight at the right moment for each relationship, you start to see what I've been calling a Relationship Operating System actually take shape. Not a CRM with AI bolted on. A system where the relationship is the architecture and everything else serves it.

The other piece Slant is moving toward — and this matters more than most people realize — is custodial data integration. Not portfolio management systems. Custodial data. Going to the source. That means transactions, trades, positions, RMDs, beneficiary information, account opening — the ground truth of what's actually happening in a client's financial life, accessible and usable inside the relationship layer.

Planning and research are expanding fast. Altruist's Hazel AI launched in September 2025 with the ability to query client conversations, emails, files, and market data from a single interface. They've since released a dedicated tax planning tool, and the direction from there is fairly obvious — estate planning is a logical next expansion, given how much of the relevant data already lives in the custodial and account layer Altruist controls. The "ask anything" functionality isn't a feature. It's a preview of what the entire advisory workflow looks like in 18 months.

Client communication is where the leverage is most underestimated. Morgan Stanley's AI Debrief is saving 30 minutes per client meeting across one million annual client calls. Do that math across your firm. That isn't efficiency. That's a different business model.

The Regulatory Moat Is Real — But It's Not What You Think

Here's where wealth management diverges from what Matt described. And this is important to get right, because the wrong lesson here is dangerous.

Regulation will slow AI adoption in certain specific areas. Discretionary investment decisions require human accountability. Formal financial advice requires a licensed fiduciary signature. Certain supervisory and attestation functions have legal requirements built around human oversight. The SEC, FINRA, and state regulators aren't going away, and compliance frameworks are deliberately designed to move slower than markets.

This creates a temporary moat in some places. Emphasis on temporary.

What it does not protect is the 60-70% of advisor time currently spent on non-revenue-generating activities — the meeting prep, the follow-up emails, the document assembly, the research synthesis, the CRM data entry, the scheduling coordination, the internal reporting. None of that is protected by regulation. All of it is vulnerable right now.

The mistake would be to look at the places where AI can't yet sign a Form ADV and conclude that AI isn't disrupting advisory. It already is. It's just starting with the parts that don't require your license.

My co-host, on the AI for Advisors Podcast, Mark Heynen and I were recently on the Zero Basis Points podcast with Haik Sahakyan and George Guidotti — between the simultaneous sips (IYKYK) one of the things we kept coming back to was this: right now, inside advisory and wealth firms, compliance departments are the single biggest barrier to AI adoption. Not the technology. Not the cost. Compliance. The instinct is to treat AI as a risk to be managed rather than a tool that manages risk.

"The instinct is to treat AI as a risk to be managed rather than a tool that manages risk."

But here's my prediction: the notetakers knocked at the compliance gates first. They did the initial work of getting AI into the room. The ones who actually collapse the castle walls are companies like Hadrius and Archive Intel — the platforms purpose-built to help compliance departments use AI to do their own jobs better. The moment compliance sees AI catching what their manual review processes miss, flagging the off-channel communications before they become SEC inquiries, surfacing supervision gaps in real time — that's when the wall comes down. Not because compliance gave up. Because AI proved it was on their side.

Once that happens, the internal resistance at large firms changes character entirely. It goes from "we can't allow this" to "we need more of this."

In the meantime: the regulatory friction that slows AI adoption inside large broker-dealers and wirehouse platforms is the same friction that creates an asymmetric opportunity for nimble RIAs. The firms that can experiment, adapt, and rebuild workflows without a 200-person compliance review cycle are going to establish capability advantages that compound. Large firms will eventually deploy AI at scale. But the distribution of those capabilities will be negotiated and delayed and filtered through institutional caution in ways that won't apply to a 12-person RIA that can make a decision this week.

"The 55% of advisors who told researchers that integrated technology platforms are their most important consideration in a custodian or aggregator relationship are telling you something about where this goes. The platform that figures out the AI layer first doesn't just win efficiency. It wins talent and assets."

The Architectural Problem Under Everything

I've written about CRM's original sin before. I've written about why email was built for 1971. This is the third piece in that same argument.

The reason AI lands differently in wealth management isn't just regulatory. It's architectural. Most firms are trying to add AI to systems that were never designed to hold the kind of data AI actually needs to be useful.

A CRM that holds static contact records and timestamped notes can't tell you that a client mentioned a large purchase coming up three conversations ago, that cash isn't available in their accounts to fund it, and that a trade will need to happen before a wire can go out — all surfaced in real time, in context, without anyone running a report.

That's the gap between where we are and where this goes. Not someday. The architecture to do this is being assembled right now.

