- Leveraged Exchange-Traded Funds (ETF’s) seeks to amplify the daily return of an index typically by a factor of 2x or 3x.

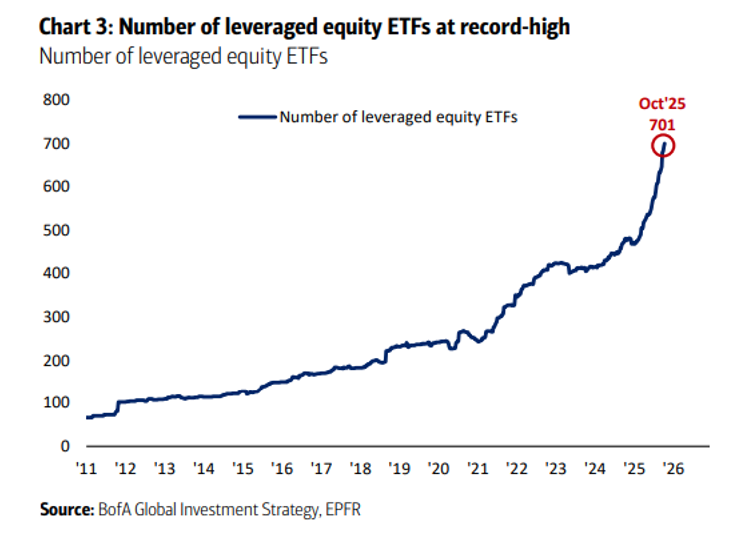

- These products have become popular on Wall Street with over 700 leveraged equity ETF’s now available

- Utilizing leveraged ETF’s in a long-term portfolio leads to underperformance and excess risk

What are Leveraged ETF’s?

“Whenever a really bright person who has a lot of money goes broke, it’s because of leverage. ” – Warren Buffet

Leveraged ETF’s are investment vehicles that seek to augment the daily performance of an index by a certain factor by utilizing derivatives and leverage to achieve daily results. These investment vehicles have gained popularity given increased accessibility, market speculation and social media hype.

Leveraged ETF’s seek to amplify the return profile of the underlying index such as by 2x or 3x. Recently, three issuers are in the process of offering 5x leveraged ETFs.

As of October 2025, there are over 700 leveraged equity ETF’s in the United States.[1]

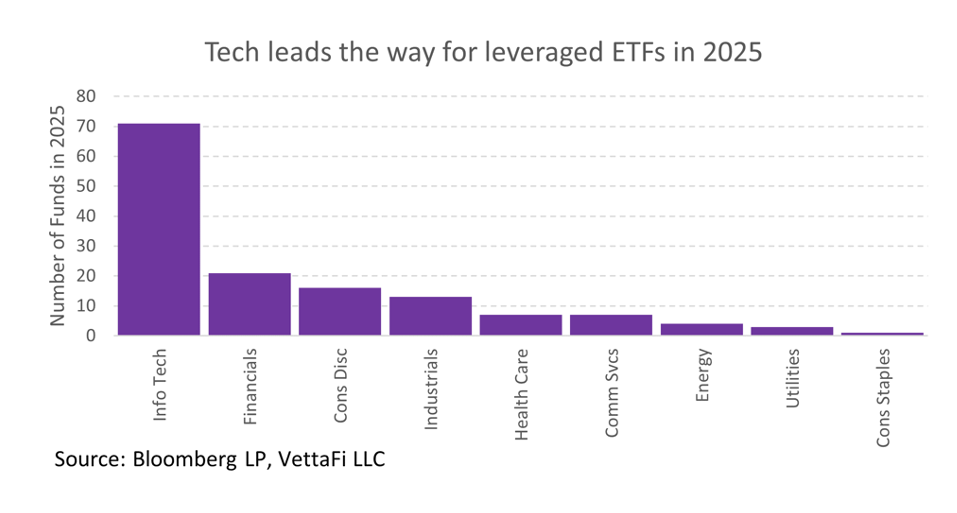

The vast majority of leveraged ETF’s launched in 2025 have been in the information technology sector.[2]

How do Leveraged ETF’s Operate?

Leveraged ETF’s utilize debt and derivatives to attempt to magnify the daily performance of their underlying index.

We compared a hypothetical 3x Leveraged ETF to that of the underlying index.

Why Do Levered ETF’s Underperform Over Long Time Periods?

Leveraged ETF’s tend to underperform over long time periods for several reasons.

Volatility Drag

Leveraged ETF’s suffer from volatllity drag primarily as a result of daily rebalancing and the compounding of returns. Higher volatility rates has a substantial drag on returns of leveraged ETF’s. Leveraged ETF’s also must adjust holdings on a daily basis to maintain leverage ratios which leads to selling low and buying high.

To illustrate this concept, we assumed a hypothetical scenario comparing the same hypothetical 3x leveraged ETF to it’s index assuming substantial downside and upside volatility.

Despite the index remaining unchanged after two days, the leveraged ETF significantly underperforms in this example.

Interest Costs

The financial cost to create the leveraged returns does not come free as deriatives and borrowing is used to create the embedded leverage in a leveraged ETF. This cost of financing comes as a substantial drag over long time periods, contributing to their underperformance.

Fees

Leveraged ETF’s also come with high expense ratios due to their operational costs. While the net expense ratios vary, the cost of a leveraged ETF ranges from 1. 0-1. 5%. The ETF that tracks the underlying index can typically be purchased with net expense ratios of less than 0. 25%.

Conclusion

Despite the increasing popularity of leveraged ETF’s, we do not believe in their suitability in client portfolio construction. The embedded risks of leveraged ETF’s are substantial, yet we do not believe the financial community outlines these risks appropriately. We believe those with leveraged ETF’s as part of their long term investment plan need to seriously re-consider their investment selection.

[1] BofA Global Investment Strategy and EPFR

[2] Bloomberg LP, VettaFi LLC