Think about what the current workflow actually looks like when a client says in a meeting they need $250,000 for a purchase. The advisor notes it. Someone creates a task. The task gets assigned to a trader. The trader runs a rebalance, generates trades, submits them. On T+1, someone is watching for settlement and queuing a wire request. Forms get filled. Accounts get looked up. Tasks get marked complete. Three to five people touched something that started as a single sentence in a client conversation.

Now think about what the same moment looks like on AI-native infrastructure with live custodial data. The advisor says it out loud. The system knows in real time that cash isn't available. It knows what positions exist and what a liquidation would look like. It queues the trade, the allocation, the settlement tracking, the wire request — with the right accounts, the right amounts, the right compliance flags already populated. No form filling. No looking things up. Two humans click go, because regulations require it and because trust between humans and AI systems is still being earned. The advisor initiated the action with their voice. Everything else was already done.

- Legacy workflow: Client mentions a $250,000 need; advisor writes notes, ops creates tasks, trader rebalances, someone tracks T+1 settlement, someone else queues the wire.

- AI‑native workflow: Client says “I’ll need $250,000”; system checks cash, models liquidation, queues trades and wire with correct accounts and compliance flags; two people review and click approve.

That's not science fiction. That's the logical endpoint of combining AI-native relationship data with direct custodial integration — going to the source, not routing through portfolio management middleware. Slant isn't fully there yet. Nobody is. But the architectural decisions being made right now determine whether that future is possible in three years or ten.

That's what a Relationship Operating System means in practice. Not a better CRM. A system where the relationship context, the financial reality, and the operational workflow are all the same thing.

An AI-native relationship operating system requires:

- Unified relationship record (prospects and clients, structured and unstructured data).

- Direct custodial data integration (transactions, positions, RMDs, beneficiaries, account opening).

- Embedded meeting intelligence (notes and action items tied to the right household).

- Built‑in compliance layer (surveillance, supervision, audit trail by default).

Matt wrote about the feedback loop where AI helps build the next version of AI. The same dynamic exists here. Firms that adopt AI-native relationship infrastructure start accumulating structured, synthesized, queryable relationship data. That data makes the AI more useful. The more useful AI generates better advisor outcomes. Better outcomes attract more clients. More clients generate more data. The loop closes.

Firms staying on legacy architecture don't have that loop. They have email threads and manually entered CRM notes and an archiving bill.

What Moves Fast

Anything that doesn't require a license or a signature is moving now. Meeting preparation. Follow-up drafting. Research synthesis. Financial plan generation. Client communication. Prospecting. Workflow automation. Internal reporting. All of it is either already AI-assisted or will be within 18 months.

The advisors who are experimenting seriously — not occasionally poking at the free tier of ChatGPT, but actually rebuilding workflows — are seeing productivity changes that don't look like small improvements. They look like a different job.

What Moves Slower (But Not As Slowly As You Hope)

Fiduciary accountability, discretionary portfolio decisions, the advisor-client trust relationship built over years — these have real friction. AI doesn't sign Form ADVs. Clients still want to hear a human voice when markets drop 20% in a week.

But "slower" in the current environment means two to three years, not ten. The same way healthcare took nine years to move from 39% to 70% patient portal adoption — and we're now three to five years behind banking on this curve — the question isn't whether, it's when.

The firms managing the transition well are treating regulatory requirements as fixed constraints to architect around, not as reasons to wait. Compliance is built into the platform, not bolted on after the fact. The audit trail is automatic. Supervision is feasible because everything is centralized. These firms aren't hoping regulation protects them. They're building systems that make compliance a byproduct of good architecture.

Where AI Lands First vs Later

The Simple Version

Matt wrote for the people in his life who keep asking what the deal is. Here's mine for this industry.

The advisory firms that will matter in five years are being built on AI-native infrastructure right now. Not because AI makes better investment decisions — it doesn't, not yet, not in ways that matter for your clients today. But because the relationship layer, the communication layer, the research and synthesis and workflow layer, is being rebuilt from scratch by the firms willing to acknowledge that the old architecture was always broken.

The CRM your firm has used for 10 years was built for one-sided data capture. The email system you still use for substantive client communication was built in 1971. The quarterly review process that generates a PDF attachment nobody reads was designed when advisors had 60-client books and no fiduciary standard.

None of that was built for what you've become. AI didn't create that problem. AI just made it urgent.

You don't have to abandon everything at once. But you do have to decide whether you're building toward the architecture that compound advantages or defending the one that doesn't.

The water is rising. I've watched this industry stand in it long enough.

What advisors should do next?

- Audit where advisors spend non‑revenue time today.

- Pilot one meeting‑intelligence tool with a small advisor group.

- Map custodial data into your relationship layer instead of just portfolio tools.

- Involve compliance early with tools built for them (Hadrius, Archive Intel, etc.).

Related: Email Is Becoming a Compliance Liability in Wealth Management